What Auto Dealers Need to Know About RAD Reinsurance

Picture this: a dealer's reinsurance contract year ended last December, but a customer files a VSC claim in March for a mechanical breakdown on a vehicle sold the previous October. The dealer's reinsurance company pays the claim — and the dealer wonders why coverage is still active.

The answer is the risk attaching basis.

Not all reinsurance contracts trigger coverage the same way. Some respond based on when a loss occurs. Others respond based on when the original policy was written.

For dealers running their own reinsurance companies, that distinction isn't a technical footnote: it determines whether claims get covered, how premiums are accounted for, and what happens when a contract ends.

This article covers:

- What RAD (Risk Attaching During) means and how coverage is triggered

- How it works inside a dealer reinsurance program

- How it compares to LOD (Loss Occurring During)

- Why the structure matters for VSCs, GAP, and other long-tail F&I products

TL;DR: Key Takeaways

- RAD coverage is triggered by policy inception date — not when the loss happens

- All F&I products written during the treaty period stay covered, even if claims emerge years later

- VSCs are long-tail products: actuarial data shows only 5% of losses emerge in year one, peaking in years 3–4

- RAD includes built-in run-off protection; LOD does not

- Multi-year premium accounting under RAD requires strong back-office support to manage accurately

What Does RAD Mean in Reinsurance?

RAD stands for Risk Attaching During — a reinsurance contract structure where the reinsurer covers losses from any policy that incepted (was written, renewed, or came into force) during the reinsurance contract period, regardless of when the actual claim occurs.

The coverage trigger is the policy's start date, not the loss date — which means a claim filed years after the contract period ends can still be the reinsurer's responsibility, as long as the underlying policy was written during the covered term.

Insurance Business Magazine explains: "Coverage is determined by the policy's start date rather than when a loss occurs." IRMI's foundational analysis confirms RAD (also called "policy attaching during") covers "reinsured losses on policies attaching — i.e., incepting — during the reinsurance contract period."

That timing distinction has real operational consequences for dealers. Here's how it plays out in practice.

A Concrete Dealer Example

Say a dealer's reinsurance contract runs from January 1 to December 31. A VSC is sold on October 15. The customer files a mechanical breakdown claim in March of the following year.

Under RAD, that claim is covered — because the VSC incepted within the contract period. The reinsurer doesn't care that the breakdown happened after December 31.

Why This Matters for F&I Products

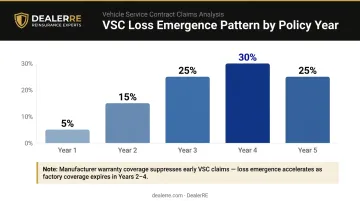

VSC terms commonly run 5 to 7 years for new vehicles and 1 to 3 years for used vehicles. Claims don't emerge evenly across that window. For a standard 5-year new-car VSC, actuarial data shows a heavily back-loaded emergence pattern:

| Policy Year | % of Total Losses |

|---|---|

| Year 1 | 5% |

| Year 2 | 15% |

| Year 3 | 25% |

| Year 4 | 30% |

| Year 5 | 25% |

Claims are effectively zero while the manufacturer's warranty is in effect — meaning the bulk of liability surfaces long after the point of sale. RAD is designed for exactly this kind of tail. Without it, dealers would face a structural mismatch between when premiums are ceded and when claims actually land.

How Risk Attaching Basis Works in a Dealer Reinsurance Program

Mapping the Process Step by Step

Step 1 — Treaty established. The dealer's reinsurance company (typically an admin obligor structure) enters into a RAD-basis treaty with a carrier for a defined period. All F&I products issued during that window will attach to this treaty.

Step 2 — Policies attach as they're written. Each VSC, GAP policy, or other covered product sold by the dealer becomes part of the treaty as of its inception date. The sale date is the anchor.

Step 3 — Claims are evaluated against inception date, not loss date. When a claim arrives, the relevant question is: "When was this policy sold?" If the answer falls within the treaty period, the reinsurer responds — even if the breakdown happened two years later.

Step 4 — Coverage continues after the contract expires. Once the RAD treaty period ends, no new policies attach. But every policy already written during the period stays covered through its natural expiration. This run-off protection is built into the structure — no separate endorsement required.

Step 5 — Premium accounting spans multiple periods. Because claims on incepted policies emerge over time, premium income and loss development need to be tracked across two or more accounting years. This is the administrative trade-off that comes with RAD's broader protection.

That tracking complexity is exactly where purpose-built administration matters. DealerRE's full-service model handles claims adjudication, compliance management, bookkeeping, and performance reporting across treaty years, so dealers can stay focused on selling rather than managing back-office detail.

RAD vs. LOD: Key Differences Every Dealer Should Understand

LOD (Loss Occurring During) flips the coverage trigger: the reinsurer covers any claim where the loss event happens during the treaty period, regardless of when the original policy was sold. A breakdown on November 5 is covered by the treaty active that November.

That simplicity makes LOD attractive — but it creates real gaps for long-tail F&I products like VSCs.

Here's how the two structures compare across the dimensions that matter most to dealers:

The Structural Difference, Side by Side

| Dimension | RAD | LOD |

|---|---|---|

| Coverage trigger | Policy inception date | Date of loss |

| In-force policies at treaty start | Generally excluded | Included |

| Run-off after expiration | Built in — liability follows incepted policies | Liability ends when treaty ends |

| Premium basis | Written premium during treaty | Earned premium during treaty |

| Best suited for | Long-tail, liability, complex lines | Short-tail, property, catastrophe |

| Claims administration | More complex — tracks inception dates | Simpler — tracks loss occurrence dates |

The Run-Off Problem With LOD

Under LOD, if a dealer doesn't renew their reinsurance contract, losses occurring after the termination date are simply not covered. That means a customer who bought a VSC 18 months ago and experiences a breakdown the day after the contract lapses gets nothing.

Unless a specific run-off clause is negotiated, the dealer absorbs that exposure directly.

RAD eliminates this risk structurally. Every policy incepted during the treaty period stays protected through the life of that contract. No separate negotiation required.

Accounting and Premium Differences

LOD contracts typically involve a single premium adjustment at year-end based on the written premium for the period — clean and straightforward. RAD contracts require premium adjustments over two or more years as incepted policies generate claims. That complexity demands careful reserve management, but it also aligns premium recognition with the actual liability being assumed.

For short-tail or property-style risks where losses are reported quickly, LOD offers simplicity that makes sense. For VSCs and other long-tail F&I products — where the SOA notes that unearned premium reserves can be 10 to 20 times larger than claim reserves — RAD's structure provides far more comprehensive and predictable protection.

Advantages of Risk Attaching Basis for Dealer-Owned Reinsurance

Built-in run-off protection. When a RAD contract ends or isn't renewed, there's no coverage gap for previously sold F&I products. Every incepted policy stays protected through its natural expiration. That eliminates one of the most significant financial risks in program transitions.

Precise treaty-year accountability. Because coverage is anchored to inception date, dealers and their program administrators know exactly which products are reinsured under which treaty year. That clarity simplifies claims adjudication, financial reporting, and reinsurance recoveries. DealerRE's administration model is built around this kind of policy-level tracking.

Alignment with long-tail product lifecycles. VSCs commonly remain in force for three to five years or longer. RAD ensures reinsurance coverage mirrors the full duration of the underlying product liability, covering the product from inception through expiration rather than limiting exposure to a single calendar year. A dealer who sells a 6-year VSC in October shouldn't have to worry about whether reinsurance coverage expires before the contract does.

Premium stays where it belongs — in the dealer's program. With F&I gross profit per vehicle averaging $2,501 for publicly owned dealers in Q4 2024, the pool of premium available for dealer reinsurance participation is substantial.

RAD ensures that once a VSC premium is ceded into the dealer's reinsurance entity, the full lifecycle of that contract stays within the dealer's financial control. That includes the years when investment income accrues on reserves before claims peak — a meaningful source of return that would otherwise flow to a third-party provider.

Potential Drawbacks and Considerations

No structure is without trade-offs. RAD's advantages come with real administrative and financial considerations dealers need to plan for.

Three considerations deserve attention before structuring a RAD program:

- Pricing complexity: The reinsurer stays exposed to claims long after the treaty period closes. That extended horizon of uncertainty gets priced into the program, and dealers need to understand what they're buying.

- Accounting overhead: Premium income develops across multiple years, with loss emergence patterns that don't map cleanly to a single accounting period. Robust back-office support — monthly financials, performance reporting, ongoing loss monitoring — isn't optional for a program built this way.

- Carrier solvency risk: Under a RAD contract, a reinsurer that becomes financially impaired after the contract period ends still carries live obligations. IRMI notes that some ceding companies prefer cut-off clauses over run-off precisely because of solvency concerns.

That last point is where program structure becomes a real differentiator. DealerRE's admin obligor model — backed by A-rated carriers — addresses this directly. If the dealer's reinsurance company cannot meet its obligations, the ultimate liability for claim payments rests with the direct writing insurance company. The dealer's exposure is limited to formation costs plus accumulated earnings. In a long-tail RAD program, that backstop is a structural feature, not an afterthought.

Frequently Asked Questions

What does RAD mean in reinsurance?

RAD stands for "Risk Attaching During" — a reinsurance contract basis where coverage applies to all policies written during the contract period, regardless of when a claim or loss occurs. The coverage trigger is the policy's inception date, not the date of the breakdown or claim filing.

How is risk attaching basis different from loss occurring reinsurance?

RAD covers claims tied to when a policy was written; LOD (Loss Occurring During) covers claims tied to when the actual loss event takes place. The key practical difference is run-off: RAD provides automatic coverage continuity for incepted policies after a contract ends, while LOD does not.

Why do dealer-owned reinsurance programs use risk attaching basis?

VSCs and other F&I products are long-tail contracts where most claims emerge well after the sale date — often years later. RAD ensures coverage follows the full life of each product rather than a single calendar window of loss events, which fits how VSCs and GAP products actually behave.

What happens to RAD coverage when a dealer's reinsurance contract ends or isn't renewed?

All policies incepted during the treaty period remain covered through their natural expiration — that's the built-in run-off benefit. No separate run-off negotiation is required, unlike LOD, which can leave gaps when coverage lapses.

Does risk attaching basis affect premium accounting in a dealer's reinsurance company?

Yes. Because policies written during the treaty period can generate claims over multiple years, premium income and loss development are tracked across more than one accounting period. Dealers need solid administrative support — specifically monthly financial reporting and multi-year loss monitoring — to manage this accurately.

Is RAD or LOD better for a dealer-owned reinsurance program?

For most dealer F&I programs, RAD is the better fit — its run-off protection and alignment with long-tail product lifecycles match how VSCs and GAP products behave. Long-tail products almost always point toward RAD, though your specific product mix and administrative capabilities are worth confirming with your program administrator.