For dealer principals operating their own admin obligor reinsurance companies through programs like those administered by DealerRE, this isn't abstract accounting theory. VSC mechanical breakdown claims, GAP total loss events, and CPI losses all create real dollar flows between the dealer's reinsurance company and the backing carrier. Knowing how to read, calculate, and manage those flows directly affects how much underwriting profit stays in the dealer's company.

This guide covers what reinsurance recoverables are, the main types, how to calculate them, and why they matter — with specific context for dealer-owned reinsurance programs.

TL;DR

- Reinsurance recoverables are amounts a ceding insurer expects to recover from a reinsurer after paying covered claims

- They appear as assets on the primary insurer's balance sheet and liabilities on the reinsurer's

- Four types: paid claims, reported-but-unpaid losses, IBNR, and unearned premium recoverables

- Core formula: Reinsurance Recoverable = Total Claims Paid – Retention Amount

- Over-reliance creates counterparty credit risk if the reinsurer defaults

What Are Reinsurance Recoverables?

A reinsurance recoverable is the amount a primary (ceding) insurer expects to collect from a reinsurance company for covered losses and related costs, based on the terms of a reinsurance contract. Two parties define this relationship: the ceding insurer, who originally underwrote the risk and paid the claim, and the assuming reinsurer, who agreed to cover a portion of that risk in exchange for a share of the premiums.

Balance Sheet Treatment

The accounting is asymmetrical by design:

- Ceding insurer: records recoverables as assets — money is owed to them

- Assuming reinsurer: records the same amounts as liabilities — they may have to pay

Both GAAP and statutory accounting principles confirm this dual treatment, per NAIC Statutory Issue Paper No. 75, which states that "reinsurance recoverables on paid losses and loss adjustment expenses are reported as an asset under both statutory accounting and GAAP." In some arrangements, primary insurers require collateral from reinsurers before recognizing recoverables as admitted assets.

Recoverables vs. Receivables

These terms are often used interchangeably. "Reinsurance recoverables" is the broader term encompassing all amounts owed by reinsurers — paid losses, unpaid losses, IBNR, and unearned premiums. "Reinsurance receivables" sometimes refers more narrowly to billed, collectible amounts. In practice, both terms appear across financial statements and regulatory filings, often referring to the same underlying balances.

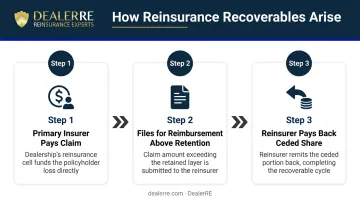

How Recoverables Arise

The process follows a clear sequence:

- The primary insurer pays a claim to the policyholder

- It files for reimbursement from the reinsurer for the portion above its retention threshold

- The reinsurer pays back that share, restoring the primary insurer's capital position

This allows insurers to underwrite more policies without exhausting capital reserves — large or unexpected losses get partially absorbed by the reinsurance layer rather than hitting the ceding insurer's balance sheet alone.

Types of Reinsurance Recoverables

Not all recoverables are created equal. They vary by certainty level, timing, and how they're estimated.

| Recoverable Type | Description | Certainty Level |

|---|---|---|

| Paid claims recoverables | Amounts already disbursed to policyholders, now billed to reinsurer | Highest — amounts known and billed |

| Reported but unpaid | Filed claims with estimated amounts, not yet settled | Moderate — claim known, amount uncertain |

| IBNR recoverables | Losses incurred but not yet formally reported | Lowest — requires actuarial estimation |

| Unearned premium recoverables | Premiums recoverable on cancelled or lapsed policies | Deterministic — based on contract terms |

Paid Claims Recoverables

The insurer has already paid the policyholder and is now seeking reimbursement from the reinsurer for the ceded portion. The amount is known, billed, and tracked until the reinsurer pays — making this the most straightforward recoverable category to manage.

Reported but Unpaid Loss Recoverables

A claim has been filed and the insurer has set a case reserve — an estimated dollar amount for what the claim will cost — but hasn't paid it yet. The recoverable is calculated based on the ceded share of that reserve.

IBNR Recoverables

Incurred But Not Reported losses are the most complex category. These are losses that have already occurred but haven't yet surfaced as filed claims. For F&I products, IBNR is significant: VSC claims develop over multi-year contract terms, and GAP claims depend on two triggering events (total loss declaration plus a deficiency between loan balance and insurance settlement). CAS actuarial research on GAP insurance documents expected loss ratios of 80–90% with claim frequency around 1.19% — meaning IBNR recoverables can be the largest single category on a dealer-owned reinsurer's balance sheet at any point in time.

The three categories above all involve loss events. The fourth type works differently — it's about premiums, not claims.

Unearned Premium Recoverables

When a reinsurance contract is cancelled or an underlying policy lapses, the primary insurer may recover the unearned portion of premiums already paid to the reinsurer. The unearned premium reserve is the share of collected premiums not yet earned by covering the remaining policy period. This becomes relevant during program restructuring or mid-term cancellations.

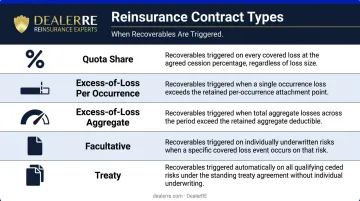

How Contract Type Shapes Recoverables

Understanding which recoverable types appear — and how large they'll be — depends heavily on the reinsurance structure in place:

- Quota share: Every claim generates a proportional recoverable from dollar one

- Excess-of-loss (per occurrence): Recoverables only arise when an individual claim exceeds the retention threshold

- Excess-of-loss (aggregate): Recoverables begin after cumulative losses exceed an annual aggregate deductible

- Facultative: Risk-specific placements with recoverables tied to identified policies

- Treaty: Blanket coverage generating recoverables systematically across the covered book

For dealer-owned reinsurance programs, quota share is the dominant structure — which means all four recoverable types are typically active simultaneously, each requiring its own tracking and estimation approach.

How to Calculate Reinsurance Recoverables

The Core Formula

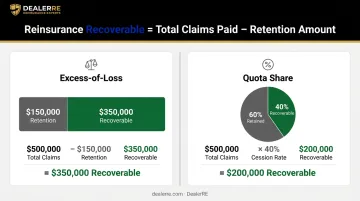

Reinsurance Recoverable = Total Claims Paid by the Insurer – Retention Amount

Each variable has a precise meaning:

- Total Claims Paid: The full amount disbursed to policyholders for covered losses

- Retention Amount: The threshold the primary insurer is responsible for before the reinsurer steps in

Worked Example

A dealer's reinsurance company covers VSC mechanical breakdown claims. Over a period, it pays $500,000 in total claims. The retention amount under the reinsurance agreement is $150,000.

Reinsurance Recoverable = $500,000 – $150,000 = $350,000

That $350,000 flows back to the dealer's reinsurance company from the backing carrier — restoring capital and preserving underwriting profit.

For a quota share structure, the math is different: if the dealer's company ceded 40% of premiums and losses, the recoverable on that same $500,000 in claims would be $200,000 (40% × $500,000), regardless of any per-claim threshold.

Those examples assume clean, single-layer structures. Most active dealer programs don't work that way.

Complicating Factors in Practice

In practice, several variables can shift the final recoverable figure:

- Multiple reinsurance layers: A program may have a per-occurrence excess layer stacked above an aggregate layer, each with separate recoverables

- Co-insurance provisions: Where the primary insurer retains a percentage of losses above the retention

- IBNR uncertainty: Actuarial estimates introduce variability into total recoverable figures — especially for long-tail products like VSCs

- Aggregate vs. per-occurrence structures: Aggregate deductibles require tracking cumulative loss experience before any recoverable is triggered

The Retention Level Decision

Retention level isn't just a calculation input — it's a core program design choice. A lower retention means more of each claim is recoverable from the reinsurer, which limits downside exposure but also limits how much premium profit stays in the dealer's company. A higher retention keeps more risk (and more profit potential) with the primary insurer.

Setting the right retention means analyzing claim frequency, average severity, and the dealer's realistic capacity to absorb a bad loss year — then stress-testing those assumptions before the program launches.

Retention design is closely tied to how recoverable balances are treated on the books — which brings in a separate accounting requirement.

CECL and Expected Credit Losses

Under ASC 326-20 (the CECL standard), GAAP filers must measure expected credit losses on reinsurance recoverables, even when credit risk is considered remote.

This means setting an allowance against recoverable balances based on the reinsurer's financial strength, collateral arrangements, and historical loss experience. For dealer-owned programs where the backing carrier is unrated, individual credit assessments may be required rather than portfolio-level pooling.

Why Reinsurance Recoverables Matter

Financial Stability

Recoverables prevent large claim events from depleting the primary insurer's capital reserves. Without them, a single high-severity loss period could impair an insurer's ability to continue underwriting new policies. For dealer-owned reinsurance companies, this is especially relevant — VSC programs can see claim costs spike on older, high-mileage vehicles, and having a reinsurance layer that generates recoverables keeps the program solvent through those cycles.

Liquidity and Cash Flow

When reinsurers pay on recoverables promptly, they restore cash flow to the primary insurer. The risk isn't always whether a recoverable is valid — it may be contractually guaranteed — but whether delays in collection create short-term liquidity stress. Dealers operating reinsurance programs should track outstanding recoverable balances alongside their trust account positions for a complete liquidity view.

Profit Protection for Dealer-Owned Programs

Recoverables are most directly relevant to program economics in dealer-owned structures. In DealerRE's admin obligor model, the dealer's reinsurance company retains all underwriting profit from the F&I products it covers. Recoverables flow back into that company when losses exceed the retention threshold, protecting the profit base.

F&I products now represent 25% of total dealership gross profit according to research from Colonnade Advisors — up from 15% in 2009. That financial weight makes accurate recoverable tracking critical. DealerRE's monthly statements cover claims adjudication, financial reporting, and performance analysis, giving dealers and their advisors a clear view of true program profitability rather than an incomplete snapshot.

Risks and Limitations of Reinsurance Recoverables

Recoverables are assets, but they're contingent ones. Understanding where they can lose value is essential to managing them.

Counterparty Credit Risk

A recoverable is only worth what the reinsurer can actually pay. If a reinsurer becomes insolvent or financially impaired, the primary insurer may collect nothing — or significantly less than the balance on their books.

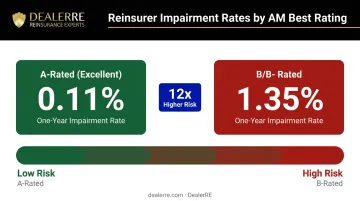

AM Best's data quantifies how much rating category matters: A-rated (Excellent) reinsurers show a one-year impairment rate of just 0.11%, compared to 1.35% for B/B- rated entities. That's a 12x difference in failure probability. DealerRE's carrier partners carry A ratings, which narrows — though doesn't eliminate — this risk.

For captive reinsurers (including dealer-owned companies), NAIC Model Law 785 governs whether recoverables ceded to them can be recognized as admitted assets. Unrated captives typically must collateralize their obligations through trust accounts rather than relying on rating-based credit, making trust fund adequacy the operative constraint.

Dispute Risk

Credit risk and dispute risk are different problems. Credit risk is about inability to pay; dispute risk is about unwillingness — where a reinsurer challenges whether specific claims fall within contract terms, delaying or reducing recovery.

Under CECL accounting standards, dispute risk is treated separately — it doesn't appear in the allowance for credit losses. It still affects real-world collectability and can create cash flow timing problems.

Over-Reliance Risk

A program structured to depend heavily on reinsurance recoverables faces structural vulnerability if the reinsurer changes contract terms, increases pricing, or exits the relationship. When that happens, the consequences for an underprepared primary insurer include:

- Gaps in reserve coverage during contract transitions

- Forced renegotiation from a position of dependency

- Exposure to pricing increases with no viable alternative

Reinsurance Recoverables in Dealer-Owned Programs

How the Structure Works

When DealerRE establishes an admin obligor reinsurance company for a dealer, the dealer's company functions as the primary insurer — issuing F&I products across multiple categories:

- Vehicle service contracts (VSCs) and extended warranties

- GAP and debt cancellation coverage (DCC)

- Collateral protection insurance (CPI)

- Ancillary products like tire and wheel and windshield coverage

An A-rated carrier provides the backing layer. Any losses above the dealer company's retention that are covered by the carrier layer become recoverables flowing back into the dealer's program.

This structure means dealers both bear claim costs and benefit from tracking recoverables. Unlike a traditional third-party F&I arrangement — where the warranty company keeps all underwriting profit — the admin obligor model puts both the risk and the reward inside the dealer's own company.

Why Recoverable Tracking Affects Program Profitability

Dealers who don't actively monitor their recoverable position may underestimate actual program performance — or overestimate it if they're counting as profit dollars that haven't yet been collected from the carrier.

DealerRE's administration through AVP (Assured Vehicle Protection) includes monthly financial statements covering all reinsurance operations, claims adjudication, and periodic management reviews. That reporting infrastructure is what makes accurate recoverable tracking possible, so dealers can measure actual retained underwriting profit — not just gross premium collected.

Making Smarter Structural Decisions

That visibility directly shapes program design going forward. Knowing how much of the claim dollar comes back from the carrier layer — and how quickly — helps dealers and their advisors make better decisions about retention levels, product mix, and program structure as the program matures.

Frequently Asked Questions

What is a reinsurance recovery?

A reinsurance recovery is the amount a primary insurer actually collects from a reinsurer after paying claims that exceed its retention threshold. It's the realized version of a reinsurance recoverable — the money that actually arrives, based on the terms of the reinsurance agreement.

What is reinsurance in simple terms?

Reinsurance is insurance for insurance companies. A primary insurer transfers a portion of its risk to a reinsurer in exchange for sharing a portion of premiums, protecting the primary insurer from catastrophic or outsized losses it couldn't absorb alone.

What is the difference between reinsurance recoverables and reinsurance receivables?

The terms are largely interchangeable. "Recoverables" is the broader accounting term covering all amounts owed by reinsurers — paid claims, unpaid claims, IBNR, and unearned premiums. "Receivables" is balance sheet language that sometimes refers more narrowly to billed, collectible amounts.

How do reinsurance recoverables appear on a balance sheet?

Recoverables appear as assets on the ceding insurer's balance sheet and as liabilities on the reinsurer's — representing amounts owed in one direction and obligations to fulfill in the other.

What types of contracts generate reinsurance recoverables?

Quota share, excess-of-loss, facultative, and treaty contracts all generate recoverables. The common requirement is that the contract obligates the reinsurer to reimburse some portion of the primary insurer's covered losses.

What risks are associated with reinsurance recoverables?

The primary risks are reinsurer insolvency (counterparty credit risk), contractual disputes over coverage, collection delays that strain short-term liquidity, and over-reliance on recoverables in place of adequate independent reserves. AM Best ratings help screen for credit risk, but reviewing financial strength ratings alongside contract terms gives the most complete picture.