Introduction

F&I products generate significant revenue at auto dealerships nationwide, but most underwriting profit flows to third-party providers—not back to the dealership. This structural reality has dealer principals and F&I directors asking a fundamental question: should we continue compensating third-party administrators (TPAs) with our sales volume, or should we establish a Dealer-Owned Warranty Company (DOWC) to capture those profits ourselves?

F&I gross profit per vehicle retailed reached $2,545 in Q4 2025—within range of the all-time high set in Q3 2022. That income concentration makes the question of who captures the underwriting profit increasingly hard to ignore.

The Tax Cuts and Jobs Act (TCJA) reduced the C-corporation tax rate to a flat 21%, making domestic DOWC structures viable for dealers who previously had no alternative to offshore arrangements. With over 600 dealerships changing hands in 2025, the right structure also directly impacts enterprise value at exit.

This post defines both models, compares them across key dimensions like profit retention, volume thresholds, and tax advantages, and provides a framework for deciding which path fits your dealership.

Key Takeaways

- A DOWC captures 100% of underwriting profits and investment income — but requires roughly 100–150+ VSCs/month and real infrastructure to justify the setup

- A TPA handles administration and compliance, making it the right fit for smaller dealers not yet ready for a DOWC

- DOWCs create separate legal entities that add enterprise value at sale, while TPA arrangements generate commission income only

- The TCJA's flat 21% C-corp rate and indefinite NOL carryforward rules make DOWC tax advantages more accessible today

- Most dealers start with a TPA and graduate to a DOWC or dealer-owned reinsurance structure as volume and infrastructure grow

DOWC vs. TPA: Quick Comparison

Both models can coexist: a DOWC typically still contracts with a TPA for administration. The real distinction comes down to ownership and profit structure, not administration alone.

| Dimension | DOWC | TPA |

|---|---|---|

| Profit Retention | 100% of underwriting profit and investment income | Commission or reserve participation only |

| Setup Complexity | High—requires entity formation, state registration, CLIP, compliance infrastructure | Minimal—dealer contracts with existing provider |

| Volume Requirements | 100–150+ VSCs/month break-even; optimal at 200+ | Works at any volume |

| Control Over Products/Pricing | Full control—set terms, pricing, private-label branding | Limited—dealer sells from TPA's portfolio |

| Tax Advantages | Significant—NOL carryforward, tax deferral on underwriting profits | Standard corporate tax treatment |

| Compliance Burden | Heavier—multi-state registration, financial reporting, annual filings | Lighter—TPA handles regulatory complexity |

| Enterprise Value at Sale | Adds enterprise value as separate legal entity | No added entity value |

Volume thresholds and profit retention are where most dealers underestimate the DOWC opportunity — both are explored in detail below.

What is a Dealer-Owned Warranty Company (DOWC)?

A DOWC is a domestic C-corporation formed by the dealer specifically to serve as the named obligor on service contracts sold through their dealerships. The DOWC replaces a third-party provider as the entity legally responsible for fulfilling warranty contracts—meaning the dealer, not an outside company, holds the underwriting position.

How a DOWC Works in Practice:

The DOWC is registered as a service contract provider in each state where producing dealerships operate. It contracts with a TPA for claims adjudication and administration, and secures a highly rated insurer to back contracts via a Contractual Liability Insurance Policy (CLIP). Three key agreements govern the structure:

- Administration/Management Agreement – defines the TPA's operational responsibilities

- Contractual Liability Insurance Policy (CLIP) – provides failure-to-perform coverage from an A-rated insurer

- Dealer/Producer Agreement – establishes the relationship between the DOWC and the selling dealership

Profit and Tax Advantages:

Underwriting profits and investment income flow entirely to the DOWC (and therefore the dealer). The DOWC uses the same tax deferral mechanism available to Property & Casualty insurance companies: expenses of administration and acquisition are deducted in the current year, and net operating losses carry forward indefinitely (limited to 80% of taxable income in any given year).

Dealers can invest reserves at institutions of their choosing and borrow against them for any business or personal purpose.

Control Advantages:

Dealers set their own coverage terms, pricing, and marketing materials. They can private-label products, tailor offerings to their vehicle inventory, and manage the claims experience directly to improve customer satisfaction and retention.

DealerRE has spent over 28 years helping dealers establish admin-obligor reinsurance companies, a closely related structure that delivers the same profit-retention and control benefits as a DOWC, for dealerships nationwide.

Use Cases of a DOWC

Best suited for:

- Dealership groups with high VSC volume (typically 100–150+ contracts per month)

- Multi-rooftop operations that can spread compliance overhead across scale

- Dealers with a long-term exit strategy who want to add a profit-generating legal entity to their enterprise value

- Dealers with access to strong legal, tax, and administrative infrastructure—whether handled in-house or through a partner like DealerRE, covering state licensing, compliance filings, and financial reporting

What is a Third Party Administrator (TPA)?

In the auto dealer F&I context, a TPA is an external company that administers service contracts on behalf of the dealer or a warranty provider. The TPA handles premium processing, claims adjudication, compliance, reporting, and customer service—while retaining the underwriting position and associated profits.

How Dealers Interact with TPAs:

The dealer sells F&I products from the TPA's portfolio and earns a commission or participates in a reserve program. The bulk of underwriting profit—the difference between premiums collected and claims paid—stays with the TPA. Dealers generate the sales volume but capture only a fraction of the income their business produces.

What TPAs Do Well:

They absorb the regulatory and administrative complexity, require no upfront capital structure or entity formation, and can be deployed at any dealership volume. For newer dealers or those without F&I infrastructure, this is a practical starting point.

Limitations:

- Limited customization of products or pricing

- No tax deferral advantages

- Dependence on the TPA's claims decisions and customer service quality

- No enterprise value created for the dealer's own balance sheet

Use Cases of a TPA

A TPA works best in specific situations where simplicity outweighs profit optimization:

- Smaller or single-rooftop dealers with lower monthly volume

- Dealers early in their F&I development

- Those who prioritize administrative simplicity over maximum profit capture

- Dealers building toward a DOWC or reinsurance structure, using the TPA for operational continuity in the interim

DOWC vs. TPA: Which Structure Wins for Your Dealership?

This is not a universal winner/loser comparison—it is a volume, readiness, and goals question. For most dealers below a certain threshold, a TPA arrangement is the right starting point. Continuing with a TPA indefinitely, however, means permanently subsidizing third-party profits with dealer-generated sales volume.

Volume Threshold Reality

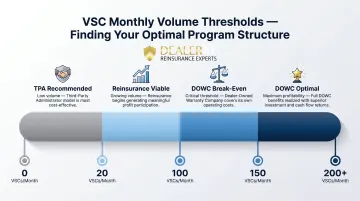

The commonly referenced benchmark is approximately 100–150 VSCs per month at which DOWC economics begin to outpace TPA participation. Below that threshold, compliance and administrative costs often erode the profit advantage.

Dealer-owned reinsurance participation becomes practical at 20–25 VSCs per month. DOWC break-even typically requires 100–150+ VSCs per month, with economies of scale maximized at 200+.

Tax Planning Dimension

In a DOWC or admin-obligor reinsurance structure, dealers gain access to the same tax deferral mechanisms that P&C insurance companies use—a significant long-term wealth-building advantage that a standard TPA arrangement does not provide. Reserve investment income can be deployed into:

- Real estate acquisitions

- Dealership reinvestment and facility upgrades

- Education, watercraft, or other appreciating assets

- Business expansion and succession planning

Customer Experience and Retention

With a DOWC or dealer-owned reinsurance, the dealer controls claims outcomes, service quality, and product design—creating a direct feedback loop between the warranty experience and customer loyalty. With a TPA, those decisions are made externally, creating a structural incentive mismatch.

That misalignment has measurable consequences: dealerships have lost 12% of service visits to competition since 2018, and only 54% of owners with cars 2+ years old return for dealership service, down from 72%.

Situational Recommendations

Choose a TPA if:

- You're a smaller dealer, new to F&I product programs, or not yet at the volume threshold for a DOWC

- You prioritize administrative simplicity and want to avoid entity formation and state compliance overhead

Choose a DOWC or dealer-owned reinsurance structure if:

- You have scale (100-150+ VSCs/month)

- You want full profit retention and control over your F&I program

- You're planning long-term wealth building or an exit and want to add enterprise value

- You have access to strong legal, tax, and administrative infrastructure

DealerRE offers a free dealership analysis that projects your volume-based break-even point, estimated profit retention, and whether a DOWC or reinsurance structure makes sense for where your dealership is today.

Conclusion

TPAs provide simplicity and accessibility, while DOWCs and dealer-owned reinsurance structures offer maximum profit, control, and long-term financial advantage—but require scale and infrastructure to deliver on that promise.

The choice connects directly to real operational outcomes:

- Profit per deal — how much F&I income stays in your pocket vs. a third party's

- Tax planning capability — whether your structure supports long-term wealth building

- Enterprise value at exit — what your program contributes to dealership valuation

Evaluate your current F&I arrangement against what you could be capturing, and consult with a reinsurance specialist like DealerRE before assuming your current model is optimal.

Frequently Asked Questions

What is a dealer-owned warranty company (DOWC)?

A DOWC is a separate C-corporation formed by the dealer to serve as the named obligor on service contracts, allowing the dealer to retain underwriting profits rather than paying them to a third-party provider.

How does a DOWC (dealer-owned warranty company) work?

The DOWC registers as a service contract provider in applicable states, contracts with a TPA for administration and claims handling, and secures a Contractual Liability Insurance Policy from a rated insurer to back the contracts sold through the dealer's stores.

Do dealerships make money on warranties?

Dealers earn commission or reserve participation from TPA-administered warranties, but in a DOWC or dealer-owned reinsurance structure, they retain 100% of underwriting profits and investment income—significantly increasing total F&I profitability per deal.

Is an extended warranty from a DOWC worth it?

Yes, from the dealer's perspective—the dealer controls pricing, coverage terms, and claims outcomes, which benefits both profitability and customer satisfaction. A rated insurer backs the contract, giving customers the same protection they'd expect from any third-party product.

What are the alternatives to DOWC?

The primary alternatives are a third-party administrator arrangement (where the TPA retains underwriting profit), dealer-owned reinsurance (an admin-obligor structure that captures similar financial benefits with a streamlined formation process), and manufacturer-backed F&I products.

What are the three types of warranties?

Manufacturer warranties cover defects at no added cost. Dealer warranties are offered directly by the dealership. Extended warranties — or vehicle service contracts — cover repairs beyond the factory period and can be issued through either a TPA or a DOWC, a key structural decision that affects how much profit the dealer retains.