Quota share reinsurance is the mechanism that changes this. It's a proportional arrangement where a fixed percentage of premiums, losses, and underwriting profits are shared between parties — rather than sending all profits to a third-party provider.

This article is written for franchise dealers, independent dealers, and BHPH dealers who sell F&I products and want to understand how quota share reinsurance works, what it does mechanically, why dealers use it, and when it may not be the right fit.

TL;DR

- Quota share reinsurance splits premiums and claims at a fixed percentage between the insurer and the dealer's captive entity.

- Instead of earning only a commission, dealers capture underwriting profits — the money remaining after claims are paid — inside their own entity.

- Covered products typically include VSCs, GAP insurance, tire and wheel, windshield repair, door ding protection, and theft protection.

- Unlike excess-of-loss structures, quota share uses a fixed sharing ratio that applies uniformly across every covered product sold.

- Actual returns depend on sales volume, claims experience, and how the program is structured from the start.

What Is Quota Share Reinsurance?

Quota share reinsurance is a type of proportional reinsurance where a fixed percentage of premiums and losses from a defined policy portfolio is shared between two parties: the primary insurer (or administrator) and the reinsurer (the dealer's captive entity). Both sides share results at the same rate, on every covered policy.

According to the NAIC's Regulator's Introduction to the Insurance Industry, in a quota share treaty, "the assuming and ceding insurers share losses and premiums according to a fixed, agreed-upon proportion." In a 50% quota share, each party covers half of every loss — no exceptions, no thresholds.

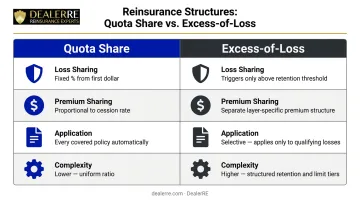

How It Differs from Excess-of-Loss

The key distinction comes down to when risk-sharing activates:

| Feature | Quota Share | Excess-of-Loss |

|---|---|---|

| Loss sharing | Fixed % from first dollar | Only above a retention threshold |

| Premium sharing | Proportional to cession rate | Fee-based for coverage layer |

| Application | Every covered policy automatically | Triggered only when loss exceeds limit |

| Complexity | Lower — uniform ratio applies | Higher — requires per-loss threshold tracking |

For dealers entering reinsurance for the first time, quota share's fixed-rate structure is more predictable. Excess-of-loss has its place, but the math is less straightforward. That predictability is exactly what makes quota share the more common entry point — and it shapes the financial outcome directly.

The Core Outcome

The dealer's reinsurance company receives a predetermined share of premium income from every F&I product sold. In return, it takes on that same proportional share of claims. When claims run lower than premiums collected over time — which is the normal pattern for a well-managed F&I book — the dealer retains the underwriting profit instead of passing it to a third-party provider.

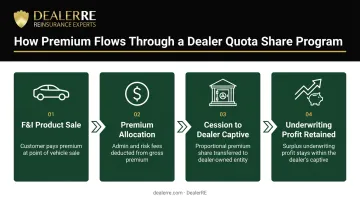

How Quota Share Reinsurance Works for Auto Dealers

The end-to-end flow starts at the point of sale and ends with underwriting profit — or loss — sitting inside the dealer's own entity. Each stage below shows exactly how premium moves, where risk transfers, and when profit accrues.

Step 1: Customer Purchases an F&I Product

A customer in the F&I office elects to purchase a vehicle service contract, GAP insurance, or another covered protection product. The customer's premium flows through the dealership to the administrator. Without a completed sale, there's no cession and no reinsurance event.

Step 2: Premium Allocation and Cession

The total premium doesn't flow to the reinsurance entity in full. It's first broken down:

- Administrative costs — fees for program management and contract administration

- Risk management fees — charges retained by the primary insurer

- Reserve contributions — funds set aside to pay future claims

The net underwriting exposure is then ceded to the dealer's reinsurance captive at the agreed quota share percentage. This cession is the mechanism that moves both the risk and the profit potential from the third-party administrator into the dealer's entity.

Plain-dollar example: On a $1,500 VSC premium with a 60% quota share, the dealer's captive receives $900. If a $2,000 claim is filed on that contract, the captive pays $1,200. If claims run light across the book, the remaining reserves accumulate as underwriting profit.

Step 3: Reserves, Claims, and Underwriting Profit

The dealer's captive holds reserves to fund its proportional share of claims over the life of the contracts. As claims come in, the captive covers its share. Over time, if the book performs well:

- Reserves exceed claims paid

- The surplus becomes underwriting profit

- That profit stays inside the dealer's entity

DealerRE structures dealer programs using an admin obligor model, where the dealer's reinsurance entity is backed by A-rated insurers. If the captive cannot meet its obligations, the direct writing insurance company carries the ultimate liability — protecting the dealer while still allowing full participation in underwriting profits.

All funds are held in a U.S.-based trust account, not sent offshore.

Why Auto Dealers Use Quota Share Reinsurance

F&I now represents up to 73% of total dealership profit, according to VisionAST's 2025 analysis of 202 dealerships — up from 56% just one year prior. Dealers running on a commission-only model are earning a fraction of what their F&I department actually generates, while the administrator captures the rest.

Quota share reinsurance changes that math in four meaningful ways.

Underwriting Profit Capture

Under a traditional commission arrangement, the dealer earns a flat fee per product sold. The administrator retains the underwriting profit — the spread between premiums collected and claims paid — plus any investment income on held reserves.

Quota share redirects that profit into the dealer's own captive. The amount captured varies by product type, claims experience, and program terms. Dealers who own a proportional share of results participate in favorable loss years instead of watching that income flow elsewhere.

Countercyclical Income

Reinsurance profits aren't tied to this month's vehicle sales volume. Reserves and underwriting profit accumulate over the life of previously sold contracts — meaning a slow sales period doesn't stop the captive from generating returns on an already-established book. This makes quota share income a useful counterweight to the volatility of front-end margins.

Customer Experience Control

When the dealer owns the reinsurance captive and retains underwriting risk, claims handling is no longer entirely in a third party's hands. Dealers can ensure claims are resolved in ways that protect the customer relationship and drive repeat business — rather than having a distant administrator make decisions that may frustrate customers at the worst moment.

Tax Planning and Wealth Accumulation

Premiums that accumulate inside the dealer's captive entity can be invested and grown in a tax-advantaged environment. For example, a CFC making an IRC Section 831(b) election may be taxed only on investment income — not on premium income — up to the annual threshold, which is $2.8 million for 2025.

Important: Specific tax treatment depends entirely on entity structure, domicile, elections made, and individual circumstances. Dealers must consult a qualified tax advisor before making any decisions.

Retained earnings in the captive also build a separate asset base over time. Dealers commonly use those funds to support:

- Generational wealth transfer and estate planning

- Retirement funding outside the dealership's balance sheet

- Buy-sell arrangements between partners or successors

This positions the captive as a long-term financial planning vehicle, not just an incremental revenue line.

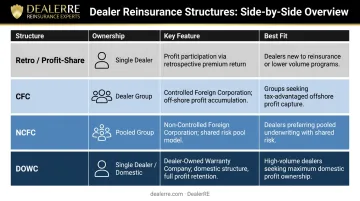

Quota Share vs. Other Dealer Reinsurance Structures

Quota share is not an entity type — it's a profit-sharing mechanism applied within a reinsurance structure. Understanding the entity types helps clarify what quota share actually fits inside.

The Four Common Dealer Reinsurance Structures

| Structure | Ownership | Key Feature | Best Fit |

|---|---|---|---|

| Retro / Profit-Share | No entity formed | Contractual profit-share with administrator | Smaller dealers testing the concept |

| CFC | Single dealer/group | Offshore domicile; 831(b) eligible | Small to mid-size dealers wanting direct control |

| NCFC | 11+ unaffiliated dealers | Pooled ownership; tax-deferred until distribution | High-volume dealers seeking scale |

| DOWC | Single dealer/group | Domestic domicile; full obligor risk | Large, sophisticated dealer groups |

Quota Share vs. Retro Arrangements

A retro (profit-sharing) arrangement is a contractual agreement with the administrator — the dealer receives a portion of favorable results without forming their own captive. No entity formation, no compliance management, no upfront capital commitment.

The tradeoffs are worth mapping out directly:

- Retro: Lower complexity, no entity to manage, profit-share paid at the administrator's discretion

- Quota share in a captive: Direct ownership of the reserve pool, investment control, higher long-term accumulation potential — with more compliance to manage

- Key difference in control: With retro, the administrator defines what "favorable results" means and when you get paid. With your own captive, the reserve pool is yours from day one.

For dealers with enough volume to justify the structure, a dealer-owned captive with quota share typically outperforms a retro arrangement over time — the dealer owns the full profit pool rather than receiving a contractual slice of it.

Common Misconceptions and Limitations

"This Is Primarily a Tax Shelter"

It isn't. The core function of quota share reinsurance is legitimate risk-sharing and profit retention — the tax structure is a component of program design, not the purpose. Today's programs are highly regulated, and reputable administrators like DealerRE handle all filings, tax returns, licensing, and renewals as part of their service.

The January 2025 IRS final regulations, which introduced a Seller's Captive exception for dealer F&I programs, clarified the compliance landscape significantly, but the requirements (including 95% unrelated customer risk) must be actively maintained.

"Any Dealer Can Benefit Equally"

Volume matters. Reserve accumulation and underwriting profit are directly tied to how much premium flows through the program. One reinsurance program administrator suggests the structure becomes practical around 20–25 service contracts per month, though this varies by product mix, average premium size, structure type, and administration costs. DealerRE typically works with dealers selling more than 30 vehicles per month, using a personalized business analysis to evaluate fit rather than a single universal threshold.

"It's Guaranteed Passive Income"

This one can get dealers into trouble. Because the captive takes on a proportional share of claims, a period of abnormally high losses reduces or eliminates underwriting profit. This is real underwriting risk. Sustainable results depend on:

- Selecting products with sound loss histories

- Maintaining claims management discipline

- Keeping reserves adequately funded

Dealers who enter quota share expecting guaranteed returns without active program oversight typically see those expectations fall short.

Frequently Asked Questions

What is quota share reinsurance?

Quota share reinsurance is a proportional agreement where a fixed percentage of premiums and losses from an insurance policy portfolio is shared between the primary insurer and the reinsurer. In the auto dealer context, the reinsurer is typically the dealer's own captive entity — meaning the dealer participates directly in underwriting results.

What F&I products are typically covered under a dealer quota share reinsurance program?

Vehicle service contracts, GAP insurance, and ancillary products are the most common. DealerRE's programs cover VSCs, GAP, tire and wheel protection, windshield repair, door ding protection, and theft protection, among others. Product eligibility depends on the program structure and administrator.

How is quota share reinsurance different from a profit-sharing (retro) arrangement?

A retro is a contractual profit-share with the third-party administrator — no captive entity required, but also no direct ownership of the reserve pool. Quota share within a dealer-owned captive gives the dealer full ownership of reserves, investment control, and typically higher long-term profit potential, with more setup and compliance to manage.

What percentage is typically used in a dealer quota share reinsurance agreement?

Cession percentages vary by program, product type, risk profile, and administrator. There is no universal industry standard. The appropriate percentage should be determined through a program analysis with a qualified reinsurance manager — not assumed from published benchmarks.

Do dealers need a minimum sales volume to make quota share reinsurance worthwhile?

Yes — volume matters because reserve accumulation is directly tied to premium flow. Dealers with very low F&I product penetration may not generate enough premium to offset startup and ongoing administration costs. A dealership analysis is the standard first step in determining whether a quota share program is worth pursuing.

Who manages the compliance and administration of a dealer quota share reinsurance program?

DealerRE manages all legal forms, filings, tax returns, and renewals on behalf of its dealer clients — including claims adjudication and performance reporting. The company partners with specialized CPAs and legal counsel to maintain ongoing compliance under IRS Code 831(b) and applicable state regulations.