For auto dealers, this distinction is more than academic. Confusing the two leads to misunderstanding where profits go in an F&I program, what financial tools are actually available, and — most importantly — whether you're participating in the profit side of the insurance products you sell every day.

According to the NAIC, reinsurance is "insurance for insurance companies" — a contract between two insurers, completely separate from the end consumer. Excess insurance, by contrast, is purchased by a policyholder to extend coverage beyond a primary policy's limits. Same general space, opposite ends of the insurance relationship.

TL;DR

- Reinsurance transfers risk between insurers — the policyholder is not a party to the contract

- Excess insurance extends coverage for the policyholder once primary policy limits are exhausted

- Reinsurance sits behind the primary insurer; excess insurance sits above the primary policy

- Dealers who own their reinsurance company keep the underwriting profits that would otherwise go to third-party F&I providers

- These two tools are not interchangeable and carry distinct legal, financial, and tax implications

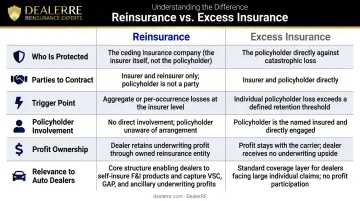

Reinsurance vs. Excess Insurance: Quick Comparison

Here's how reinsurance and excess insurance compare across the dimensions most relevant to auto dealers:

| Dimension | Reinsurance | Excess Insurance |

|---|---|---|

| Who is protected | The primary insurer (cedent) | The policyholder |

| Parties to the contract | Insurer-to-reinsurer | Policyholder-to-insurer |

| Trigger point | Reinsurer's agreed retention level | Exhaustion of primary policy limits |

| Policyholder involvement | None (except assumption reinsurance) | Direct contractual relationship |

| Profit ownership | Retained by the reinsurer (or dealer-owned entity) | No profit-sharing mechanism |

| Relevance to auto dealers | Core profit strategy for F&I programs | Liability protection only |

Reinsurance operates between insurers — excess insurance is a product a policyholder buys. For dealers, only one of these structures creates a profit opportunity.

What Is Reinsurance?

Reinsurance is a contract where a primary insurer — the cedent — transfers a portion of its risk to another insurer (the reinsurer) in exchange for a share of premiums. The end policyholder has no direct relationship with the reinsurer and typically has no knowledge the arrangement exists.

Swiss Re describes two main types:

- Proportional (quota share): Premiums and losses are shared between the cedent and reinsurer at a fixed percentage from the first dollar of loss

- Non-proportional (excess of loss): The reinsurer only pays once losses exceed a specified retention point — the cedent absorbs everything below that threshold

In the auto dealer F&I context, proportional quota share structures are generally more common because they allow the dealer-owned reinsurance company to participate in premiums from day one, rather than waiting for losses to exceed a high threshold.

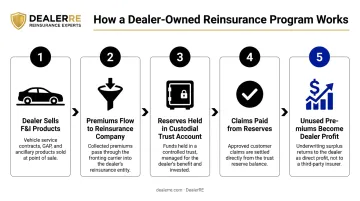

How Dealer-Owned Reinsurance Works

A dealer establishes their own reinsurance company — typically structured as an admin obligor backed by A-rated insurers — to reinsure the F&I products their dealership sells. The mechanics:

- The dealer sells F&I products (VSCs, GAP, ancillary coverage) to customers

- Premiums flow into the dealer's reinsurance company via a fronting carrier

- The reinsurance company holds reserves in a custodial trust account

- Claims are paid from those reserves; unused premiums become underwriting profit

- The dealer's company retains that profit — not a third-party provider

The A-rated insurer backing matters for one key reason: if the dealer's captive reinsurance company cannot meet its obligations, the direct writing insurance company remains ultimately liable. The dealer's financial exposure is limited to formation costs and accumulated earnings.

DealerRE has helped over 400 dealers build and manage programs structured exactly this way since 1994.

Use Cases of Reinsurance in Auto Dealerships

F&I gross profit per vehicle retailed averaged $2,505 in Q1 2025, according to Haig Partners — and that number continues climbing. Every dollar of that profit runs through products that generate underwriting income on the back end.

Dealers who rely on third-party providers for VSCs, GAP, tire and wheel, windshield repair, and other ancillary products are keeping their front-end commission while the provider retains the underwriting profit on unexpired reserves. Reinsurance puts that underwriting profit back in the dealer's pocket.

Profit retention is only part of the picture. Dealer-owned reinsurance also provides:

- Claims control — drive service contract claims back to your own service department, and stop waiting on third-party approval processes

- Reserve investment — funds held in trust can be invested; once reserves exceed 125% of unearned premiums, excess capital can be deployed more aggressively

- Wealth-building flexibility — dealers have used reinsurance earnings to purchase real estate, fund college education, and reinvest in dealership operations

- Tax planning advantages — reinsurance companies may qualify for favorable tax treatment under IRC Section 831(b), which is covered below. Consult a qualified tax advisor for specifics applicable to your situation

What Is Excess Insurance?

IRMI defines excess insurance as "a policy or bond covering the insured against certain hazards and applying only to loss or damage in excess of a stated amount or specified primary or self-insurance." The key word: insured. This is coverage for the policyholder — not a risk transfer between insurance companies.

Excess insurance activates once the underlying primary policy's limits are exhausted. The excess insurer then pays the portion of a claim that exceeds those limits, up to its own stated limit.

Straight Excess vs. Umbrella-Style Coverage

These two terms get conflated, but they behave differently:

- Straight excess: Covers only the amount above the primary policy's limits. Does not "drop down" to cover losses if the primary insurer becomes insolvent — a distinction confirmed by the Tenth Circuit in Canal Ins. Co. v. Montello, Inc. (2015). Generally less expensive for this reason.

- Umbrella-style excess: May offer broader coverage across multiple underlying policies and can drop down to provide primary-basis coverage when underlying insurance is unavailable.

There is no profit-participation mechanism in either structure. Premiums paid for excess coverage are a pure expense — no underwriting upside, no reserves returned.

Use Cases of Excess Insurance

Excess insurance is common in commercial lines where businesses need coverage beyond standard primary limits:

- Construction firms managing project liability exposure

- Manufacturers with product liability risk

- Businesses with commercial general liability, property, or commercial auto policies

For example: a primary commercial liability policy covers up to $500,000. A claim totals $750,000. The excess policy pays the remaining $250,000. The business is protected from the overage — but the premium paid for that protection is gone.

Excess insurance is purely a protection tool. Dealers sometimes encounter the term and assume it relates to reinsurance, but the two structures serve entirely different purposes — and only one of them creates a financial asset for the dealership.

Which Structure Fits Your Needs?

The structural divide is clear: excess insurance is a protection-only tool for businesses managing liability exposure. Reinsurance is a risk-transfer mechanism between insurance entities — and for auto dealers, it represents an opportunity to participate in the profit chain rather than simply buying protection from it.

Situational Fit

Choose excess insurance when:

- You need to extend your liability limits as a business

- Your primary policy limits are insufficient for your risk exposure

- You're in construction, manufacturing, or another commercial sector with high-limit liability requirements

Choose (or establish) a reinsurance arrangement when:

- You sell insurance-backed products like vehicle service contracts, GAP, or ancillary F&I coverage

- You want to capture the underwriting profit those products generate rather than paying it to a third party

- You're looking to build a separate, income-generating financial structure alongside your dealership

Tax and Financial Implications

This is where the two structures diverge most sharply. Excess insurance is a business expense with no associated tax planning strategy. Reinsurance — specifically a dealer-owned reinsurance company — operates as a separate legal entity with its own tax treatment.

Dealer-owned reinsurance companies may qualify for treatment under IRC Section 831(b), which allows qualifying small property and casualty insurance companies to be taxed only on investment income rather than underwriting profit. Reserve funds can be invested conservatively in government bonds initially, with more aggressive options available once reserves exceed required levels.

These structures also create deferred income opportunities and distinct wealth-building mechanisms that do not exist when you're paying premiums to a third-party provider.

Note: These are general descriptions of how the structures work. Tax implications vary by entity structure, state, and individual circumstances. Always consult a qualified CPA or tax attorney before establishing a reinsurance company.

The Practical Takeaway for Auto Dealers

If you're currently using third-party F&I product providers — and most dealers are — you're funding underwriting profits that flow to someone else's company, not yours. That's the core issue reinsurance solves.

As DealerRE notes: "If your current third-party warranty provider weren't making a profit off of you or taking a loss, why would they continue to do business with you?" Those providers are profitable because they retain the underwriting income your customers' premiums generate.

A dealer-owned reinsurance program — with proper structure, A-rated backing, and expert administration — is how dealers take that profit back. It's not reserved for large dealer groups. Dealers selling more than 30 cars per month are typically positioned to benefit, though the threshold varies by program.

Conclusion

Reinsurance and excess insurance are not competing products. They serve different parties and solve different problems. Excess insurance protects a policyholder from catastrophic liability exposure above their primary policy limits. Reinsurance manages and redistributes risk at the insurer level — and for dealers, owning a piece of that structure means owning a piece of the profit.

The relevant question for auto dealers isn't which coverage to buy. It's whether you're participating in the profit side of the insurance products you already sell.

Dealers who understand this distinction keep more of what they earn through:

- Reserve investment income generated inside their own reinsurance company

- Tax planning advantages tied to dealer-owned program structures

- Direct ownership of underwriting income instead of ceding it to third-party providers

That shift — from buyer to owner — is where real, compounding financial advantage starts.

Frequently Asked Questions

What is the difference between excess insurance and reinsurance?

Excess insurance is purchased by a policyholder to extend coverage beyond a primary policy's limits; the insured pays premiums and receives additional protection. Reinsurance is a contract between two insurance companies where the primary insurer transfers risk to a reinsurer. The policyholder is not a party to the arrangement and typically has no knowledge it exists.

What is an example of excess insurance?

A business holds a commercial liability policy with a $1 million limit and faces a $1.5 million claim. The primary policy pays its $1 million limit; the excess policy covering the next $500,000 pays the remaining balance, making the business whole.

What is per risk excess of loss reinsurance?

Per risk excess of loss reinsurance covers individual risks — such as a single policy or property — where the reinsurer pays the portion of a claim exceeding the primary insurer's retention on that specific risk, up to the reinsurance limit. This differs from per event (or catastrophe) XoL, which aggregates multiple individual claims from the same event.

What is the difference between XoL and surplus?

Excess of loss (XoL) is a non-proportional reinsurance structure where the reinsurer pays only above a set retention threshold, describing how risk is shared between insurers. Surplus lines refers to insurance placed with non-admitted carriers for risks the standard market won't cover, describing where insurance is placed rather than how losses are divided.

What does "£200 excess" mean?

In UK and Australian personal insurance, a "£200 excess" (or equivalent) refers to the deductible: the out-of-pocket amount the policyholder pays before the insurer covers the rest of a claim. This use of "excess" as a deductible is unrelated to "excess insurance," which is a separate policy extending coverage limits above a primary policy.