The practical distinction matters most here: one model transfers risk externally after a policy is issued; the other splits risk among multiple insurers at the point of origination. Neither involves the dealer capturing underwriting profits — unless the dealer structures their own reinsurance company.

This article covers clear definitions of both models, a side-by-side comparison, and a focused look at which structure creates the most financial leverage for auto dealerships.

TL;DR

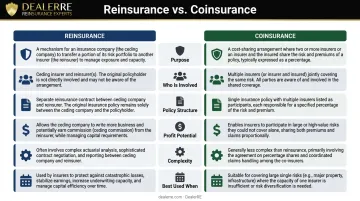

- Reinsurance is a back-end risk transfer between two insurance companies — invisible to the policyholder

- Coinsurance splits a single policy's risk across multiple insurers at origination — all carriers are visible to the insured

- For auto dealers, the relevant structure is reinsurance — specifically dealer-owned reinsurance, which allows dealers to capture underwriting profits rather than cede them to third-party providers

- F&I gross profit averaged $2,505 per vehicle in Q1 2025 — profit that flows to third-party providers when dealers have no participation structure

- Coinsurance is designed for large commercial risks, not dealer profit retention

Reinsurance vs Coinsurance: Quick Comparison

| Dimension | Reinsurance | Coinsurance |

|---|---|---|

| Purpose | Protects a primary insurer from excess losses by transferring risk to a second insurer | Distributes a single large risk across multiple insurers from the start |

| Who Is Involved | Primary insurer and reinsurer; policyholder has no direct relationship with the reinsurer; reinsurer is invisible to them | Two or more insurers and the insured; all carriers are visible to the insured |

| Policy Structure | Separate back-end agreement between insurers; original policy remains intact | Single policy shared among carriers, each covering their defined percentage |

| Profit Potential | Underwriting profits accrue entirely to the reinsurer | Premiums and profits are split proportionally; no single party captures full underwriting gain |

| Complexity | More complex to structure; offers greater financial leverage and control | Simpler to set up; spreads both risk and reward, limiting individual upside |

| Best Used When | A single insurer needs back-end protection after issuing a policy | Multiple insurers share a risk from policy inception |

What Is Reinsurance?

The Insurance Information Institute defines reinsurance as "insurance for insurance companies" — a transaction where a primary insurer (the cedant) transfers a portion of its risk and premium to a reinsurer in exchange for protection against large or unexpected claims. The original policyholder's coverage is unaffected; they never know the arrangement exists.

Treaty vs. Facultative Reinsurance

Two primary structures exist:

- Treaty reinsurance automatically covers all risks within a defined category — for example, all vehicle service contracts written by a particular carrier. No case-by-case negotiation is required.

- Facultative reinsurance is negotiated individually for specific, high-value, or unusual risks that fall outside standard treaty coverage.

Dealer-owned reinsurance programs operate on treaty-like principles, automatically covering classes of F&I products sold at the dealership.

Why Reinsurance Creates Financial Leverage

For the reinsuring party, the model unlocks three strategic advantages:

- Frees up capital by offloading risk to the reinsurer

- Enables coverage of policies that would otherwise exceed single-carrier capacity

- Retains underwriting surplus when claims come in below reserves — the core profit driver for dealer-owned programs

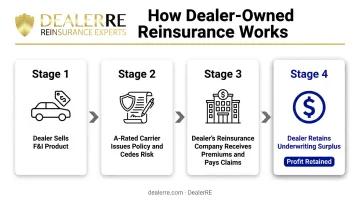

The Dealer-Owned Reinsurance Model

Auto dealers can establish their own reinsurance companies — typically structured as an admin obligor arrangement — to reinsure the F&I products they sell. Vehicle service contracts, GAP, collateral protection, and ancillary products like tire and wheel or debt cancellation coverage all qualify.

Under this structure, the dealer's reinsurance company receives ceded premiums from an A-rated carrier, pays claims from reserves, and retains the underwriting surplus. Profits that previously flowed to third-party administrators stay with the dealership instead.

DealerRE has helped over 400 dealers establish and manage these programs since 1994, handling legal filings, tax returns, claims adjudication, and ongoing training.

Reinsurance in Practice

Broad insurance industry: Large insurers use reinsurance to absorb catastrophic losses that no single carrier could sustain. In 2024, global insured losses from natural disasters reached $140 billion — the third-costliest year since 1980. The $400 billion global reinsurance market exists specifically to spread that kind of exposure.

Auto dealer context: The scale is different, but the mechanism is identical. A dealer sells an F&I product; the underlying A-rated insurer cedes the risk to the dealer's reinsurance company; the dealer's company collects premiums, pays claims, and retains surplus. The vehicle service contract market alone exceeded $32 billion in 2024, growing toward $49.85 billion by 2032 — that's the pool from which dealer reinsurance profits are drawn.

What Is Coinsurance?

Coinsurance is a risk-sharing arrangement where two or more insurers collectively cover a single policy. Each carrier is directly liable to the policyholder for their pre-agreed percentage of any claim.

Unlike reinsurance, the split is established at the front end — before or at policy issuance — and all participating carriers are visible to the insured.

Proportional vs. Non-Proportional Coinsurance

| Type | How It Works |

|---|---|

| Proportional | Each insurer pays their exact percentage of every claim. A carrier holding 30% of the risk pays 30% of every loss. |

| Non-proportional | Each insurer covers losses up to a defined threshold, beyond which exposure shifts to the next layer — unlike reinsurance's back-end excess-of-loss structure. |

The quota-share concept applies to both: each carrier's share of premium and liability is defined upfront, with no ambiguity about who owes what when a claim arrives.

When Coinsurance Makes Sense

Coinsurance is designed for risks too large for any single insurer to carry alone. The Lloyd's of London subscription market is the best-known example — multiple syndicates each underwrite a percentage of a single risk on a single policy, with a lead underwriter setting terms.

Common applications include:

- Large commercial real estate portfolios

- Aviation hull and liability coverage

- Marine cargo on high-value shipments

- Major infrastructure or energy projects

Coinsurance in the Dealer Context

For auto dealers, coinsurance is irrelevant to F&I program strategy. Here's why it doesn't apply:

- Vehicle service contracts and GAP policies don't present risks large enough to require pooled carrier capacity

- Coinsurance offers no mechanism for a dealer to own the risk entity

- There's no path to capturing residual underwriting profits — the core financial advantage of dealer-owned reinsurance

Key Differences Between Reinsurance and Coinsurance

Risk Transfer vs. Risk Sharing

Reinsurance moves risk from a primary insurer to a separate party after the policy is issued. Coinsurance divides risk among multiple parties at policy origination. This structural difference determines who holds the financial upside.

In reinsurance, the reinsurer (which can be a dealer-owned entity) sits in the profit position. In coinsurance, profits are split proportionally with no individual party capturing full underwriting gain.

Policyholder Visibility

- Reinsurance: The policyholder contracts with one insurer only. The reinsurance arrangement is a separate agreement between insurers — the customer submits claims to their original insurer and has no awareness of what happens behind the scenes.

- Coinsurance: The policyholder may have contractual relationships with multiple carriers and often must deal with each separately when filing claims. This adds complexity for the insured.

Profit and Loss Dynamics

In reinsurance, underwriting profits (excess premium over claims) accrue entirely to the reinsurer. A dealer-owned reinsurance company captures that full margin. In coinsurance, profits are distributed proportionally — no single party retains the complete underwriting gain.

That distinction carries real financial weight. F&I accounted for 28.4% of total dealership gross profit in Q1 2025, up from 26.4% the previous quarter. As front-end vehicle margins compress, the underwriting profit embedded in F&I products represents a growing revenue line — and reinsurance is the structure that lets dealers keep it.

Regulatory Framework

Understanding the profit structure also means understanding the compliance layer that governs it. Two key frameworks apply to dealer-owned reinsurance:

- NAIC Credit for Reinsurance Model Law (#785): Revised in 2019 and implemented across all 56 U.S. jurisdictions, this governs how ceding companies take financial statement credit for reinsured risk.

- IRC 831(b): Dealer-owned reinsurance programs structured under this provision operate within a well-established legal framework with clear compliance requirements.

Coinsurance arrangements fall under standard insurance regulation and don't involve the reinsurance-specific compliance infrastructure that dealer programs navigate.

Which Model Works Best for Auto Dealers?

For most dealers, coinsurance isn't the operative question. It's a commercial insurance mechanism designed for risks that require multiple carriers pooling capacity — aircraft, mega-properties, marine cargo. That's not F&I.

The real decision is simpler: do you send underwriting profits to a third-party provider, or do you keep them?

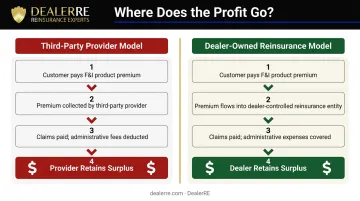

The Third-Party Provider Problem

When a dealer sells a vehicle service contract through a third-party administrator, the profit structure looks like this:

- Dealer earns a flat commission on the sale

- Premium flows to the third-party provider

- Provider pays claims from reserves

- Provider retains the surplus — the underwriting profit

Consider the logic directly: if your third-party warranty provider weren't making a profit from your customers' policies, why would they continue doing business with you?

The Dealer-Owned Reinsurance Alternative

Under a dealer-owned reinsurance structure, the same transaction works differently:

- Dealer sells the F&I product and earns the same back-end gross profit

- The A-rated carrier issues the policy and cedes risk to the dealer's reinsurance company

- Dealer's reinsurance company receives premiums, pays claims, and retains the surplus

- Surplus can be reinvested in the dealership, used for tax planning under IRC 831(b), or deployed into other assets

Dealers around the country have captured hundreds of thousands of dollars in underwriting profits that previously went to third-party providers. With F&I generating over $2,500 per vehicle at publicly traded dealer groups, a mid-volume dealer moving 75–100 units per month is leaving a substantial profit stream on the table.

Consumer protection is maintained throughout this structure. The A-rated carrier backstops all obligations, so if the dealer's reinsurance company faces financial pressure, the ultimate claim liability stays with the carrier.

Getting Started

That profit opportunity doesn't materialize on its own. Setting up a dealer-owned reinsurance company requires specific legal structure, compliance management, and program administration. DealerRE handles all of it: legal filings, tax returns (IRC 831(b) structures), claims adjudication through their administrator partner, and ongoing F&I training for dealer staff.

If you're evaluating whether a dealer-owned reinsurance program fits your dealership, contact DealerRE to discuss your specific volume, product mix, and financial goals.

Frequently Asked Questions

Is coinsurance the same as reinsurance?

No. Coinsurance splits risk among multiple insurers on a single policy at origination — all carriers share premiums and liability proportionally from day one. Reinsurance transfers risk from one insurer to a separate reinsurer after the policy is issued, in a back-end agreement the policyholder never sees.

How is reinsurance different from regular insurance?

Insurance covers policyholders against loss. Reinsurance is insurance for insurance companies — it protects the primary insurer from excess claims on the policies it has already issued. The policyholder is unaware of and unaffected by any reinsurance arrangement.

What is dealer-owned reinsurance?

Dealer-owned reinsurance is a structure where an auto dealer establishes their own reinsurance company to reinsure the F&I products — vehicle service contracts, GAP, CPI, ancillary products — sold at their dealership. Instead of those underwriting profits flowing to a third-party provider, they accrue to the dealer's own company.

What are the main types of reinsurance?

Treaty reinsurance automatically covers all risks within a defined category (such as all service contracts written by a carrier), while facultative reinsurance is negotiated case-by-case for individual risks. Both types can be structured as proportional — shared percentages of premium and loss — or non-proportional, where the reinsurer covers losses above a set retention threshold.

Can auto dealers actually profit from their own reinsurance company?

Yes — dealers retain underwriting profits when claims fall below reserves, earn investment income on held reserves, and access tax planning advantages under IRC 831(b) for companies under $2.2 million in annual net premiums. Proper structure and administration are essential for compliance, which is why program administrator selection matters.