Introduction

Every time a dealer marks up an extended warranty and hands the contract to a third-party provider, they're keeping the spread — but giving away something far more valuable: the underwriting profit, the investment income, and years of compounding wealth that the provider quietly keeps.

The numbers make the stakes clear. According to NADA data, F&I profit per vehicle retailed climbed 14% across 2025, while front-end gross fell to $279 in December — down 52.4% year-over-year. F&I is now carrying dealership profitability.

Dealers who rely only on warranty markup are leaving hundreds of thousands in long-term profit on the table. Dealerships that have transitioned to dealer-owned reinsurance are building wealth assets that outlast any single vehicle sale.

Below, we break down how each model works, what dealers actually earn from each, and how to match the right approach to your dealership's volume, risk tolerance, and financial goals.

Key Takeaways

- Aftermarket warranty markup is simple and low-risk: dealers buy contracts wholesale and mark them up at retail, but the provider retains all underwriting profit and investment income

- Dealer-owned reinsurance captures those underwriting profits and investment returns by owning the company that backs the warranty risk

- Reinsurance requires more setup and structure, but delivers significantly higher lifetime returns, tax advantages, and wealth-building potential

- Volume, risk appetite, and long-term goals all factor into the decision — most established dealers selling 30+ units per month are well-positioned for reinsurance

Reinsurance vs. Aftermarket Warranty Markup: Quick Comparison

Here's how the two approaches stack up across the factors that matter most to dealer profitability.

| Aspect | Warranty Markup | Reinsurance |

|---|---|---|

| Profit Potential | One-time front-end spread per deal; provider keeps the underwriting profits | Front-end income plus underwriting profit, investment returns, and surplus distributions |

| Control Over Claims | None — third-party provider manages all claims and reserves | Dealer controls claims experience and reserve funds through their own entity |

| Tax Treatment | Revenue recognized immediately as ordinary income | Premiums grow tax-deferred in trust; taxed only on distributions or investment income |

| Setup Complexity | Minimal — dealer resells a third-party product at a markup | Requires forming a reinsurance entity, working with a program administrator, and maintaining compliance |

A program administrator like DealerRE handles the entity setup, compliance, and ongoing administration — so dealers get the benefits of reinsurance without managing the structure alone.

What Is Aftermarket Warranty Markup?

Aftermarket warranty markup is the simplest participation model in F&I: dealers purchase Vehicle Service Contracts (VSCs) or extended warranties from third-party providers or manufacturers at wholesale cost, then resell them to customers at a marked-up retail price. The difference between wholesale and retail is the dealer's F&I income.

According to industry sources, dealer markup typically accounts for 50% or more of the VSC's retail price. Dealer cost for a VSC typically ranges from $600-$1,200 depending on coverage level, vehicle, and term, while retail pricing runs $1,500-$3,500.

The markup spread is the dealer's only income from the transaction. Once the contract is sold, all premiums flow to the provider who manages reserves, pays claims, and retains any unused premium as underwriting profit. None of that returns to the dealer.

That structure works for certain dealer profiles, but it also defines where the model's ceiling sits.

Where Aftermarket Warranty Markup Fits

Warranty markup suits dealer operations where:

- Lower-volume dealerships sell fewer than 25-30 VSC contracts monthly

- Dealers are early in their F&I program development and lack administrative infrastructure

- Franchise dealers offer manufacturer-backed extended warranties where markup is the primary participation mechanism

Structural limitations to consider:

- Markup income builds no reserve and earns no investment return

- Every dollar of F&I profit is recognized and taxed in the year it's earned — no deferral advantage

- The profitability ceiling is fixed at the spread, regardless of how low claims experience runs

- Strong product performance generates no additional income for the dealer

What Is Dealer-Owned Reinsurance?

Dealer-owned reinsurance is a structure in which the dealer forms and owns their own reinsurance company that assumes the risk behind the F&I products (VSCs, GAP, tire and wheel, etc.) sold at the dealership. Instead of premiums flowing to a third-party carrier, they flow into the dealer's own trust, where they build as a reserve.

The Admin Obligor Model

In the admin obligor model, the dealer's reinsurance company is the obligor on the contract, backed by an A-rated insurer that fronts the product. This gives the dealer full participation in underwriting profits while remaining protected from catastrophic exposure.

According to industry standards, the dealer's entity is the named obligor responsible for claims payment, but ultimate liability rests with the fronting carrier — ensuring claims are paid even if the dealer's reserve is depleted. DealerRE has helped over 400 dealers implement this model nationwide.

How Premiums Are Structured in Trust

Unearned premium reserves (UPR) are held in restricted accounts to cover open claims. These A accounts are invested conservatively — typically 90% fixed income, maximum 10% equities.

Once contracts mature and claims are settled, surplus funds transfer to an unrestricted B account where they can be invested more aggressively and accessed by the dealer. The B account allows dealers to invest in equities, higher-yielding assets, and even real estate, generating returns that compound tax-deferred over time.

Tax Advantages

Premiums deposited into the reinsurance trust are generally treated as tax-deferred income. Dealers are not taxed on premiums until claims are paid or distributions are made — reducing current-year tax liability and improving cash flow.

Under Section 831(b), small reinsurance companies are taxed only on investment income — not underwriting gains — provided annual premiums stay under $2,450,000. For dealers in high tax brackets, that distinction alone can shift thousands of dollars from the IRS to the trust.

Wealth-Building Applications

Unlike markup income which is consumed immediately, reinsurance surplus can be reinvested and deployed strategically:

- Build a tax-deferred retirement fund entirely separate from dealership operations

- Fund acquisitions or facility upgrades using surplus capital you already earned

- Transfer wealth to the next generation through structured distributions at exit

- Retain key managers with profit-sharing tied directly to reinsurance performance

That's a different financial profile than simply marking up a warranty contract — and understanding the gap between the two is where the real decision gets made.

Head-to-Head: Profit, Control, and Long-Term Value

Profit Comparison Over Time

Warranty markup generates predictable but fixed per-deal income. Reinsurance generates that same front-end income AND accumulates underwriting profit from unused premiums — meaning a dealer's effective return per contract grows substantially over the life of the program.

Industry data shows VSC loss ratios can be as low as 30%, with 40% commonly used in modeling. That means 50–70% of collected premiums may remain after claims — underwriting profit that dealers capture through reinsurance but forfeit under markup-only models.

A dealer selling 30 VSC contracts monthly at an average premium of $1,200 collects $432,000 annually. At a 40% loss ratio, that dealer could retain roughly $259,200 in underwriting profit over the contract term — profit a markup-only dealer never sees.

Claims Control and Loss Ratio Management

With reinsurance, the dealer has visibility into and direct influence over the claims experience. Lower loss ratios produce more surplus — the dealer is rewarded for running a tight program.

With markup, claims performance is irrelevant. The dealer earns the same spread whether the product pays out heavily or barely at all.

Risk Profile

Markup carries zero reserve risk but also zero upside beyond the spread. Reinsurance involves managed risk — the dealer takes on underwriting exposure but is backstopped by A-rated insurer backing (in admin obligor structures) and guided by reserve requirements, making the risk manageable rather than uncapped.

Tax and Cash Flow Impact

Markup income is taxed immediately as ordinary income. For dealers in higher tax brackets, reinsurance income compounding tax-deferred on hundreds of thousands of dollars in annual premiums creates a material difference in both cash flow and long-term net worth.

Here's how the two models compare across these four dimensions:

| Factor | Markup Only | Reinsurance |

|---|---|---|

| Underwriting profit | Forfeited to provider | Retained by dealer |

| Claims performance impact | None — spread is fixed | Direct — lower loss ratios = more surplus |

| Tax treatment | Ordinary income, taxed immediately | Tax-deferred accumulation |

| Reserve risk | Zero | Managed, backed by A-rated insurer |

Investment Income and Compounding

Once funds clear to the surplus B account, dealers can invest them across a broader range of assets — equities, real estate, or reinvestment in the dealership. The benefits of a thoughtful investment program can be substantial, with B account funds compounding over time on a tax-deferred basis.

Markup programs offer none of this. Once the spread is earned, the income leaves the dealer's control — taxed, distributed, and gone.

Which Model Is Right for Your Dealership?

Volume Threshold Considerations

Reinsurance programs typically require a minimum monthly contract volume to be financially viable. Industry sources cite 25-30 VSCs monthly (300-350 annually) as the minimum for reinsurance viability.

Dealers below that threshold often start with markup and transition to reinsurance as F&I production grows.

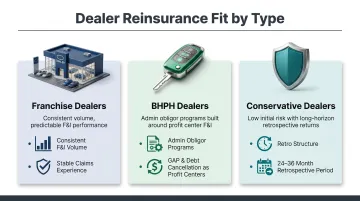

Dealer Type and Risk Tolerance

The right entry point also depends on your dealership's profile:

- Franchise dealers with consistent, predictable F&I volume are strong reinsurance candidates from the start — their product mix and brand reputation support stable claims experience.

- BHPH dealers benefit through admin obligor programs that protect against mechanical losses funded by their customer base. Debt cancellation coverage, collateral protection insurance, and GAP convert traditional risk exposures into profit centers.

- Conservative dealers can start with a retro structure, receiving surplus distributions after a retrospective period (typically 24-36 months) without taking on direct reserve risk before committing to full reinsurance participation.

Long-Term vs. Short-Term Orientation

Markup delivers immediate, predictable income per deal. Reinsurance builds something more durable: accumulated reserves that can fund retirement, support succession planning, or generate tax-efficient wealth over time.

Mercer Capital notes that reinsurance "can represent a significant component of a dealer's income and enterprise value in an extremely tax-efficient manner."

Conclusion

Aftermarket warranty markup and dealer-owned reinsurance represent different levels of F&I maturity, not competing philosophies. Markup generates income. Reinsurance builds it into a program that keeps paying out long after the contract is sold.

The right fit depends on where a dealer is today and where they want their business to go. For dealers selling 25-30 VSC contracts monthly or more, and especially for those in high tax brackets with long-term wealth-building goals, reinsurance delivers returns that markup simply cannot match.

For dealers ready to stop giving away underwriting profits to third-party providers and start retaining reserve growth, investment returns, and claims savings inside their own structure, the path forward is clear. Connect with DealerRE to find out whether your dealership is ready to make the transition.

Frequently Asked Questions

How much do dealers mark up extended warranties?

Dealer markup typically accounts for 50% or more of the VSC's retail price, with dealer cost ranging from $600-$1,200 and retail pricing from $1,500-$3,500. The markup is the dealer's only profit source — the underlying underwriting profit stays with the provider.

Do dealers lose money on warranty repairs?

Under markup-only models, the third-party provider covers all claims — dealers absorb no repair costs but keep no underwriting profit either. A dealer-owned reinsurance model shifts that financial exposure to a structure the dealer controls, allowing them to retain the profit instead.

What are the 4 types of reinsurance?

The four primary structures in auto dealer reinsurance are:

- Walkaway — low risk, markup-only profit

- Retro — surplus distributions after 24-36 months

- CFC/Offshore — tax-deferred premium growth under Section 831(b)

- DOWC/Domestic — admin obligor with significant tax efficiency

Each carries different risk, profit, and tax profiles depending on the dealer's situation.

How much does a 100,000 mile extended warranty cost?

The dealer's wholesale cost for a high-mileage VSC varies by coverage level and vehicle age, typically ranging from $600-$1,200. Without a reinsurance program, both the retail markup and the underlying premium reserve stay with the provider — profit the dealer generated but never captured.

What is the red flag rule for car dealers?

The FTC Red Flags Rule requires auto dealers to implement a written Identity Theft Prevention Program covering identity theft detection, response, and prevention in credit transactions. While separate from reinsurance compliance, dealers building out F&I programs typically need support across both areas — and full-service reinsurance administrators like DealerRE handle the compliance management, filings, and legal forms that keep programs running cleanly.