Introduction

Picture an insurance company with a balance sheet cluttered by old workers' compensation claims from five years ago — still open, still uncertain, still tying up capital that could be deployed elsewhere. The liabilities are real, the reserves are set aside, but no one knows exactly when those claims will close or what they'll ultimately cost. That uncertainty has a price.

Loss Portfolio Transfers (LPTs) exist to solve exactly this problem. By transferring a defined block of existing liabilities — along with the reserves backing them — to a reinsurer, the ceding company converts open-ended uncertainty into a fixed, known cost. That predictability frees up capital and removes the drag of long-tail exposure from the balance sheet.

LPTs are used across a range of scenarios: insurers exiting a line of business, captives winding down, self-insured employers recovering collateral, and companies navigating M&A transactions. Dealers managing their own admin-obligor reinsurance programs encounter this structure too, making it worth understanding.

This article covers the definition, mechanics, key benefits, common use cases, and primary risks of LPTs — with straightforward explanations at every step.

TL;DR

- An LPT transfers existing loss liabilities and reserves from a cedent to a reinsurer, who assumes full claims responsibility

- The premium is discounted below full reserve value, reflecting the time value of money

- Reinsurers profit by investing transferred reserves before claims are paid

- Benefits include balance sheet relief, freed-up capital, lower admin costs, and cleaner M&A transactions

- Primary risks: reinsurer insolvency and claims exceeding projected reserves

What Is a Loss Portfolio Transfer (LPT) in Reinsurance?

The Core Definition

According to IRMI, an LPT is "a financial reinsurance transaction in which loss obligations that are already incurred and will ultimately be paid are ceded to a reinsurer." The cedent transfers both the asset (reserves) and the obligation (future claim payments) to the reinsurer in a single structured transaction.

This is what separates LPTs from standard prospective reinsurance. Traditional reinsurance covers future, unknown underwriting risk — events that haven't happened yet. An LPT deals with liabilities that already exist, including:

- Case reserves — known, reported claims with estimated costs

- IBNR claims — losses incurred but not yet reported to the insurer

IBNR is particularly significant for long-tail lines. A workers' compensation claimant might not file for years after an injury occurs. LPTs cover both categories, giving the reinsurer full exposure to the run-off. That complexity is also what makes pricing an LPT a distinct discipline.

How Pricing Works

Because the reinsurer is taking on payment obligations that will be settled over time — not immediately — the premium is calculated using the present value of expected future losses, discounted for the time value of money. This means the cedent pays less than the full face value of the reserves.

Several factors influence the final price:

- Projected payment timing (faster payouts reduce reinsurer investment income)

- Investment return assumptions on the transferred reserves

- Loss development expectations and reserve adequacy

- Broker commissions and due diligence costs

As IRMI notes, "the cedent's statutory surplus increases by the difference between the premium and the amount that had been reserved" — a direct, measurable benefit on the balance sheet.

What Can Be Transferred

LPTs can be scoped narrowly or broadly depending on what the cedent needs to exit. Common transfer structures include:

- A specific line of business (workers' compensation, auto liability, general liability)

- A defined set of accident years

- A specific geographic territory

- A bounded group of policies

On transaction size, Artex's 2022 case study data suggests deals are often best suited in the $5 million to $50 million range, with a minimum of approximately $2 million in accrued liabilities for a single line.

How Does an LPT Work? The Mechanics Explained

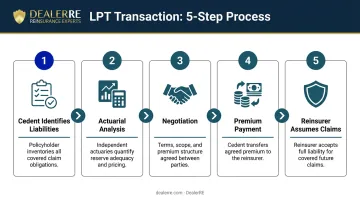

The Transaction Sequence

The basic structure follows a straightforward path:

- Cedent identifies the block of liabilities to be transferred — specific lines, accident years, or policy groups

- Actuarial analysis establishes reserve levels and projected payment patterns

- Negotiation determines the premium, coverage limits, and any aggregate caps

- Premium payment is funded by the transferred reserves, plus any additional consideration

- Reinsurer assumes claims management and payment responsibility going forward

The reinsurer then invests the transferred reserves, aiming to earn investment income before claims are paid out. As Investopedia explains, "the reinsurer expects to generate investment income from the transferred reserves before claims are actually paid, which allows the insurer to often receive a discount on the premium."

Risks the Reinsurer Accepts

Two primary risks define the reinsurer's position in any LPT:

- Timing risk — if claims resolve faster than projected, the reinsurer earns less investment income on the reserves before payout

- Investment risk — if market returns underperform assumptions, the reinsurer's profit margin shrinks

NAIC SSAP 62R requires that it be "reasonably possible that the reinsurer will realize a significant loss from the transaction" for the contract to qualify as reinsurance rather than a deposit arrangement. Without both risks present, regulators may reclassify the transaction entirely.

The Cedent's Residual Obligation

An LPT transfers the economic burden of outstanding claims — but not the cedent's regulatory obligation to policyholders.

Even after the transaction closes, the original insurer remains primarily liable if the reinsurer becomes insolvent and stops paying claims. The cedent must still fulfill those obligations regardless.

That's why reinsurer financial strength is a non-negotiable evaluation criterion before entering any LPT.

Key Benefits of a Loss Portfolio Transfer

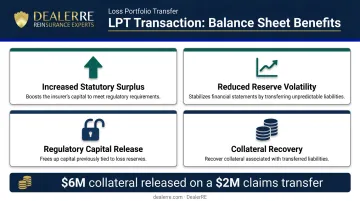

Balance Sheet Relief and Capital Release

When a company with $10 million in workers' compensation reserves transfers those liabilities to a reinsurer for $8 million, it frees $2 million in surplus and eliminates ongoing reserve volatility. That's a documented example from captives.insure's 2025 analysis of LPT transactions.

At the larger end of the spectrum, AXIS Capital's April 2025 LPT with Enstar on pre-2022 casualty reserves generated an approximately $60 million benefit from the excess of reserves ceded over consideration paid.

Other balance sheet impacts include:

- Increased statutory surplus

- Reduced reserve development volatility

- Release of regulatory capital previously held against liabilities

- Recovery of posted collateral (one Safety National case study documented $6 million in collateral released on a $2 million claims transfer)

Eliminating Long-Tail Uncertainty

Workers' compensation, general liability, and professional liability claims can take years — sometimes decades — to fully resolve. Medical inflation, statutory benefit changes, and judicial shifts all affect the ultimate cost.

An LPT converts that open-ended exposure into a defined transaction. The cedent's future obligation is capped at the agreed premium, regardless of how claims ultimately develop.

Administrative Cost Savings and Clean Business Exits

Once an LPT closes, the cedent avoids the ongoing cost of running a claims tail. For companies exiting a line of business, that means real savings on:

- Claims staffing and administration

- Actuarial analysis and reserve updates

- Compliance management and regulatory filings

Without an LPT, the alternative is maintaining that entire infrastructure for years while the portfolio slowly runs off.

That same cost-containment logic applies directly to M&A transactions. When one company acquires another, inherited prior-period liabilities can complicate valuations and create hidden financial exposure. An LPT allows legacy claims to be ring-fenced and transferred, giving the acquiring company a clean financial picture from day one.

Common Use Cases for Loss Portfolio Transfers

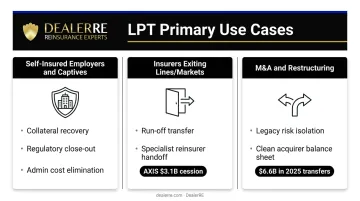

Self-Insured Employers and Captives Exiting Programs

Self-insured employers and captive insurance structures are among the most frequent LPT users. When a company exits its self-insurance program — whether due to business changes, cost pressures, or shifting risk appetite — accumulated workers' compensation and liability claims don't disappear. An LPT formally transfers those liabilities to a carrier, enabling the entity to:

- Recover posted collateral that was securing open obligations

- Close out regulatory obligations with state workers' compensation boards

- Eliminate ongoing administrative costs associated with claims management

Insurers Exiting Lines of Business or Geographic Markets

An insurance company withdrawing from workers' compensation in a specific state, or exiting a regional auto liability book, doesn't want to maintain a claims operation for years after writing its last policy. An LPT transfers those run-off obligations to a specialist reinsurer focused on efficient claims management and long-duration reserve investment.

The AXIS Capital/Enstar transaction announced in December 2024 illustrates this at scale: AXIS ceded $3.1 billion in reinsurance segment reserves (predominantly pre-2022 casualty portfolios) to Enstar, advancing its strategic shift toward specialty underwriting. Regulatory approvals — standard for transactions at this scale — were required before closing.

Mergers, Acquisitions, and Corporate Restructuring

According to PwC's 2025 Global Insurance Run-Off Survey, approximately $6.6 billion in gross liabilities transferred to legacy market participants in just the first eight months of 2025, across 25 publicly announced deals. That volume reflects how central LPTs have become in corporate transactions.

When companies inherit liabilities through acquisitions, an LPT provides a structured path to isolate and transfer those legacy risks — rather than absorbing unpredictable claim development into the acquirer's balance sheet.

Risks and Considerations in an LPT Transaction

Reinsurer Insolvency Risk

The cedent's residual policyholder obligation makes reinsurer financial strength the single most important factor in LPT counterparty selection. If the reinsurer fails, the original insurer must still pay claims — despite having already transferred the economic risk.

Mitigation typically involves selecting highly rated counterparties. Enstar's subsidiary Cavello Bay Reinsurance, used in the AXIS transaction, carries both S&P "A" and AM Best ratings. Safety National, a frequent LPT provider for self-insured workers' compensation, holds an AM Best A+ (Superior) rating.

Adverse Loss Development

If actual claims exceed the projections used to price the LPT, the reinsurer absorbs losses — but only up to the transaction's aggregate limits. Many deals include excess cover layers for precisely this reason:

- The Enstar/SiriusPoint $400 million workers' compensation LPT included $200 million of additional cover above ceded reserves

- The Enstar/QBE deal included $175 million of additional coverage beyond ceded reserves

Cedents should understand clearly what is excluded from coverage and where their residual exposure begins if development exceeds the LPT's limits.

Regulatory and Accounting Complexity

LPTs face specific accounting treatment under NAIC SSAP 62R: they must be classified as retroactive reinsurance, and any gain recognized at inception goes into a special surplus account (not unassigned funds) until actual claims paid by the reinsurer exceed the consideration paid. If the contract fails to meet risk transfer requirements, deposit accounting applies and no reserve credit is taken.

Beyond accounting treatment, closing an LPT requires navigating several additional layers:

- Most states require regulatory approval before closing, as both the AXIS/Enstar and Enstar/SiriusPoint transactions confirmed

- Actuarial work to establish reserve levels, payment projections, and investment return assumptions must be completed before pricing is finalized

- Each of these requirements adds meaningful time and professional fees to the transaction timeline

Parties entering an LPT should budget for this process early — delays in regulatory or actuarial work are among the most common reasons transactions take longer than expected.

What LPTs Mean for Dealer-Owned Reinsurance Programs

Most dealer-owned reinsurance programs — including the admin-obligor structures DealerRE administers — are designed as prospective, ongoing programs, not run-off vehicles. Dealers are writing new vehicle service contracts, GAP coverage, and ancillary F&I products continuously, with reserves accumulating and claims being paid in parallel.

That said, understanding LPT mechanics matters in a few specific scenarios:

- Program wind-down — if a dealer retires, sells the dealership, or decides to exit their reinsurance program, open claims and accumulated reserves need to be resolved through a structured process

- Dealer group acquisitions — when a dealership changes hands, the buyer may not want to inherit the seller's open F&I reinsurance obligations

- Program restructuring — transitioning from one program structure to another may require isolating and resolving legacy liabilities before the new structure goes live

DealerRE's admin-obligor structure includes built-in protections that reduce the likelihood of a complex exit being necessary. Reserve funds are held in US-based Trust Company accounts, withdrawals require underwriting insurance company approval, and regulatory guidelines require maintaining reserves at 125% of unearned premiums — a conservative standard that keeps programs adequately funded.

Those protections also make transitions more manageable when they do occur. DealerRE has helped over 400 auto dealers build and manage admin-obligor reinsurance programs since 1994, providing full-service administration including claims adjudication, compliance, financials, and all regulatory filings.

That track record means dealers have a partner who knows how programs are structured, how reserves should be maintained, and what resolution options exist — whether a transition is planned or unexpected.

Frequently Asked Questions

What is LPT in reinsurance?

LPT stands for Loss Portfolio Transfer: a reinsurance transaction where a cedent transfers existing loss liabilities and related reserves to a reinsurer, who then assumes responsibility for paying those claims. The premium is discounted below full reserve value to reflect the time value of money and expected investment income.

What is the difference between a loss portfolio transfer and a commutation?

A commutation terminates an existing reinsurance agreement between original contracting parties, with a lump-sum settlement sending risk back to the cedent. An LPT moves risk forward to a new third-party reinsurer, who then manages and pays claims over the run-off period.

How is the premium for a loss portfolio transfer calculated?

LPT premiums are based on the present value of estimated future claim payments, discounted for the time value of money. The reinsurer's expected profit comes from investment income earned on the reserves before claims are paid, which is why the cedent receives a discount below full carried reserves.

What risks does the reinsurer take on in an LPT?

The reinsurer accepts timing risk (claims paid out faster than projected, reducing investment income) and investment risk (returns on transferred reserves fall short of assumptions). Both reduce profitability and must be present for the transaction to qualify as reinsurance under NAIC accounting standards.

What happens if the reinsurer in an LPT becomes insolvent?

The original insurer remains legally responsible to its policyholders even after the LPT closes. The transfer shifts economic risk, not the regulatory obligation. That's why reinsurer financial strength ratings matter when selecting a counterparty.

Can LPTs be used in dealer-owned reinsurance programs?

While most dealer-owned admin-obligor programs are prospective in nature, LPT-like mechanisms can be relevant when a dealer restructures, sells, or winds down a program. DealerRE helps dealers structure and administer those transitions — including program wind-downs and restructuring — so the right reinsurance framework is in place before issues arise.