Introduction

Most dealers entering a reinsurance program ask one question: "What's the admin fee?" It's the most visible number on any program summary. But it's rarely the most important one.

The real cost of running a dealer-owned reinsurance program includes ceding fees, claims adjudication expenses, premium taxes, and a collection of ancillary charges that rarely appear in a program pitch. Individually, each line item looks manageable. Together, they determine how much premium actually reaches your reinsurance entity, and how much underwriting profit you actually keep.

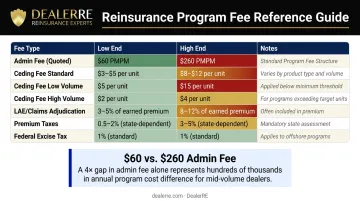

According to industry research, a quoted admin fee of approximately $60 per contract can balloon to $260 once hidden charges like loss adjustment expenses, capitalization fees, and state taxes are factored in. That's a $200-per-contract gap between the quoted price and the real one.

What follows is a breakdown of every fee category — what each covers, what a reasonable range looks like, and how the full structure determines what you actually keep.

TL;DR

- F&I reinsurance programs involve multiple fee layers — admin fees, ceding fees, premium taxes, and claims costs all reduce net underwriting profit.

- Admin fees are the most visible cost but often not the most damaging; ceding fees and loss adjustment expenses can have equal or greater cumulative impact.

- Published fee ranges vary widely — admin fees from under $100 to over $400 per contract, ceding fees from 1% to 15% or higher depending on volume.

- A dealer-owned admin obligor structure with a transparent administrator like DealerRE lets dealers capture underwriting profit instead of surrendering it to third-party providers.

What F&I Reinsurance Costs Are Really Paying For

Reinsurance fees are not arbitrary. They compensate administrators for functions that keep a dealer's reinsurance entity legally compliant, financially sound, and operationally functional.

Core functions covered by program fees typically include:

- Underwriting and contract processing

- Claims adjudication and payment

- Compliance management and state regulatory filings

- Financial reporting, bookkeeping, and tax returns

- F&I training and program performance analysis

Some of these costs are regulatory requirements — premium taxes exist regardless of which administrator you choose. Others reflect the service level your administrator actually delivers. Knowing which is which gives you a clearer basis for comparing programs side by side.

Retrocession vs. Dealer-Owned Admin Obligor: Why Structure Changes Your Fee Exposure

The two most common participation models dealers encounter are retrocession (retro) programs and dealer-owned admin obligor reinsurance companies.

In a retrocession (retro), the administrator reinsures the products and pays back a portion of underwriting profit to the dealer as a taxable commission. There's no entity formation, no separate legal structure, and the administrator absorbs most operational costs. The tradeoff: retro participants typically receive roughly 50% of potential underwriting profit, and that income is taxed at the dealership's standard income rate.

A dealer-owned admin obligor structure works differently. The dealer owns the reinsurance entity, participates in the full underwriting profit, and can also earn investment income on trust funds. The full fee stack applies — admin fees, ceding fees, premium taxes, and claims adjudication costs — but the dealer controls significantly more of the economic outcome.

| Feature | Retrocession | Dealer-Owned Admin Obligor |

|---|---|---|

| Entity formation required | No | Yes |

| Underwriting profit share | ~50% | Up to 100% |

| Investment income | No | Yes |

| Fee exposure | Low | Full stack |

| Dealer control | Limited | High |

The right model depends on where a dealer is in their F&I journey — and understanding that distinction shapes how every fee in the program should be evaluated.

The Main Fee Types in an F&I Reinsurance Program

Administrative Fees

The admin fee is charged per contract by the program administrator and covers contract processing, documentation, and program management. It may be quoted as a flat dollar amount per contract or as a percentage of premium.

This is the fee most dealers scrutinize during program comparisons. The problem is that focusing on admin fee in isolation misses every other cost category — and in some programs, those other costs dwarf the admin fee itself.

Ceding Fees

Ceding fees represent the percentage of premium retained by the administrator before funds transfer to the dealer's reinsurance entity. Even a small difference compounds significantly at scale.

Hypothetical example — same annual volume, different ceding fees:

Assume a dealer generates $500,000 in annual gross written premium.

- At a 2% ceding fee: Administrator retains $10,000 → Dealer's entity receives $490,000

- At a 5% ceding fee: Administrator retains $25,000 → Dealer's entity receives $475,000

That's a $15,000 annual difference on the same production volume. Claims, other fees, and investment income aren't even factored in yet. Over five years, that gap exceeds $75,000.

Published ceding fee ranges span from 1% to 15%, with volume playing a significant role. Dealers producing under $100,000 in annual premium may face retention rates of 15% to 20% or more. Those exceeding $250,000 annually can often negotiate below 10%.

Claims Adjudication Fees

Loss Adjustment Expenses (LAE) cover the cost of reviewing, processing, and paying claims. They typically range from 5% to 13% of the submitted claim amount. The problem: LAE is often bundled into total claims paid on cession statements rather than broken out as a separate line item.

Many dealers don't realize this cost exists until they request an itemized breakdown. If your administrator isn't separating LAE from net claims paid, you're likely underestimating your true cost of claims.

Premium Taxes

Premium taxes are levied when contracts are ceded to the reinsurance entity. The NAIC Service Contracts Model Act distinguishes between provider fees (generally not subject to premium taxes) and premiums for reimbursement insurance policies (which are taxable). Rates vary by state and product classification.

Practically, premium taxes typically cost 2% to 2.5% of net written premium. For offshore structures, a federal excise tax of 1% applies to reinsurance premiums paid to foreign entities — an additional cost layer that domestic structures may avoid.

Some administrators include premium taxes within the admin fee; others charge them separately. Ask your administrator for a full fee schedule before making any program comparisons — bundled taxes make apples-to-apples analysis impossible otherwise.

Ancillary and Operational Costs

Ancillary costs can include:

- Technology or reporting platform fees

- Compliance support charges

- Audit expenses

- Investment management fees

- Roadside assistance costs embedded in contract pricing

- Capitalization fees

Each line item may look small in isolation, but combined they reduce the premium entering your reinsurance account. If these costs aren't disclosed upfront, you won't see them until you review a detailed cession statement — by which point the program decision has already been made.

Typical Fee Ranges: What's Normal vs. Excessive

| Fee Type | Low End | High End | Notes |

|---|---|---|---|

| Admin fee (quoted) | ~$60/contract | $260+/contract | Gap reflects bundled hidden charges |

| Ceding fee (standard) | 1% of premium | 15% of premium | Volume-sensitive |

| Ceding fee (low volume, under $100K) | 15% | 20%+ | Plus premium taxes |

| Ceding fee (high volume, over $250K) | Below 10% | — | Negotiable at scale |

| LAE / Claims adjudication | 5% of claim | 13% of claim | Often buried in claims paid |

| Premium taxes | ~2% | ~2.5% | Varies by state and product |

| Federal excise tax (offshore) | 1% | — | Applies to foreign entity structures |

The spread between a quoted $60 admin fee and a true $260 all-in cost is the clearest illustration of why single-metric comparisons fail. That gap is where the real evaluation begins.

What Full-Service Administration Should Actually Include

A higher admin fee is not inherently a problem, provided it reflects genuine services delivered. A well-structured full-service program should cover:

- Claims adjudication and payment

- Compliance management and regulatory filings

- Financial reporting, bookkeeping, and tax returns

- F&I training (onboarding and ongoing)

- Performance reporting and program analysis

DealerRE's admin obligor program covers all of these functions under one transparent fee structure: no separate line items for technology, compliance updates, or audit expenses. The alternative is a bare-bones administrator who quotes a lower number but offloads compliance, training, and reporting to the dealer — or simply leaves those functions unaddressed.

The Compounding Effect of Fee Layers

The real damage from excessive fees is cumulative: every layer of cost reduces the net premium that actually reaches your reinsurance entity.

Less net premium means:

- Fewer funds generating underwriting profit

- A smaller trust balance earning investment income

- Reduced capacity to absorb claims without eroding surplus

Over a 5- to 10-year horizon, a 3% difference in ceding fees on a mid-volume program typically represents six figures in lost underwriting profit — before factoring in the lost investment income on those same funds.

How the Fee Structure Affects Your Net Underwriting Profit

The fundamental formula for reinsurance profitability is:

Net Premium − Claims = Underwriting Profit

Because fees are deducted before funds reach the dealer's reinsurance entity, they reduce the net premium base. Underwriting profit is sensitive to fee structure even when claim ratios remain stable.

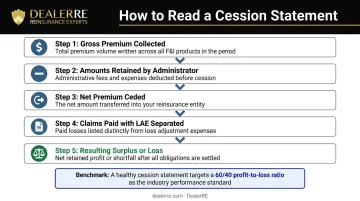

Reading Your Cession Statement

That sensitivity makes your cession statement the most practical tool for evaluating program health — it's where fee impact becomes visible. Issued quarterly, each statement should clearly show:

- Gross premium collected — total premium before any deductions

- Amounts retained by administrator — fees, ceding percentage, premium taxes

- Net premium ceded — what actually entered your reinsurance entity

- Claims paid — verify LAE is broken out separately, not buried here

- Resulting surplus or loss — the net financial position of your entity

A healthy program benchmark is a 60% profit / 40% loss ratio — meaning claims represent no more than 40% of net premium. VSC loss ratios in well-managed programs typically fall between 25% and 45%, with ancillary product loss ratios often under 20%.

Loss Ratios and Reserve Discipline

Loss ratio — claims paid as a percentage of net premium — is the most direct measure of program profitability. Reserve management matters just as much, because loss ratio alone won't reveal a future shortfall building beneath the surface.

The NAIC Model Act requires providers to maintain a funded reserve of at least 40% of gross consideration received, less claims paid, for all in-force contracts. Administrators who actively manage reserves project future claims exposure and ensure adequate funds remain in trust. Those who neglect this discipline may present healthy short-term cession statements while building a claims deficit that won't appear until contracts mature.

When Fee Structures Signal a Problem

Reserve neglect and fee opacity often appear together. Watch for these red flags:

- Net premium ceded is significantly lower than expected after reviewing gross premium

- Fees have never been clearly disclosed or itemized in writing

- LAE appears bundled with claims paid rather than as a separate line

- The program has run for multiple years without a formal performance review

- Multiple fee labels cover what appears to be the same service category

Common Misconceptions About Reinsurance Fees

"The Lowest Admin Fee Equals the Best Program"

Two programs with identical admin fees can produce materially different results based on ceding fees, claims adjudication quality, and the level of active management included. Chasing the lowest headline fee is a false economy — lower admin fees often mean slower claims processing, no proactive program management, and services the dealer ends up sourcing independently at additional cost.

"Reinsurance Is a Set-It-and-Forget-It Strategy"

Programs must be actively monitored. Products should be reviewed periodically based on loss ratio performance, and fee structures warrant renegotiation as volume grows and programs mature. Industry advisors compare annual reinsurance checkups to an annual physical — and DealerRE recommends reassessing program structure and efficiency at least every 18 months. Dealers who disengage from oversight often miss early signs of loss ratio drift or ceding fee creep until the damage is already done.

"Bundled Fees Are Simpler and Therefore Better"

When multiple cost categories are grouped into a single line item, it becomes impossible to audit whether charges are reasonable or whether you're paying for services you don't actually receive. Bundling commonly obscures:

- Admin fees rolled together with ceding fees at inflated combined rates

- Claims adjudication costs that can't be benchmarked independently

- Compliance or reporting services billed whether delivered or not

- Investment management charges buried in the overall fee structure

Simplicity and transparency are in direct tension. In reinsurance, opacity typically benefits the administrator — not the dealer.

Frequently Asked Questions

What is an F&I reinsurance program?

An F&I reinsurance program allows an auto dealer to participate in the underwriting profit from F&I products they sell — such as vehicle service contracts and GAP — by directing premiums into a dealer-owned reinsurance entity rather than surrendering that profit to a third-party insurer. Instead of paying an outside provider, the dealer retains the insurance economics on their own customer base.

What is a reinsurance fee?

A reinsurance fee is a charge charged by a program administrator for services related to operating the dealer's reinsurance company — including contract administration, claims processing, compliance, and reporting. These fees reduce the net premium that flows into the dealer's reinsurance account and directly affect underwriting profitability.

What is a ceding fee in reinsurance?

A ceding fee is the percentage of premium retained by the administrator before funds transfer to the dealer's reinsurance entity. Even small differences in ceding fee percentages compound meaningfully over time — a 3% spread on $500,000 in annual premium equals $15,000 per year that never reaches the dealer's account.

What is a typical admin fee for a vehicle service contract reinsurance program?

Admin fees vary widely by program structure and administrator. Industry sources cite ranges from under $100 to over $400 per contract, with the wide spread largely explained by what services are bundled in. The right fee depends on what the administrator delivers, not the headline number alone.

How do I know if my reinsurance program is actually profitable?

Review your quarterly cession statements and verify that net premium ceded aligns with expectations after all fees are deducted. Check that your loss ratio falls within a sustainable range — the industry standard is 40% or below in claims relative to net premium.