Whether you're in risk management, insurance underwriting, or running an auto dealership's F&I program, the mechanics of how risk gets transferred, priced, and retained have a direct bearing on your profitability. Third-party providers understand this clearly. Many dealers don't — yet.

This article covers what facultative reinsurance is, how it works step by step, how it compares to treaty reinsurance, its core benefits, and what auto dealers should understand about applying reinsurance principles to their own F&I income.

TL;DR

- Facultative reinsurance covers one individual risk at a time, negotiated separately between a ceding insurer and reinsurer

- Both parties retain full discretion to accept or decline each submission — this is the defining characteristic

- It costs more per transaction than treaty reinsurance but offers far greater customization for complex or oversized risks

- A facultative certificate (fac cert) is the legal document formalizing each placement

- Auto dealers can apply the same principle: retain underwriting profits instead of ceding them to third-party providers

What Is Facultative Reinsurance?

The Insurance Information Institute defines facultative reinsurance as a form of reinsurance where "the reinsurer has the power or 'faculty' to accept or reject all or a part of any policy offered to it." That word — "faculty" — is where the term gets its name, and it points directly to what makes this structure distinctive: the reinsurer's right to say yes or no on every single submission.

Unlike treaty arrangements, where a reinsurer commits in advance to accept an entire class of policies, facultative reinsurance operates risk by risk. Every individual submission is a separate negotiation. Nothing is automatic.

The two core parties:

- Ceding company — the primary insurer that transfers a portion of a specific risk to the reinsurer, in exchange for ceding a share of the premium

- Reinsurer — the entity that evaluates, accepts (or declines), and provides coverage for that transferred portion of the risk

IRMI confirms that "the submission, acceptance, and resulting agreement is required on each individual risk or portion of an individual risk that the ceding company seeks to reinsure." Every placement is evaluated and agreed to on its own terms.

How Facultative Reinsurance Works: The Core Mechanics

The Submission and Underwriting Process

When a primary insurer encounters a risk too large or unusual to retain on its own balance sheet, it assembles a detailed submission — covering risk data, projected exposure, policy terms, and any relevant loss history — and presents it to one or more potential reinsurers.

The reinsurer then evaluates the submission against its own risk appetite, underwriting capacity, and area of expertise. This is not a rubber-stamp process. The reinsurer conducts its own independent assessment and retains full discretion to accept, decline, or propose modified terms.

Negotiations are often iterative. Adjustments to coverage limits, pricing, retention levels, and exclusions are common before both parties reach agreement. Once finalized, that agreement gets locked into a formal document.

The Facultative Certificate

Once terms are finalized, the placement is documented in a facultative reinsurance certificate — commonly called a "fac cert." The RAA defines this as "a contract formalizing a reinsurance cession on a specific risk." It specifies:

- The risk details and coverage period

- Premium allocation between ceding company and reinsurer

- Coverage limits and any exclusions

- Each party's obligations in the event of a loss

This certificate is the binding legal instrument for that specific placement. No fac cert, no coverage.

Multiple Reinsurers on a Single Risk

Large risks often require participation from more than one reinsurer. Consider an insurer issuing a $35 million policy on a commercial office building with a retention capacity of $25 million. The remaining $10 million exposure gets placed facultatively across multiple reinsurers, each taking a defined slice until the full amount is covered.

Investopedia notes that an insurer could seek "pieces of the $10 million from 10 different reinsurers" on a single placement. The math has to work in aggregate — every dollar of unretained exposure needs a willing reinsurer before the policy can be issued.

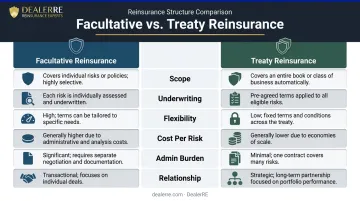

Facultative vs. Treaty Reinsurance: Key Differences

Treaty reinsurance works on a portfolio basis. An insurer and reinsurer negotiate a standing agreement that automatically covers an entire class of policies — say, all commercial auto policies the insurer writes during the treaty period. The reinsurer never reviews individual risks; it relies on a broad assessment of the ceding insurer's underwriting philosophy and historical loss data.

Facultative works the opposite way: each risk is submitted, negotiated, and bound individually on its own certificate.

| Dimension | Facultative | Treaty |

|---|---|---|

| Scope | Individual risks | Entire book or risk class |

| Underwriting | Risk-by-risk assessment | Portfolio-level review |

| Flexibility | Maximum — customized per risk | Standardized within treaty terms |

| Cost per risk | Higher | Lower |

| Admin burden | High per transaction | High upfront, then automated |

| Relationship | Transactional | Long-term partnership |

Investopedia is direct on cost: facultative reinsurance "is generally more expensive than treaty reinsurance" and "requires the use of substantial personnel and technical resources for underwriting activities." That cost is the tradeoff for precision.

The two methods aren't mutually exclusive. A risk subject to a treaty can also carry facultative coverage. When that happens, the facultative layer responds first — it "inures to the benefit of the treaty," meaning the treaty only absorbs what the facultative coverage doesn't.

Key Benefits of Facultative Reinsurance

Tailored Coverage for Complex Risks

Because every placement is negotiated from scratch, facultative reinsurance lets insurers structure each placement around the specific characteristics of a risk — unusual hazards, atypical exposures, or coverage needs that fall outside any treaty's pre-set parameters. Insurance Business Magazine describes it as "generally used to insure large, unusual, or complex risks that are not ordinarily covered by treaty reinsurance."

Expanded Underwriting Capacity

Facultative reinsurance gives primary insurers the ability to write policies that would otherwise exceed their balance sheet capacity. An insurer that can comfortably retain $25 million on a single risk can quote on a $35 million policy by sourcing the excess through facultative placements — without overstretching its capital position.

The III makes this explicit: reinsurance allows an insurer to "underwrite a larger volume of risks without excessively increasing the costs associated with maintaining solvency margins."

Solvency Protection

Transferring a portion of a large risk shields an insurer's equity and regulatory capital reserves from high-severity loss events. Rather than absorbing a catastrophic claim in full, the insurer's net exposure is limited to its retained portion. Key protections this creates include:

- Limits net exposure to the retained portion only

- Preserves liquid assets for ongoing claims obligations

- Protects regulatory capital from single-event volatility

Risk Portfolio Selectivity

Facultative reinsurance gives both parties strategic flexibility. Ceding companies can quote on risks they'd otherwise turn away. Reinsurers, in turn, select placements that fit their own underwriting appetite rather than absorbing whatever a treaty dictates. For specialty and high-value risks, this dynamic is often the only viable path to adequate coverage — treaty markets simply aren't built for outliers.

When Is Facultative Reinsurance Typically Used?

Facultative placements tend to appear in three situations:

- High-value risks where the insured amount exceeds the insurer's individual risk retention limit

- Specialty or unusual risks that fall outside an existing treaty's scope — hazardous operations, unusual structures, niche industries

- Commercial risks outside normal expertise — policies an insurer accepts for business reasons that don't align with their core underwriting competency

Consider a classic scenario: a $35 million commercial building exceeds what the insurer can comfortably hold. The insurer issues the policy, retains its portion, and places the remainder facultatively before coverage attaches.

These three triggers cover most facultative activity. When volume or risk complexity grows, insurers sometimes move toward hybrid structures that blend facultative and treaty characteristics.

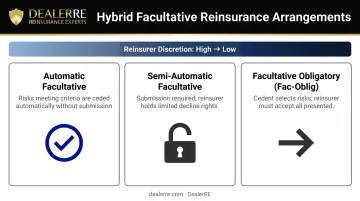

Hybrid Facultative Arrangements

Three hybrid structures are worth knowing:

- Automatic facultative — risks meeting predefined criteria are ceded and accepted automatically, without individual submission or negotiation

- Semi-automatic facultative — a middle-ground approach where the ceding company submits risks but the reinsurer has limited ability to decline within agreed parameters

- Facultative obligatory (fac-oblig) — the ceding company chooses which risks to cede, but the reinsurer must accept every cession that falls within the defined guidelines

Fac-oblig carries the most reinsurer risk of the three: because the reinsurer cannot decline individual submissions, they're effectively accepting whatever the cedent sends their way. That asymmetry is why it's the least common hybrid structure.

What Auto Dealers Should Know About Reinsurance Structures

The core logic of facultative reinsurance — retaining risk selectively and capturing the financial upside of good underwriting — translates directly to automotive F&I.

When dealers sell F&I products through third-party providers, those providers collect the premiums, pay the claims, and keep the underwriting profit — the difference between premiums collected and claims paid. Dealers receive their front-end gross. The long-term financial upside goes elsewhere.

Dealer-owned reinsurance programs change that equation. When a dealer establishes their own admin obligor reinsurance company, premiums flow into the dealer's company. The dealer's pool pays claims. Underwriting profits — which can be substantial over time — stay with the dealer. As DealerRE puts it: if your third-party warranty provider weren't making a profit off your customers, why would they keep doing business with you?

What Flows Through a Dealer-Owned Reinsurance Company

Through DealerRE's admin obligor structure, dealers can reinsure a full range of F&I products:

- Vehicle Service Contracts (VSCs)

- Guaranteed Asset Protection (GAP)

- Collateral Protection Insurance (CPI) and Debt Cancellation Coverage (DCC)

- Ancillary products — tire and wheel, door ding, windshield repair, theft protection

All funds are held in a U.S.-based trust account — no offshore asset transfer. The dealer's reinsurance company is backed by A-rated insurers, meaning if the reinsurance company can't meet obligations, the direct writing insurance company carries ultimate liability.

The BHPH Difference

For Buy Here Pay Here dealers, the structure addresses a specific operational problem: customers who don't pay for vehicles that don't run. A reinsured VSC program lets BHPH dealers build a customer-funded repair pool, protect their lending portfolio, and keep customers current on payments — without coming out of pocket for mechanical repairs.

DealerRE also enables BHPH dealers to formalize GAP coverage rather than absorbing that cost informally when total-loss events occur. The math is straightforward:

- $499 per GAP contract × 150 annual contracts = $75,000 in new receivables

- Coverage dealers were already providing — now sold as a product

Since 1994, DealerRE has helped more than 400 auto dealers nationwide build and manage their own admin obligor reinsurance companies — putting underwriting profits back where they belong. As dealer Tracy Myers put it: "Without question, starting our own reinsurance company is one of the best decisions I ever made in the used car business."

Dealers selling more than 30 cars per month are typically strong candidates to get started.

Frequently Asked Questions

What does facultative reinsurance mean in insurance?

Facultative reinsurance is a form of reinsurance where each individual risk is separately submitted, assessed, and negotiated between the ceding insurer and reinsurer. Both parties retain the right to accept, decline, or counter-propose on any submission before coverage attaches.

What is the primary difference between facultative and treaty reinsurance?

Facultative reinsurance covers one specific risk at a time through individual negotiation. Treaty reinsurance is a standing agreement that automatically covers an entire class or portfolio of risks without risk-by-risk review.

What is a key characteristic of facultative reinsurance?

The defining characteristic is mutual discretion. The ceding company chooses which risks to submit for reinsurance, and the reinsurer chooses whether to accept, decline, or counter-propose on each submission. Neither party is obligated before an individual agreement is reached.

What is an example of facultative reinsurance?

A primary insurer issues a $35 million commercial property policy but can only retain $25 million comfortably. It sources the remaining $10 million through a separately negotiated facultative agreement — potentially across multiple reinsurers — before the policy is issued and coverage attaches.

What is a facultative obligatory arrangement?

Facultative obligatory is a hybrid structure where the ceding insurer selectively chooses which risks to cede, but the reinsurer is obligated to accept all cessions within defined guidelines. Because the reinsurer cannot decline individual submissions, it carries more risk — and these arrangements are less common.

What are the main types of reinsurance?

The primary types are facultative, treaty (quota share, surplus share, and excess of loss), catastrophe reinsurance, and stop-loss. Facultative and treaty describe how risks are placed; proportional and non-proportional describe how losses are shared. Most insurers use a combination depending on their portfolio and risk management goals.