These aren't isolated deals. They're part of a deliberate shift toward what F&G calls a capital-light, fee-based business model — one where third-party capital funds growth rather than F&G's own balance sheet carrying every annuity obligation.

Understanding what F&G is doing, and why, matters beyond Wall Street. The underlying principle — that whoever owns and controls the reinsurance structure captures the profit — applies whether you're managing $73 billion in assets or running a dealership F&I program.

TL;DR

- August 2025: F&G partnered with a Blackstone-backed reinsurer on a forward flow quota share arrangement, with ~$1B in anticipated capital commitments

- February 2026: F&G sold Bermuda subsidiary F&G Life Re to Ancient Financial (future Ancient Re) for ~$300M in net proceeds and entered a new flow reinsurance agreement

- The pattern: F&G has used the same sell-and-flow playbook since 2020 — externalizing ownership while retaining origination and distribution

- The tradeoff: Capital freed from holding subsidiaries — counterparty risk grows with each third-party relationship replacing a captive structure

Who Is F&G Annuities & Life?

Founded in 1959 as Fidelity & Guaranty Life Insurance Company, F&G is headquartered in Des Moines, Iowa, and trades on the NYSE under the ticker FG. Fidelity National Financial (FNF) holds an approximately 85% majority stake, making FNF the ultimate parent entity — relevant context for investors researching F&G Global Funding, a special-purpose vehicle used by F&G's insurance subsidiaries.

F&G's product focus centers on:

- Fixed indexed annuities (FIAs) — its core retail product, first introduced in 1998

- Pension risk transfer (PRT) — serving institutional clients seeking to offload defined benefit obligations

- Funding agreements — contributing to the institutional segment through F&G Global Funding

As of December 31, 2025, F&G reported record retained AUM of $57.6 billion (up 7% year-over-year), with AUM before flow reinsurance reaching $73.1 billion. Gross sales for FY 2024 hit $15.3 billion — triple the 2020 figure.

That growth directly drives the reinsurance restructuring. FIA sales reached $126.9 billion industry-wide in 2024 — a 32% annual increase — and hit $127.9 billion in 2025, marking the fifth consecutive year of record sales. At that scale, flow reinsurance becomes a structural requirement, not an optional capital management tool.

F&G's History of Reinsurance Restructuring

The Blackstone and Ancient Financial deals follow a playbook F&G established in 2020.

The 2020 Aspida Transaction

On September 30, 2020, F&G announced the sale of F&G Reinsurance Ltd. — its Bermuda-based subsidiary holding approximately $2 billion in invested assets — to Aspida Holdings Ltd., an indirect subsidiary of Ares Management Corporation.

The structure set the template: sell the Bermuda entity, then immediately enter a flow reinsurance agreement with the buyer. In this case, F&G and Aspida agreed to a MYGA (multi-year guaranteed annuity) flow reinsurance agreement on a coinsurance fund withheld basis. F&G described the arrangement as enhancing its competitive positioning while freeing proceeds for growth.

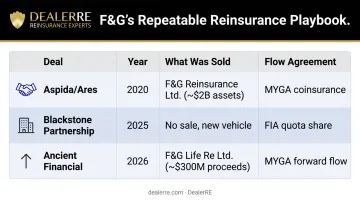

The Repeatable Playbook

Three transactions over six years follow the same core structure:

| Deal | Year | What Was Sold | Flow Agreement |

|---|---|---|---|

| Aspida/Ares | 2020 | F&G Reinsurance Ltd. (~$2B assets) | MYGA coinsurance |

| Blackstone Partnership | 2025 | No sale — new vehicle | FIA quota share |

| Ancient Financial | 2026 | F&G Life Re Ltd. (~$300M proceeds) | MYGA forward flow |

In each case, F&G separates the economic ownership of reinsurance capacity from its operational access to it — retaining distribution control while transferring the liability and balance sheet weight to a capital partner.

The 2025 Blackstone Partnership: F&G's Capital-Light Growth Strategy

What Was Announced

On August 6, 2025, F&G announced a strategic partnership with a new reinsurance vehicle backed by Blackstone managed funds, with approximately $1 billion in anticipated capital commitments. The arrangement is a forward flow reinsurance agreement on a quota share basis covering certain fixed indexed annuity products, effective August 1, 2025 (the reinsurance vehicle's name was not publicly disclosed).

How It Works in Plain Language

A forward flow quota share works differently from a bulk policy transfer. Instead of moving an existing block of policies in one deal, F&G cedes a defined percentage of newly written FIA premiums — along with the related liabilities — to the Blackstone-backed entity as each new policy is issued.

For F&G, this means:

- New FIA volume flows continuously to the reinsurance partner

- F&G's capital requirements for that ceded portion transfer with it

- Balance sheet capacity expands to support more volume without requiring additional capital raises

CEO Chris Blunt described it as "an important step in F&G's continued evolution to a more fee-based, higher margin, and less capital-intensive business, with the expectation to expand its return on equity over time."

Why Blackstone?

F&G's investment management relationship with Blackstone dates to 2017 — making this an extension of an established arrangement rather than a new introduction. The choice also reflects a broader dynamic: alternative asset managers actively seek stable, long-duration insurance liabilities because those cash flows pair well with their private credit and alternative investment strategies.

That pattern is already established at scale. Blackstone's 2022 strategic partnership with Resolution Life — which involved $3 billion in new equity capital commitments and a target of managing up to $25 billion in assets — shows how consistently alternative managers are building insurance liability platforms to anchor long-duration asset deployment.

The Ancient Financial Deal: Selling F&G Life Re

The Transaction

On February 19, 2026, Ancient Financial — a newly formed financial services company — announced a definitive agreement to acquire F&G Life Re Ltd., F&G's Bermuda-based reinsurance subsidiary, and rename it Ancient Re Ltd. Simultaneously, F&G entered a forward flow reinsurance agreement with Ancient Re covering MYGA new business.

F&G expected approximately $300 million in net proceeds from the sale. The company had already recaptured roughly $900 million — about one-third of F&G Life Re's statutory reserves — in preparation for the planned transaction.

Who Is Ancient Financial?

Ancient Financial launched as a specialized reinsurance and asset management platform for the life and annuity sector. It operates independently of any existing insurance company or asset manager — describing its model as an "open-architecture approach to assets and liabilities." The firm is backed by equity commitments from Ancient Management LP, alongside institutional investors and single-family offices.

Its CEO, Erich Schram, is a founding partner of Blackstone Insurance Solutions (established 2019) and a former Senior Managing Director at Blackstone. That Blackstone thread runs through every recent F&G reinsurance transaction, either directly or through leadership lineage.

F&G's Rationale

Chris Blunt called it "a true win-win": F&G monetized a Bermuda entity that was "no longer needed to support our reinsurance strategy" while locking in a quality flow reinsurance partner going forward.

In practice, F&G sold the subsidiary, captured $300 million, and kept ongoing access to reinsurance capacity through the flow agreement — shedding the capital cost of ownership in the process.

The Risk Worth Noting

Analysts have flagged that restructured third-party reinsurance arrangements introduce counterparty and execution risk. A February 2025 analysis by Retirement Income Journal drew a comparison to the pre-2008 "originate-to-distribute" mortgage model — noting that when risks are continuously transferred to third parties, questions about alignment and durability arise.

No ratings agency has issued a formal downgrade tied to these specific transactions; all four major agencies — AM Best, S&P, Fitch, and Moody's — maintain stable outlooks on F&G's insurance subsidiaries as of early 2026.

What These Moves Signal for the Reinsurance Industry

A Systemic Shift in Who Holds the Risk

F&G isn't alone. AM Best's June 2025 special report confirmed that Bermuda "continues to maintain its role as a driving force in offshore reinsurance" and noted that "more companies may look to reinsurers to manage growth and capital levels." The FIA market's sheer scale — over $127 billion in annual sales — creates capital demands that internal balance sheets struggle to absorb efficiently.

The emerging model: large insurers retain distribution and underwriting expertise, then use third-party capital — from private equity, institutional investors, sovereign wealth funds — to hold the liabilities.

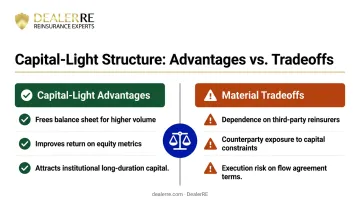

The Strategic Tradeoff

The capital-light model delivers clear advantages:

- Frees balance sheet for higher volume without proportional capital raises

- Improves return on equity metrics

- Attracts institutional capital seeking long-duration yield

The tradeoffs are material:

- Dependence on third-party reinsurers whose priorities can shift

- Counterparty exposure if a reinsurance partner faces capital constraints

- Execution risk if flow agreement terms prove unfavorable over time

A captive reinsurance structure eliminates those dependencies — the owner controls the terms, the claims experience, and the accumulated reserves.

What This Means at the Dealership Level

F&G's moves are sophisticated corporate strategy built for a publicly traded insurer managing billions in liabilities. But the underlying principle transfers directly to smaller-scale reinsurance structures.

Dealers who establish their own reinsurance companies through programs like DealerRE maintain direct ownership of their reinsurance structure — no third-party restructuring cycles, no exposure to outside capital providers deciding to exit the arrangement. The dealer's reinsurance company exists solely to reinsure that dealership's F&I business, meaning the claim experience, underwriting profits, and accumulated reserves all stay within the dealer's own structure.

DealerRE structures it this way intentionally: your reinsurance company "will only reinsure the business that your dealership writes through your F&I operations. No other company's operations will affect the profits or losses of your company." That's a degree of insulation from external capital market dynamics that F&G — operating at enormous scale with publicly traded obligations — simply cannot maintain.

What drove F&G to sell its Bermuda subsidiaries and enter flow agreements applies at any scale: whoever owns and controls the reinsurance structure captures the profit. That's as true writing 50 vehicle service contracts a month as it is managing $73 billion in AUM.

Frequently Asked Questions

What does F&G stand for?

F&G stands for Fidelity & Guaranty, derived from the company's original name, Fidelity & Guaranty Life Insurance Company. The Des Moines-based insurer now trades publicly on the NYSE under the ticker FG and operates as F&G Annuities & Life.

Who is F&G insurance?

F&G Annuities & Life is a leading U.S. provider of fixed indexed annuities, life insurance, and institutional insurance solutions. Headquartered in Des Moines, Iowa, it serves both retail customers and institutional clients, with record retained AUM of $57.6 billion as of year-end 2025.

Who is the parent company of F&G Global Funding?

F&G Global Funding is a special-purpose funding vehicle affiliated with F&G Annuities & Life. The ultimate parent is Fidelity National Financial (FNF), which holds approximately an 85% majority stake in F&G.

What is a forward flow reinsurance agreement?

A forward flow reinsurance agreement is an arrangement where a cedent agrees in advance to transfer a defined share of newly written policies to a reinsurer on an ongoing basis — as each policy is issued, rather than in a single block transfer — giving both parties predictable, continuous risk-sharing over time.

Why did F&G sell F&G Life Re to Ancient Financial?

F&G sold the Bermuda subsidiary because it was no longer essential to its reinsurance strategy. The sale generated approximately $300 million in net proceeds while F&G retained ongoing reinsurance capacity through a forward flow agreement with Ancient Re under its new independent ownership.

What is F&G's relationship with Blackstone?

Blackstone has managed F&G's investment portfolio since 2017. In August 2025, F&G deepened that partnership through a new Blackstone-backed reinsurance vehicle, bringing approximately $1 billion in capital commitments to support FIA growth via a quota share forward flow arrangement.