Introduction

Reinsurance structure is one of those topics that looks simple on the surface — until a large claim hits and you realize your program wasn't set up to handle it the way you expected.

That gap usually traces back to one decision: per risk vs. per occurrence. Both are forms of excess-of-loss reinsurance, but they respond to completely different scenarios. Choose the wrong structure and you may be paying for protection that never activates — or absorbing losses you assumed were covered.

For auto dealers operating — or considering — their own reinsurance companies, this distinction is practical. The F&I products your program covers, your portfolio size, and the nature of your typical claims all determine which structure fits.

Motor vehicle repair costs have risen 43.6% since January 2019, which means high-severity individual claims are more common than they used to be. Getting the structure right matters more now.

This article breaks down how each structure works, where each one belongs in a dealer reinsurance program, and what to watch for when your program covers more than one line of business.

TL;DR

- Per risk triggers when a loss on one individual contract exceeds the dealer's retention.

- Per occurrence triggers when a single event (hailstorm, batch defect) causes losses across multiple policies exceeding the dealer's retention.

- The unit being measured is the key difference: one contract vs. one event affecting many contracts.

- Most dealer VSC programs use per risk structures because mechanical claims are individual, not event-driven.

- The wrong structure leaves either coverage gaps or premiums spent on protection that never triggers.

What Are Per Risk and Per Occurrence Reinsurance?

Both structures fall under non-proportional (excess-of-loss) reinsurance. Unlike proportional structures, there's no dollar-for-dollar sharing of every loss. The reinsurer sits above the retention and only steps in after the dealer's company has absorbed its defined share.

Per Risk Reinsurance

Per risk excess reinsurance, as defined by IRMI, allows an insurer to recover losses on an individual risk above a specified per-risk retention. Each covered risk is evaluated on its own, in isolation from every other claim.

In a dealer program, a "risk" is typically one vehicle or one service contract. One customer's VSC on one car. That claim stands alone. If it exceeds the retention, the reinsurer covers the excess. If it doesn't, the dealer's company absorbs it entirely, with no reinsurer involvement.

Per Occurrence Reinsurance

Per occurrence reinsurance shifts the trigger from a single claim to a group of claims tied to one event. The Puerto Rico Office of the Commissioner of Insurance reinsurance glossary defines this as indemnifying losses above a specified retention with respect to an accumulation of losses resulting from a catastrophic event or series of events.

Multiple claims from one occurrence get pooled. Once that pool exceeds the retention, the reinsurer pays the excess up to the per-occurrence limit.

What This Means for Dealer Programs

The product type determines which trigger applies:

- VSC / mechanical breakdown — claims are individual and unrelated; per risk is typically appropriate

- Physical damage / CPI programs — a single weather event can hit multiple vehicles simultaneously; per occurrence protection becomes relevant

- GAP / ancillary F&I — generally individual in nature, aligning more with per risk

How Per Risk Reinsurance Works

The Basic Mechanics

The dealer's reinsurance company retains losses on each individual claim up to the retention limit. When a single claim exceeds that retention, the reinsurer covers the difference — up to the stated reinsurance limit. Each new claim on a different vehicle starts fresh.

Example: Retention is set at $2,500 per risk. A VSC claim on one vehicle comes in at $7,000 — a transmission replacement plus labor. The dealer's company pays the first $2,500. The reinsurer covers the remaining $4,500. A separate engine claim on a different vehicle next week? That starts a brand new $2,500 retention calculation.

Why the Reinsurance Limit Matters

The per-risk reinsurance limit caps what the reinsurer will pay on any single claim. This matters because high-severity repairs have become genuinely expensive. AAA reports mechanic labor rates commonly running $120–$159 per hour in 2026. Engine replacements, transmission failures, and major powertrain work can push claims well past what most dealers expect.

Without a well-calibrated per-risk limit, a dealer's program either overpays for reinsurance capacity it doesn't need or finds itself uncovered on truly catastrophic single-vehicle claims.

How a Per Risk Claim Is Processed

Understanding where the limit sits helps frame how a claim actually moves through the system:

- Claim submitted on a covered vehicle

- Loss assessed against the per-risk retention for that individual contract

- If the claim exceeds retention, the excess is presented to the reinsurer for recovery

- Reinsurer pays the excess up to the stated per-risk limit

- Next claim on a different vehicle starts the process over from zero

The per-risk structure gives the dealer's reinsurance company predictable loss containment on high-severity individual claims, while preserving full underwriting income on the smaller claims that stay within retention.

How Per Occurrence Reinsurance Works

The Basic Mechanics

Instead of evaluating claims one by one, per occurrence reinsurance aggregates all losses from a single defined event. Once the combined losses from that event exceed the retention, the reinsurer pays the excess up to the per-occurrence limit.

The definition of "occurrence" in the treaty determines what qualifies. The Casualty Actuarial Society notes that catastrophe excess-of-loss treaties typically include hours clauses — commonly 72 hours — to define the time window within which losses from a single event are aggregated. Without precise contract language, insurers and reinsurers may dispute what qualifies as a single occurrence.

When This Structure Is Relevant for Dealers

Per occurrence protection becomes meaningful when a single event can generate multiple simultaneous claims. The most common scenario in the dealer context is physical damage from severe weather.

In 2025, the U.S. experienced 52 severe convective storm events with $52.3 billion in insured losses. Dealer lots are exposed to this risk in a concentrated way — all inventory sitting in one location, subject to the same storm. A hailstorm that damages 15 vehicles across a BHPH dealer's lot isn't 15 separate per-risk events. It's one occurrence producing 15 claims.

Example: A hailstorm damages 15 vehicles on a dealer's lot. Combined physical damage claims total $90,000. With a per occurrence retention of $25,000 and a reinsurance limit of $200,000, the dealer's company retains $25,000 and recovers $65,000 from the reinsurer. That's a single retention absorbing a multi-vehicle event — very different from 15 individual retentions under a per-risk structure.

Where Per Occurrence Fits in Dealer Programs

That hailstorm scenario points to a broader pattern. Per occurrence is more relevant when:

- The program covers physical damage or CPI across a portfolio of vehicles

- Vehicles are geographically concentrated — same lot, same ZIP code, same weather exposure

- The dealer operates a BHPH portfolio with collateral protection on multiple financed units

- A single event (weather, fleet accident, regional issue) could realistically trigger multiple claims at once

Key Differences and How to Choose the Right Structure

The practical distinction is simpler than the technical definitions suggest. Per risk asks: how much did this single claim cost? Per occurrence asks: how much did this one event cost across all affected policies?

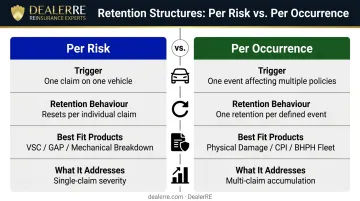

Comparison at a Glance

| Factor | Per Risk | Per Occurrence |

|---|---|---|

| Trigger | One claim on one vehicle/contract | One event affecting multiple policies |

| Retention reset | Fresh for each new risk | One retention per defined event |

| Best fit | VSC, GAP, mechanical breakdown | Physical damage, CPI, BHPH fleet coverage |

| Key risk addressed | Single-claim severity | Multi-claim accumulation from one event |

Factors to Evaluate When Choosing

- Product type — VSC and GAP claims are almost always individual; physical damage claims can cluster

- Portfolio concentration — the more vehicles covered in one location, the more relevant per occurrence protection becomes

- Typical claim severity — high-severity individual claims favor per risk; event-driven accumulation favors per occurrence

- Program mix — a dealer running both VSC and CPI may need both structures

Some dealer-owned programs use both structures in combination: per risk excess-of-loss on VSC claims layered with per occurrence catastrophe protection on physical damage. Each layer targets a different type of loss exposure. DealerRE works with dealers to analyze their actual program profile and match retention levels to real risk — not just build coverage that looks thorough on paper.

Common Misconceptions About These Reinsurance Structures

These three misconceptions show up regularly in dealer conversations about reinsurance structure — and each one can lead to real misalignment between program design and actual protection.

"Per Occurrence Means Per Claim"

This is the most common confusion. Many dealers assume any single repair event — a transmission job, an engine replacement — is automatically an "occurrence" under per occurrence reinsurance. It isn't. A single claim on a single vehicle is a per-risk event. An occurrence requires an incident that simultaneously produces losses across multiple covered risks. That distinction determines whether the reinsurer responds at all.

"Per Occurrence Is Always Broader Protection"

Per occurrence coverage is designed for accumulation risk. If a dealer's program doesn't have meaningful accumulation exposure — most claims are independent mechanical repairs on individual cars — per occurrence protection may trigger rarely or never. Paying for coverage built to respond to hailstorms when your program is purely VSC-based is buying the wrong tool.

"The Retention Works Like an Annual Deductible"

Some dealers interpret per-risk retention as something that fills up over the course of a year and then resets. That's not how it works. In per risk reinsurance, the retention applies fresh to each individual claim on each individual risk. There's no annual aggregate threshold.

Consider what that means in practice:

- A dealer with 200 VSC claims in a year faces 200 separate retention calculations

- Each claim is evaluated independently — no "credit" carries over from prior claims

- Reinsurer recovery depends on individual claim severity, not cumulative volume

Getting this wrong leads to inflated recovery projections and program costs that don't pencil out as expected.

Frequently Asked Questions

What is the difference between per risk and per occurrence reinsurance?

Per risk triggers when a loss on one individual vehicle or contract exceeds the retention — each risk is evaluated independently. Per occurrence triggers when a single event causes aggregate losses across multiple policies that exceed the retention. The distinction comes down to unit of measurement: one contract versus one event affecting many.

What is per risk reinsurance?

Per risk reinsurance is a form of excess-of-loss coverage where the reinsurer pays the portion of a claim on a single identified risk that exceeds the ceding company's retention limit, up to the reinsurance limit. Each new claim on a different risk resets the retention calculation independently.

What does $100,000 per occurrence mean?

A $100,000 per occurrence limit means the reinsurer will pay up to $100,000 for all covered losses arising from a single defined occurrence or event, after the dealer's retention is met. It caps the reinsurer's exposure per event — not per individual claim — so multiple claims from one storm share that single limit.

When would a dealer choose per occurrence over per risk reinsurance?

Per occurrence fits programs with physical damage or fleet exposure where a single weather, collision, or environmental event could simultaneously generate multiple claims. It's most common in BHPH physical damage and collateral protection programs, where that kind of accumulation risk is real.

Can per risk and per occurrence reinsurance be combined in a single dealer program?

Yes. Programs can layer both structures — per risk protection on individual VSC or warranty claims and per occurrence protection on physical damage accumulation. Each layer addresses a different type of loss exposure, and the two don't conflict when structured correctly.

How is the retention limit set in a per risk reinsurance contract?

Retention is set based on program size, claim frequency history, average repair severity, and premium economics. The goal is a level that keeps reinsurance costs manageable while still providing meaningful protection when high-severity claims such as engine replacements or major transmission failures hit the program.