Introduction

Every F&I deal a dealer closes generates underwriting profit. The question is who keeps it.

For most dealerships, the answer is a third-party provider. Dealers earn the markup, close the deal, and move on — while the warranty company retains the reserve sitting between premiums collected and claims paid. At scale, across hundreds of contracts per year, that's a substantial revenue stream the dealer never sees.

Meanwhile, front-end vehicle margins continue to compress. F&I departments now account for roughly 25% of total dealership gross profit, up from 15% in 2009 — meaning F&I income has never mattered more to overall dealer profitability. Yet most dealers are structured to share that value rather than own it.

Automotive reinsurance changes that equation. This article breaks down what dealer-owned reinsurance actually is, the three primary financial and operational advantages it creates, and how dealerships of different types and sizes can put it to work.

TL;DR

- Dealer-owned reinsurance captures the underwriting profit that third-party F&I providers currently keep

- Dealers gain direct control over claims adjudication, which directly shapes customer experience outcomes

- Properly structured programs offer tax deferral under IRC Section 831(b) and long-term wealth-building through invested reserves

- Franchise dealers, independent dealers, and BHPH operations each benefit — with the right program structure in place

- The financial advantages compound: every year without a program is a year of lost underwriting profit you can't recover

What Is Automotive Reinsurance?

Dealer-owned reinsurance is exactly what it sounds like: the dealer owns an insurance company that participates in the underwriting profit of the F&I products sold at their dealership.

Here's the plain-language version. When a dealer sells a vehicle service contract through a third-party provider, two profit events happen:

- The dealer earns a gross profit on the sale

- The third-party provider retains the underwriting profit — the premium reserve left after claims are paid

Reinsurance addresses the second event. By owning a reinsurance entity that assumes a portion of the risk on those same contracts, the dealer redirects that reserve back to themselves. As DealerRE puts it to new clients: "If your warranty company were not making a profit off of you selling their products, would they continue to do business with you?"

What Products Qualify?

Most F&I products a dealer already sells can be structured into a reinsurance program:

- Vehicle service contracts (VSC) / extended warranties

- Guaranteed Asset Protection (GAP)

- Collateral Protection Insurance (CPI)

- Debt Cancellation Coverage (DCC) — particularly relevant for BHPH

- Ancillary products: tire and wheel, door ding, windshield repair, theft protection

The dealer doesn't change what they sell. They change where the underwriting profit goes — from a third party's balance sheet to their own.

The distinction matters: authorized resellers earn a commission on each sale. Dealers who own a reinsurance company capture the reserve — the profit that keeps accumulating as long as claims stay below the premium collected.

Key Advantages of Automotive Reinsurance for Dealers

The advantages below are tied to measurable financial and operational outcomes. Over 400 dealerships have built these benefits into their business through dealer-owned reinsurance programs — including several NIADA National Quality Dealer of the Year recipients.

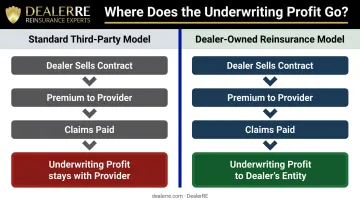

Advantage 1: Profit Retention — Capturing What Third Parties Keep

Under a standard third-party F&I arrangement, the provider keeps the underwriting profit. The dealer earns the markup on the sale, but the reserve — the premium that isn't used to pay claims — stays with the vendor.

F&I PVR for publicly traded dealer groups reached $2,515 in Q2 2025, up from $1,463 in 2019 — a 72% increase in six years. That growth represents an expanding profit pool, and dealers without reinsurance structures are ceding a growing share of it to third parties.

Under a dealer-owned reinsurance model, premiums flow into the dealer's reinsurance entity. Claims are paid from that reserve. Whatever remains belongs to the dealer.

KPIs directly affected:

- F&I profit per vehicle retailed (PVR)

- Total annual F&I revenue

- Net dealer profit margin

When it matters most: Higher-volume dealers with consistent product penetration see the most immediate return. Lower-volume operations still recover meaningful underwriting profit over a 3–5 year window as reserves accumulate. The vehicle service contract industry reached $35 billion at retail with industry VSC attachment rates averaging around 46% — meaning the premium pool flowing through dealer F&I programs is substantial.

Advantage 2: Claims Control and Customer Experience

When a dealer owns the reinsurance entity behind their F&I products, they gain direct influence over how claims are adjudicated, rather than depending on a third-party administrator whose incentives favor minimizing payouts over satisfying customers.

This matters more than most dealers initially recognize. Consider the service retention data:

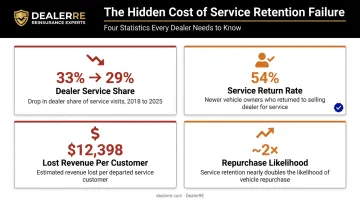

- Dealership share of total service visits fell from 33% in 2018 to 29% in 2025, a 12% decline

- Only 54% of owners with vehicles two years old or newer returned to the selling dealership for service in 2025

- Each lost service customer represents approximately $12,398 in lost revenue over the vehicle's ownership period

- Service retention can nearly double a customer's likelihood to repurchase from the same dealer

A claims experience is a service experience. When a third party handles it poorly, the dealer absorbs the reputational damage without any say in the outcome. Dealer-controlled claims processes allow for fair, fast resolution, turning a breakdown into a loyalty moment instead of a complaint.

For DealerRE clients, claims adjudication is handled through Assured Vehicle Protection (AVP), with the dealer maintaining meaningful influence over how their customers are treated. DealerRE's full-service model gives dealers the operational infrastructure to deliver on that promise without managing the complexity independently.

KPIs directly affected:

- Customer satisfaction scores (CSI)

- Service lane retention rate

- Repeat purchase rate

BHPH-specific note: For buy-here-pay-here dealers, claims control is even more critical. Customers won't pay for vehicles that don't run. A dealer-controlled reinsurance program funds repairs quickly, keeps customers current on payments, and reduces repossession rates — making it as much a portfolio management tool as a customer experience one.

Advantage 3: Tax Advantages and Long-Term Wealth Building

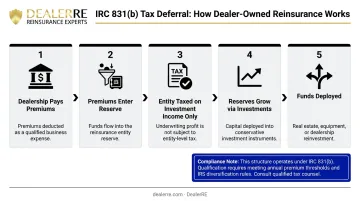

A properly structured dealer-owned reinsurance company can offer significant tax deferral opportunities that traditional F&I arrangements cannot.

Under IRC Section 831(b), qualifying small insurance companies — including dealer-owned reinsurance entities with net written premiums below $2.2 million annually — may elect to be taxed only on investment income, not on underwriting profits. The dealership deducts those premiums as ordinary business expenses.

The practical result: instead of recognizing underwriting income at the dealership level immediately, those funds accumulate in the reinsurance entity's reserve. They grow through conservative investment in government securities and become available for deployment into real estate, dealership reinvestment, equipment, or education funding.

Important compliance context: The IRS has increased scrutiny of micro-captive structures through Notice 2016-66 and subsequent regulations. DealerRE's approach specifically addresses this — the company emphasizes full compliance with IRS Code 831(b), works with specialized insurance CPAs, and structures programs to ensure legitimate risk transfer. Dealers should always work with qualified tax advisors on the specifics of their situation.

KPIs directly affected:

- Effective tax rate

- Net retained earnings

- Return on invested reserves

- Total asset base outside dealership operations

Who benefits most: Dealers who are profitable and growing feel the most immediate tax pressure, making deferral and reserve accumulation especially valuable. DealerRE structures funds held in a U.S.-based trust account (no money is sent offshore), providing both security and regulatory clarity.

What Happens When Dealers Skip Reinsurance

Dealers who rely entirely on third-party F&I providers are directly funding someone else's underwriting profit — month after month, deal after deal.

The math is structural. Third-party warranty and insurance companies are consistently profitable on dealer-sourced business. They price their products to retain underwriting margin after claims. That margin exists whether a dealer participates in it or not; the question is who it flows to.

The hidden costs of non-participation:

- Underwriting profit goes elsewhere — every contract written generates reserves the dealer never touches

- Claims control surrendered — the customer's warranty experience is managed entirely by a third party

- Tax-deferred growth forfeited — reserves that could have grown inside a dealer-owned structure instead show up as ordinary taxable income

- The gap widens over time — each year without a program adds to the cumulative underwriting profit already ceded, and there's no way to recover it retroactively

To put a number on it: there are approximately 16,500 franchise dealerships in the U.S., with average F&I PVR exceeding $2,500 and F&I accounting for roughly 25% of total gross profit. The aggregate underwriting pool flowing to third-party providers is enormous in aggregate. Dealers without a reinsurance program are ceding a portion of that pool every single month.

How to Get the Most Value from Your Reinsurance Program

The structure only works if the dealership uses it well. Three operational factors separate high-performing reinsurance programs from ones that underperform their potential.

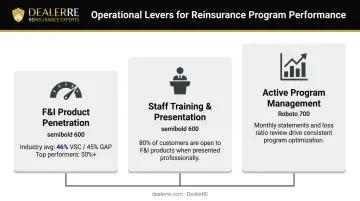

The admin obligor structure — where the dealer's reinsurance company is backed by an A-rated insurer — is the most practical starting point for most dealerships. It provides profit participation while limiting the dealer's direct liability to their formation costs plus accumulated earnings. The fronting carrier covers ultimate claim obligations if reserves fall short.

Three operational levers that separate high-performing programs from underutilized ones:

F&I product penetration — Industry averages sit at roughly 46% for VSCs and 45% for GAP. Top performers push past 50%. Higher penetration means more premium flowing into the reinsurance reserve, which directly increases underwriting profit capture.

Staff training and consistent presentation — NIADA research indicates that 80% of customers are at least willing to listen on F&I products. Effective presentation converts that openness into penetration. DealerRE's model includes F&I training classes (online and in-person), F&I menus, and ongoing development as part of full-service administration — not as an add-on.

Active program management — Reviewing loss ratios, adjusting product offerings, and reinvesting reserves strategically are what keep a program growing. DealerRE provides monthly financial statements, performance analysis, and compliance management so dealers aren't navigating program health blind.

All three levers are supported under DealerRE's full-service administration model, which handles claims adjudication, compliance, legal filings, tax return preparation, and performance reporting in one relationship. Dealers stay focused on the floor. The program compounds in the background.

Conclusion

Automotive reinsurance isn't a complex instrument reserved for large franchise groups. It's a structured way for any dealership to recover profits they are already generating — but currently routing to someone else.

The three advantages covered here — profit retention, claims control, and tax-advantaged wealth building — reinforce each other. Better claims control improves customer retention, which increases product renewal rates, which grows the premium pool, which amplifies the tax deferral advantage over time.

That cycle only works in a dealer's favor if the program is running. The earlier it starts, the longer it has to build — and dealers who understand that are already ahead of those still paying third-party providers to hold profits they've earned. If you're ready to see what a dealer-owned reinsurance program could look like for your store, DealerRE has been structuring these programs since 1994.

Frequently Asked Questions

What is automotive reinsurance?

Automotive reinsurance is a program structure in which a dealer owns a reinsurance company that participates in the underwriting profit of F&I products sold at their dealership. Rather than that profit going entirely to a third-party provider, it flows into the dealer's own entity — minus claims paid and expenses.

What is F&I reinsurance?

F&I reinsurance refers to reinsurance programs tied to finance and insurance products sold in the dealership's business office — vehicle service contracts, GAP coverage, CPI, DCC, and ancillary products. The dealer's reinsurance entity assumes a share of the premium and retains the underwriting profit after claims.

What types of dealers can benefit from a reinsurance program?

Franchise dealers, independent dealers, retail used car dealers, and BHPH dealerships can all benefit. Program structure varies based on volume, product mix, and business model — BHPH programs, for example, use monthly premium billing aligned with customer payment schedules to protect cash flow.

What is an admin obligor reinsurance structure?

An admin obligor structure positions the dealer's reinsurance company as the obligor on service contracts, backed by an A-rated insurance carrier. The dealer captures underwriting profits while the fronting carrier assumes ultimate claim liability if reserves fall short, limiting the dealer's direct financial exposure.

How do dealers get started with their own reinsurance company?

Setup typically involves working with a reinsurance administrator like DealerRE to establish the legal entity, select the appropriate program structure, and integrate it with existing F&I product offerings. DealerRE handles licensing, tax preparation, compliance, and onboarding as part of its full-service model.

Can a dealer-owned reinsurance company be used for tax planning?

Yes. Properly structured programs may qualify under IRC Section 831(b), allowing the entity to be taxed only on investment income — not underwriting profits — with accumulated reserves available to invest in real estate, equipment, or other assets. Dealers should consult a qualified tax advisor for guidance specific to their situation.