The reinsurance value chain is the sequence of participants and profit flows—from the car buyer's F&I product premium through administrators, insurers, and reinsurers—that determines who ultimately keeps the underwriting profit on vehicle service contracts, GAP, and related products. For most dealerships, that profit ends up somewhere other than their own account.

This article is written for franchise dealers, independent dealers, and BHPH operators. If you're selling F&I products through a third-party provider, you're generating revenue at the front of this chain while someone downstream collects the larger share of profit. Understanding how the chain is structured—and where you currently sit in it—is the first step toward changing that.

TL;DR

- F&I premiums flow from the customer through the dealer, administrator, and insurer—with underwriting profit accumulating at the downstream end

- In the traditional model, dealers earn a front-end markup but lose the underwriting margin to third-party providers

- Dealer-owned reinsurance repositions the dealer at the downstream end, where reserves accumulate and convert to profit

- The four core participants in a restructured chain are the dealer, administrator, fronting carrier, and the dealer's own reinsurance entity

- How much profit returns to the dealer depends on volume, claims performance, and program structure

What Is the Reinsurance Value Chain in Auto F&I?

The reinsurance value chain in the dealer context is the end-to-end flow of premium from the retail customer through contractual and financial layers until it reaches the entity bearing the ultimate insurance risk—and collecting the profit for doing so.

The chain exists because risk needs to be priced, distributed, and held by parties with enough capital to pay claims. The premium above actual claims and expenses is underwriting profit. Whoever sits at the risk-bearing end of the chain collects it.

How This Differs From Traditional Insurance Reinsurance

The dealer F&I value chain is distinct from broad insurance industry reinsurance. Large carriers use global reinsurance treaties to manage catastrophic exposure—hurricanes, mass casualty events, systemic risks. Dealer reinsurance operates on a completely different scale, centered on high-frequency, lower-severity consumer products:

- Vehicle service contracts (VSCs) — mechanical breakdown coverage

- GAP insurance — covers the gap between loan balance and vehicle value in a total loss

- Ancillary products — tire and wheel, debt cancellation, CPI, door ding, windshield protection

These products generate predictable, manageable claims patterns. Research on extended warranty programs suggests well-managed portfolios achieve loss ratios in the 45–60% range—meaning 40–55 cents of every premium dollar is available for expenses and profit.

The question for any dealer is where in that chain they're positioned to capture it. The scale of the opportunity makes that question worth answering:

| Market | Current Size | Projected Growth |

|---|---|---|

| U.S. Auto Extended Warranty | $32.2 billion (2024, IBISWorld) | — |

| U.S. GAP Insurance | $3.5 billion | $6.4 billion |

Dealers who understand where underwriting profit accumulates — and structure their programs accordingly — are the ones positioned to capture a share of that pool rather than pass it upstream.

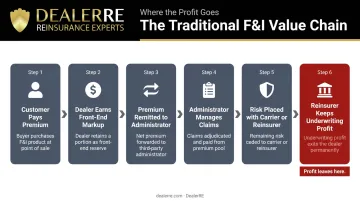

How the Traditional F&I Value Chain Works—And Where the Profits Go

In the default arrangement, the flow works like this:

- The customer pays a retail price for a VSC, GAP, or ancillary product

- The dealer earns a front-end markup—dealer reserve or participation income

- The remaining premium is remitted to a third-party administrator

- The administrator manages claims, compliance, and product fulfillment

- The administrator or product provider places the actual insurance risk with a carrier or reinsurer

- That reinsurer holds the net premium as reserves and keeps the underwriting profit when claims come in below expectations

The Layer Most Dealers Never See

The front-end markup feels like the profit. It isn't the full picture.

The underwriting profit—earned when premiums exceed claims and expenses—is captured by whoever holds the reserves. In a standard third-party arrangement, that's not the dealer. The administrator or their affiliated reinsurer keeps the surplus, along with the investment income earned on reserves held for multi-year contracts.

Per Casualty Actuarial Society research, the unearned premium reserve for auto extended service contracts is often "several times larger" than the liability for unpaid claims.

Contracts can extend up to seven years, with losses heavily back-loaded. The reserve pool is substantial—and so is the investment income it generates while claims are still emerging.

Why This Arrangement Persists

Dealers stay in this structure for three common reasons:

- Perceived complexity — Reinsurance sounds like something only large carriers understand

- Capital concerns — Assumed to require significant upfront investment

- Size assumptions — Believed to be accessible only to high-volume franchise groups

None of these assumptions hold up. The widely accepted industry minimum is approximately 20–25 F&I contracts per month to justify a standalone reinsurance entity. DealerRE works with dealers selling more than 30 cars per month—a volume many independent and BHPH operations already exceed.

Without visibility into their own claims data, dealers also have no way to evaluate whether their portfolio is profitable. They can't negotiate pricing, influence claims decisions, or access the reserves sitting idle in someone else's account. That's exactly the gap dealer-owned reinsurance is built to close.

How Dealer-Owned Reinsurance Restructures the Value Chain

When a dealer establishes their own reinsurance company, they don't leave the value chain—they move to a different position within it.

The dealer's entity steps into the downstream role: accepting reinsurance risk from a fronting carrier in exchange for receiving the unearned premium reserve. That reserve becomes a profit pool when claims are managed well.

The Admin Obligor Structure

DealerRE structures dealer-owned programs using the admin obligor (AO) model. In this structure:

- The dealer's reinsurance company becomes the contractual obligor on F&I products sold

- An A-rated fronting carrier backs the program, providing the consumer-facing regulatory wrapper

- If the dealer's entity cannot meet obligations, the fronting carrier bears the ultimate liability

- The dealer's financial exposure is bounded by the reserves generated from their own book of business—not the broader insurance market

The administrator and fronting carrier still handle product fulfillment, claims adjudication, and compliance. The dealer occupies the position in the chain where profit accumulates—without taking on the operational complexity of a standalone insurance carrier.

Three Stages of Profit Flow

Step 1 — Premium Collection and Cession

The customer pays for a VSC, GAP, or ancillary product. The dealer remits a net premium to the administrator, who cedes a portion to the dealer's reinsurance entity per the program agreement. The dealer's company now holds the reserve instead of surrendering it downstream.

Step 2 — Reserve Management and Investment

Funds are held in a U.S.-based trust account, with reserves initially invested in conservative government bonds per underwriting guidelines. Once the account balance exceeds 125% of unearned premiums, the dealer directs how accumulated funds are deployed. DealerRE clients have put those earnings to work in real estate, dealership reinvestment, and other capital priorities.

Step 3 — Claim Settlement and Profit Distribution

As claims are adjudicated and paid, losses draw from the reserve. When a contract period closes and actual claims fall below earned premium, the surplus is profit retained by the dealer's reinsurance company. It can be distributed as dividend income or held for reinvestment.

Who Participates in the Dealer Reinsurance Value Chain

Four core participants define the restructured chain:

| Participant | Role |

|---|---|

| Retail Customer | Premium origin; pays the retail price for F&I products |

| F&I Administrator | Manages product fulfillment, claims adjudication, compliance |

| Fronting Carrier (A-rated) | Regulatory wrapper; direct obligation to the customer; ultimate backstop |

| Dealer's Reinsurance Entity | Holds reserves; bears risk; collects underwriting profit |

The Role of a Program Administrator Like DealerRE

DealerRE sits outside the financial flow but enables the chain to function correctly. Founded by Tim Byrd in 1994, the company has helped over 400 dealers establish and manage admin obligor reinsurance programs—working with franchise dealers, independent dealers, and BHPH operators nationwide.

Services include:

- Setting up the dealer's reinsurance entity

- Managing all legal filings, tax returns, and annual renewals

- Claims adjudication through Assured Vehicle Protection (AVP)

- Monthly financial statements and performance reporting

- F&I training (online and in-person) to support product penetration

- Periodic ownership reviews to assess program direction

The program's tax structure is handled by insurance tax specialists. Dealers writing less than $2.2 million in annual net premiums may elect to be taxed only on investment income under IRS Code 831(b) — a meaningful tax planning advantage worth structuring for from the start.

When a Broker or MGA Is Part of the Program

Some program designs include a licensed agent or MGA between the dealer and the fronting carrier. Dealers should assess whether that layer adds genuine value—access to stronger carrier relationships, better program terms, or compliance support—or simply introduces an additional cost without improving their position in the profit flow. That question is worth raising upfront before committing to a program structure.

Common Misconceptions About the Dealer Reinsurance Value Chain

Three persistent myths keep dealers from exploring what is, for many, a straightforward profitability decision. Here's what the reality actually looks like.

"Only large franchise groups qualify."

Reality: The threshold is a function of F&I product volume, not dealership size. Many independent and BHPH dealers with disciplined F&I programs generate sufficient premium to justify their own entity. NIADA's partnership with reinsurance providers specifically extends these programs to its nearly 15,000 independent dealer members—access was never meant to be exclusive to large groups.

"Owning a reinsurance company means unlimited insurance risk."

Reality: In the admin obligor model, the dealer's exposure is capped at the premiums and reserves they control. The fronting carrier ensures customers are always protected. Financial risk is proportional to their own book of business—not the broader insurance market.

"Setting up a reinsurance company means building a claims team from scratch."

Reality: The administrator and fronting carrier still handle day-to-day operations. The dealer doesn't become an insurance company operator—they become the entity that holds reserves and keeps the profit.

Frequently Asked Questions

What is the value chain in insurance?

The insurance value chain is the sequence of participants—policyholder, agents, carriers, and reinsurers—where each party adds a service, bears a share of risk, and earns a portion of the premium. In auto F&I, that chain runs from the car buyer through the dealer, administrator, and insurer to the reinsurer who holds the final underwriting profit.

How does dealer-owned reinsurance fit into the F&I value chain?

Dealer-owned reinsurance places the dealer's entity at the downstream end of the chain, where net premiums are held as reserves and converted to profit when claims fall below expectations. Without this structure, a third-party provider occupies that position and keeps the profit.

What is an admin obligor reinsurance structure for auto dealers?

In an admin obligor structure, the dealer's reinsurance company is required by contract to pay F&I product claims, backed by an A-rated fronting carrier that handles regulatory compliance. This allows the dealer to hold premium reserves and earn underwriting profit without requiring a full insurance company license.

How much profit can a dealer realistically expect from a reinsurance program?

Profit depends on F&I product volume, claims frequency, and F&I team performance. The profit pool is the same underwriting margin third-party providers were previously retaining—the structure simply determines who keeps it.

What F&I products can be included in a dealer reinsurance program?

Most programs can include a wide range of products, each generating premium that can be ceded to the dealer's reinsurance entity:

- Vehicle service contracts and limited warranties

- GAP insurance and debt cancellation coverage

- Collateral protection insurance (CPI)

- Tire and wheel, door ding, and windshield repair protection

- Vendor single interest (VSI) coverage

How is dealer-owned reinsurance different from a standard third-party F&I program?

In a third-party program, the dealer earns only the front-end markup while the provider retains underwriting profit. In a dealer-owned program, the dealer's reinsurance entity receives the net premium and keeps that profit directly. The dealer stops being just a seller in the value chain and becomes the owner of its most profitable position.