Reinsurance isn't a single arrangement. It spans a spectrum from fully negotiated, risk-by-risk placements to automatic, portfolio-wide cessions — and fac-oblig sits in a strategically important middle position that deserves a clear explanation.

This article defines each type, explains how fac-oblig works in practice, and outlines how to evaluate which structure fits specific business needs — including dealer-owned reinsurance programs for F&I products like VSCs, GAP, and ancillary coverage.

TL;DR

- Facultative reinsurance: Both parties negotiate each risk individually — no standing commitment on either side.

- Obligatory (treaty) reinsurance: Cedant and reinsurer automatically cede and accept all risks within a defined class.

- Fac-oblig: The cedant selects which risks to cede; the reinsurer must accept all of them, creating adverse selection risk.

- Treaty structures dominate dealer F&I programs due to high volume and homogeneous risk profiles.

- Structure selection should follow purpose: wrong choices cost dealers profits, control, or both.

What Is Facultative Obligatory Reinsurance?

Facultative obligatory (fac-oblig) reinsurance is a hybrid arrangement that combines elements of both pure facultative and treaty reinsurance. The ceding insurer retains discretion over which individual risks to cede — the facultative element. The reinsurer, however, is contractually bound to accept any risk submitted that falls within the pre-agreed terms and scope — the obligatory element.

Insurance Business Magazine puts it plainly: "In facultative obligatory reinsurance, the ceding insurer can choose which individual risks to cede, but once selected, the reinsurer must accept them."

The name explains the structure directly:

| Party | Role | Obligation |

|---|---|---|

| Cedant (ceding insurer) | Chooses whether to cede each risk | Optional — no requirement to submit |

| Reinsurer | Must accept any risk submitted within agreed scope | Mandatory — no right to decline |

Neither pure facultative nor standard treaty reinsurance shares this one-sided arrangement.

The "Open Cover" Synonym

Fac-oblig is also known as a fac-oblig facility or open cover arrangement. Arundo Re, a European reinsurer, explains the terminology directly: "A Facob, also called open-cover, is a specific type of reinsurance treaty." The "open cover" label reflects that the agreement creates a standing framework — the cover remains open for the cedant to activate at its discretion without renegotiating each risk.

Fac-oblig is a specialized arrangement, used primarily in property, marine, and specialty lines where insurers need guaranteed placement capacity for irregular, non-standard risks. Its appeal lies in that guaranteed access — cedants can place difficult or oversized risks without negotiating a new agreement each time.

Types of Reinsurance: Facultative, Obligatory, and Fac-Oblig Defined

Reinsurance is not one-size-fits-all. The three primary approaches each serve different functions and carry distinct obligations for both parties.

Facultative Reinsurance

Facultative reinsurance is a risk-by-risk arrangement where both parties independently negotiate each placement. Neither is obligated to offer or accept — every deal is discretionary.

IRMI defines it as an arrangement where "the submission, acceptance, and resulting agreement is required on each individual risk" and "the reinsurer is not obliged to accept every or any submission."

Best suited for:

- Large or unusual single risks exceeding treaty capacity

- Risks explicitly excluded from treaty scope

- Specialty exposures requiring individual underwriting assessment

- One-off placements where standard treaty terms don't apply

Key trade-off: Maximum flexibility and tailored terms for complex risks, but no guaranteed capacity and significant administrative overhead. Every placement starts from zero.

Facultative reinsurance accounts for roughly 10–20% of global reinsurance premium volume — the remainder belongs to treaty structures.

Obligatory (Treaty) Reinsurance

Treaty reinsurance is a standing agreement with dual automaticity: the ceding insurer must cede all qualifying risks, and the reinsurer must accept them — no individual negotiation, no right to decline.

Investopedia defines it as a treaty that "requires an insurer to automatically send all policies on its books that fall within a set list of criteria to a reinsurer," with the reinsurer "obliged to accept these policies."

Common treaty structures include:

| Structure | Type | Typical Use |

|---|---|---|

| Quota Share | Proportional | High-volume F&I portfolios (VSC, GAP) |

| Surplus | Proportional | Commercial property and liability |

| Excess of Loss (XoL) | Non-proportional | Catastrophe and large individual losses |

| Stop Loss | Non-proportional | Protecting aggregate portfolio profitability |

Treaty reinsurance represents 80–90% of global reinsurance premium volume, making it the default structure for most commercial programs.

Best suited for: High-volume, homogeneous, predictable portfolios — exactly the profile of dealer F&I products like VSCs and GAP where hundreds or thousands of similar contracts are written annually.

Facultative Obligatory Reinsurance

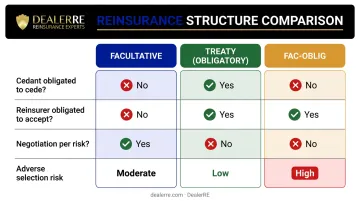

Fac-oblig occupies a structural middle ground: the cedant chooses which risks to cede, but once a risk qualifies under the agreement, the reinsurer has no right to decline. That one-sided optionality defines everything about how this structure behaves.

| Feature | Facultative | Treaty | Fac-Oblig |

|---|---|---|---|

| Cedant obligated to cede? | No | Yes | No |

| Reinsurer obligated to accept? | No | Yes | Yes |

| Negotiation required per risk? | Yes | No | No |

| Adverse selection risk | Moderate | Low | High |

The asymmetry in the fac-oblig column is the defining feature — and the source of its primary risk. Because the cedant selects what to cede but the reinsurer must accept, the reinsurer can end up with a systematically worse-than-average portfolio.

Best suited for: Non-standard or emerging risks that fall outside standard treaty capacity, require guaranteed placement without per-risk negotiation, or arise irregularly enough that a full treaty structure isn't warranted.

Why Reinsurance Structure Matters for Auto Dealers

Auto dealers who operate — or are evaluating — dealer-owned reinsurance programs need to understand reinsurance structure for a straightforward reason: the structure determines who retains the underwriting profit.

DealerRE has helped more than 400 auto dealers build reinsurance programs since 1994, administering programs across the full range of F&I products: vehicle service contracts, GAP, collateral protection insurance (CPI), debt cancellation coverage (DCC), tire and wheel protection, door ding, windshield repair, and theft protection. Across every product category, the reinsurance structure controls how profits flow.

If a third-party warranty or insurance provider weren't profiting from a dealer's book of business, they wouldn't keep doing it. Dealer-owned reinsurance structures let dealers capture those underwriting profits instead — but only when the structure fits the dealer's risk profile, volume, and product mix.

Mismatched structures have measurable consequences:

- Ceding profits unnecessarily to third parties through poorly designed arrangements

- Losing underwriting control over claims decisions

- Facing claims liabilities that exceed the program's capacity

- Creating regulatory exposure through structures that lack genuine risk transfer characteristics

For BHPH dealers, the structural stakes are higher still. Mechanical breakdown products for in-house financed vehicles involve different payment timing than retail programs — premiums billed monthly as customers make payments rather than collected upfront. The structure must accommodate that cash flow pattern while still delivering full profit capture.

That's where the distinction between facultative and obligatory arrangements becomes directly relevant to program design.

How to Choose the Right Reinsurance Structure

Structure selection should follow purpose. The right type depends on the nature of the risks, portfolio volume, required flexibility, and long-term program objectives.

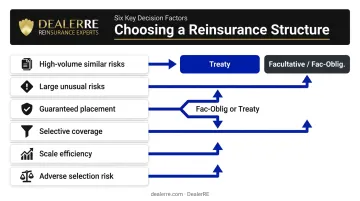

Key Decision Factors

- High-volume, similar risks (hundreds of VSC or GAP contracts annually) → treaty

- Large, unusual, or one-off risks → facultative or fac-oblig

- Guaranteed placement without per-risk negotiation → fac-oblig or treaty

- Selective, case-by-case coverage → pure facultative

- Scale efficiency: treaty handles entire portfolios automatically; fac-oblig requires per-risk documentation; pure facultative requires full negotiation per placement

- Adverse selection risk: fac-oblig demands strong internal underwriting standards — without them, the reinsurer absorbs a disproportionately poor book; treaty eliminates this through automatic, non-selective cession

For Dealer F&I Programs

The U.S. vehicle service contract market totals $33 billion at retail annually with roughly 16 million contracts sold per year. That volume and homogeneity points directly to treaty (quota share) reinsurance:

- Automatic cession of all qualifying F&I contracts

- No individual risk selection required

- Lowest administrative burden at scale

Because dealer F&I programs involve high volumes of homogeneous contracts, fac-oblig adds adverse selection risk and per-risk documentation with no corresponding benefit. When the goal is to reinsure an entire book, that complexity works against the program.

DealerRE's approach starts with a dealership analysis — evaluating cars sold per month, product mix, and program goals — before recommending any structure. That analysis surfaces whether a dealer's volume, product mix, and claims exposure actually support the structure being proposed — before any program is built.

Mistakes to Avoid When Evaluating Reinsurance Options

Two structural mistakes show up consistently and carry significant consequences.

Choosing structure based on familiarity rather than fit

The most available arrangement isn't always the most appropriate one. Dealers who select a structure because it's what their agent knows or what peers use — rather than what matches their risk profile and volume — often end up ceding profits unnecessarily or locked into terms that limit program flexibility as their business grows.

As the dealer's volume or product mix evolves, the original structure may become suboptimal. Annual reviews with a qualified reinsurance advisor are how dealers catch this before it costs them.

Underestimating adverse selection risk in fac-oblig arrangements

If a dealer or insurer attempts to use a fac-oblig structure to selectively cede only high-mileage or older-vehicle VSC contracts while retaining lower-risk inventory, the reinsurer ends up with a loss ratio far above what the agreement's pricing anticipated.

Protecting against this requires:

- Clear eligibility criteria defining exactly what can and cannot be ceded

- Retention requirements so the cedant keeps real exposure on ceded contracts

- Transparent underwriting standards embedded in the agreement

- Regular loss experience monitoring to catch adverse trends early

Ignoring these safeguards creates financial imbalance, invites disputes, and can trigger early termination or jurisdictional conflicts that turn coverage disagreements into litigation. Dealers entering fac-oblig arrangements should treat the agreement language as a working document, not a formality — because when loss ratios drift, the quality of that language determines what happens next.

Conclusion

Facultative, obligatory, and facultative obligatory reinsurance represent three distinct approaches to risk transfer, each with different obligations, flexibility levels, and appropriate use cases. The differences matter because they determine who bears underwriting exposure, how profits are retained, and how claims are managed.

For auto dealers building F&I reinsurance programs, treaty-based quota share structures remain the structurally sound, administratively efficient choice for high-volume products like VSCs and GAP. Fac-oblig has legitimate applications in specialty commercial reinsurance — but it introduces adverse selection risk and complexity that don't fit the standardized, predictable nature of dealer F&I portfolios.

DealerRE has been helping dealers navigate these decisions since 1994. If this article raised questions about how your current program is structured — or whether the structure fits your actual volume and product mix — that's worth a conversation before the next renewal cycle.

Frequently Asked Questions

What is FAC oblig reinsurance?

FAC oblig (facultative obligatory) reinsurance is a hybrid arrangement where the ceding insurer has discretion to choose which individual risks to cede, while the reinsurer is contractually obligated to accept any risk that qualifies under the pre-agreed terms.

What is the difference between facultative reinsurance and obligatory reinsurance?

Facultative reinsurance involves individual, negotiated risk placements — neither party is obligated to offer or accept any specific risk. Obligatory (treaty) reinsurance requires both parties to automatically cede and accept all risks within a defined class, with no case-by-case discretion on either side.

What is the main risk of facultative obligatory reinsurance for the reinsurer?

The primary risk is adverse selection. Since the cedant controls which risks to submit but the reinsurer must accept them, the cedant may selectively cede only the most challenging or loss-prone risks — leaving the reinsurer with a disproportionately poor portfolio that performs worse than the agreement's pricing assumed.

When is facultative obligatory reinsurance typically used?

Fac-oblig is used for large, non-standard, or emerging risks that exceed standard treaty limits or fall outside treaty scope, where the cedant needs guaranteed placement capacity without negotiating each risk individually. It's most common in property, marine, and specialty commercial lines.

How does reinsurance structure affect a dealer-owned reinsurance program?

Reinsurance structure governs how risk is transferred, how underwriting profits are retained, and how claims exposure is managed. Treaty (quota share) structures are standard for dealer F&I programs because they efficiently handle high-volume, homogeneous products like VSCs and GAP while aligning with the dealer's volume, product mix, and profitability objectives.

Can a dealer-owned reinsurance program use a fac-oblig structure?

Treaty reinsurance is the standard for dealer-owned programs given the high-volume, homogeneous nature of F&I products. Fac-oblig could apply to non-standard exposures outside a treaty's scope, but it introduces adverse selection risk and administrative complexity that rarely serve dealer programs well.