The cost of setting up and running a reinsurance program varies significantly based on structure type, sales volume, and administrative approach. Many dealers misunderstand these costs entirely — they focus on the annual operating fee without calculating what they currently surrender to external providers, or they choose the cheapest entry structure without evaluating loss ratio risk specific to powersports segments.

The result: dealers either overpay for programs that don't match their volume, or they walk away from a wealth-building strategy that could generate tens of thousands in recaptured profit annually.

Key Takeaways

- Annual operating costs range from $5,000–$6,000 for basic offshore structures up to $15,000+ for full-service admin obligor programs

- Retro programs have no upfront cost — but dealers permanently surrender the underwriting profit they could own

- Key cost drivers: program structure, sales volume, F&I penetration rate, and administrative support level

- The real question isn't what a program costs — it's how much profit you're leaving with a third party by not having one

How Much Does a Powersports Dealer Reinsurance Program Cost?

There's no single price tag for a dealer reinsurance program. The total investment depends on the structure type, administrative model, services included, and your dealership's specific volume and product mix.

Dealers who expect a simple quote often misunderstand what they're actually buying. You're forming a legal entity designed to capture insurance underwriting profit — a business decision with ongoing financial and compliance implications, not a recurring vendor expense.

What goes wrong when dealers misunderstand cost:

- Selecting a low-cost structure without evaluating ongoing compliance obligations or state-level filing requirements

- Underestimating annual maintenance fees — charter renewals, tax return preparation, and regulatory filings add up

- Missing hidden ceding fees charged by some administrators that erode underwriting profit each time premium flows through the entity

- Focusing on minimizing expense instead of maximizing net retained income

Before comparing programs, ask for a complete fee schedule that includes formation costs, annual operating expenses, per-claim fees, and any volume-based or ceding charges.

Three program structures define most of the powersports reinsurance market, each with a different cost profile and level of operational commitment.

Entry-Level / Retro Profit-Sharing Program

What's included: No insurance entity to form or maintain. The F&I product provider shares a percentage of unused premium with the dealer after claims are settled, typically on an 18-month lag. The dealer has zero direct cost and no downside risk.

Best for: Lower-volume powersports dealers selling fewer than 15–20 service contracts monthly who want to participate in unused reserves without administrative burden or compliance responsibility.

Retro programs offer the simplest entry point into profit participation, but distributions are taxed as ordinary income and the dealer never captures 100% of the underwriting profit — the third-party administrator retains a portion as compensation for bearing the risk.

Mid-Range / Offshore Reinsurance (CFC-Style Structure)

What's included: Formation of an offshore reinsurance entity, commonly domiciled in Turks and Caicos. Annual operating costs typically run $5,000–$6,000, covering charter renewal and tax preparation/filings. Premiums cede to the entity and grow tax-deferred under IRC Section 953(d), with potential 831(b) election if net premiums remain under $2.2 million annually.

Who it fits: Mid-volume dealers willing to absorb modest annual operating costs in exchange for growing a tax-advantaged reserve that can be reinvested or distributed at capital gains rates.

Offshore structures offer lower formation costs than domestic alternatives, but they carry ongoing compliance obligations and require disciplined financial oversight. Funds typically remain in U.S. financial institutions despite the offshore domicile.

Full-Service Admin Obligor Program

What's included: A domestically structured or hybrid reinsurance entity where the dealer participates in 100% of underwriting profit. The administrator manages claims adjudication, compliance, legal filings, tax returns, financial reporting, and F&I training. Risk is backed by an A-rated insurer via a Contractual Liability Insurance Policy (CLIP), so the dealer captures profit without bearing direct claim liability.

Best for: Dealers committed to long-term wealth accumulation who want to replace third-party F&I providers entirely and capture underwriting profit at scale, with professional oversight managing operational complexity.

Full-service programs carry higher annual costs than basic offshore structures, but they bundle compliance, training, and claims management into a single engagement. That consolidation eliminates the need to coordinate multiple vendors and reduces exposure to regulatory missteps.

Key Factors That Drive Reinsurance Program Costs

Total cost isn't just the program's sticker price. It's shaped by operational, structural, and volume-based factors that determine whether the economics work in your favor.

Program Structure and Entity Type

Your choice of structure — retro, offshore CFC, domestic DOWC, or admin obligor hybrid — directly determines both setup and ongoing costs.

- Offshore CFC formation: Approximately $5,000–$6,000 one-time, with annual operating costs of $5,000–$6,000 for charter renewal and tax filings

- NCFC formation: Approximately $25,000 one-time, with shared risk across 11+ unaffiliated shareholders

- DOWC formation: As low as $500 for administrative filing, though total capitalization requirements are higher

Some administrators also charge ceding fees — a percentage deducted from premium as it flows into the reinsurance entity. These fees cut directly into underwriting profit and can wipe out the returns you projected. Always request a complete fee breakdown before committing.

Dealer Sales Volume and F&I Penetration Rate

Volume is the primary economic lever. A dealer selling 80 units monthly with 30% service contract penetration generates a fundamentally different reserve pool than one selling 25 units monthly.

Illustrative example:

- Monthly units sold: 50

- Service contract penetration rate: 30%

- Service contracts written per month: 15

- Reserve allocated per contract: $400

- Monthly premium into reinsurance: $6,000

- Annual reserve accumulation: $72,000

At $72,000 in annual reserves and a $5,000–$6,000 operating cost, the program absorbs roughly 7–8% of reserves in administrative expense before claims. If the loss ratio runs 60%, the dealer retains approximately $22,000–$23,000 in underwriting profit after claims and costs — roughly a 4x return on the $5,000–$6,000 operating cost.

Below certain volume thresholds, the cost of operating a reinsurance entity doesn't justify the administrative burden. That's when retro programs make more sense.

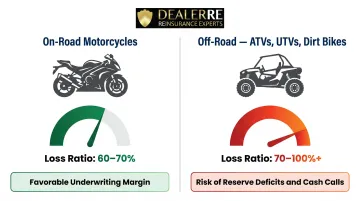

Loss Ratios by Vehicle Type and Product

Powersports loss ratios vary widely by segment. The gap between vehicle types has a direct impact on whether reinsurance generates profit or creates a cash drain:

| Segment | Typical Loss Ratio |

|---|---|

| On-road motorcycles | 60–70% |

| Off-road (ATVs, UTVs, dirt bikes) | 70–90%, sometimes exceeding 100% |

High loss ratios flip the economics of reinsurance. If claims consistently exceed premiums, the dealer may be required to deposit additional funds to cover shortfalls, turning a profit strategy into a cash drain.

Why this matters: A dealer whose product mix skews heavily toward off-road UTVs and ATVs faces materially different underwriting risk than an on-road motorcycle dealer. Before selecting a structure, model your expected loss ratios based on your actual segment mix. A full-service administrator should provide this analysis before program launch.

Level of Administrative Support

You can self-manage a reinsurance program by contracting separately for legal filings, tax returns, compliance oversight, and claims adjudication — or you can engage a full-service administrator that bundles all these functions.

Self-managed programs appear cheaper upfront but carry hidden costs:

- Legal fees for annual filings and compliance updates

- CPA fees for tax return preparation and 831(b) election management

- Time spent coordinating multiple vendors

- Risk of compliance gaps that trigger audits or penalties

Full-service administration costs more annually, but that premium buys something self-managed programs can't guarantee: a single party accountable when claims spike, a compliance deadline gets missed, or a tax filing needs to be defended. For most dealers, that risk coverage is worth more than the fee differential.

Full Cost Breakdown: What You're Actually Paying For

Most dealers underestimate total program costs because they focus on setup fees and overlook the recurring operational layer. Understanding both categories upfront is how you compare programs accurately — and avoid surprises once you're running.

Entity Formation and Setup

This is a one-time expense covering legal formation of the reinsurance entity, initial documentation, regulatory filings, and program structuring. Costs vary by structure:

- Offshore CFC: $5,000–$6,000

- NCFC: $25,000

- DOWC: $500 filing fee (total capitalization requirements are higher)

Annual Charter Renewal and Tax/Compliance Filings

This is an ongoing annual expense. It covers charter renewal, tax return preparation for the reinsurance entity, and required regulatory filings. For basic offshore structures, these costs typically run $5,000–$6,000 per year.

Full-service programs may bundle these costs differently, incorporating them into a comprehensive administration fee.

Administration, Claims Adjudication, and Reporting

The recurring administration cost covers ongoing program management:

- Processing and adjudicating claims

- Generating monthly performance reports (balance sheet, P&L, loss ratio by model/product)

- Maintaining financial records and compliance documentation

Full-service administrators like DealerRE bundle these functions into program management rather than billing them separately. When comparing providers, confirm what's included — specifically whether per-claim fees or volume-based charges apply as your program grows.

F&I Training, Menus, and Staff Development

Training is a periodic cost that dealers consistently undervalue. Some administrators bundle menu development, staff coaching, and ongoing F&I training into their service package — others bill for it separately.

What makes this line item significant is the downstream effect: F&I penetration directly determines how much premium flows into your reinsurance entity. For mid-volume dealers, a 10-point penetration increase can double annual reserve accumulation.

Retro Program vs. Admin Obligor: A Cost Comparison

Both structures let dealers participate in unused F&I premium — but the similarities end there. Cost structure, risk exposure, and profit ceiling vary significantly between the two.

| Dimension | Retro Program | Admin Obligor |

|---|---|---|

| Direct cost to dealer | $0 upfront; no ongoing fees | $5,000–$6,000+ annually for entity + administration |

| Risk exposure | None — provider covers shortfalls | Backed by A-rated insurer via CLIP; no direct dealer liability |

| Tax treatment | Distributions taxed as ordinary income | Premiums grow tax-deferred; dividends at capital gains rates |

| Long-term wealth potential | Limited — dealer receives a share, not 100% | High — dealer captures 100% of underwriting profit |

| Administrative burden | None — fully managed by provider | Managed by administrator; dealer receives reports and oversight |

Retro programs are the right starting point for smaller dealers who want to test profit participation without operational complexity. Admin obligor programs are the right long-term structure for dealers committed to capturing 100% of underwriting profit.

Every year a dealer stays in a retro program past the point of readiness is a year of underwriting profit handed to a third-party provider — profit that could have stayed in the dealer's own company.

What Most Powersports Dealers Get Wrong About Reinsurance Costs

Focusing Only on the Annual Operating Fee Without Calculating What They Give Away

Dealers who balk at a $5,000–$6,000 annual operating fee often fail to calculate what they currently surrender to third-party warranty companies.

Example: A dealer writing 20 service contracts monthly at $400 reserve per contract generates $96,000 in annual reserves. At a 60% loss ratio, $38,400 remains after claims. If the dealer participates in a retro program that shares 50% of unused premium, they receive $19,200. If they own the reinsurance entity outright, they capture the full $38,400 — a $19,200 difference.

The $5,000 operating cost is a rounding error compared to the incremental profit captured.

Choosing the Cheapest Structure Without Evaluating Loss Ratio Risk

Low-cost entry into reinsurance without understanding powersports-specific loss ratios can backfire. Dealers heavily weighted toward off-road UTVs and ATVs with 80–90% loss ratios may find themselves required to deposit additional funds to cover claim shortfalls.

What starts as a profit strategy ends with cash calls and reserve deficits — the opposite of why dealers enter reinsurance in the first place.

Underestimating the Cost of Doing It Wrong

Underperforming programs usually trace back to three root causes:

- Poor F&I penetration that leaves reserves chronically thin

- Incorrect product mix relative to actual powersports loss patterns

- No administrator oversight to catch problems before they compound

Fixing a poorly structured program — re-forming the entity, correcting tax filings, resolving compliance gaps — routinely costs more than a properly managed full-service setup would have from day one. The remediation bill is often the first real number that clarifies what the discount was actually worth.

Frequently Asked Questions

How much does reinsurance cost?

For a dealer-owned reinsurance entity, direct annual operating costs typically run $5,000–$6,000 for basic offshore structures. Full-service admin obligor programs bundle additional services like claims management, compliance, and training, which affect total cost. The key metric is net profit retained versus cost of the program.

What are the 4 types of reinsurance?

Dealers typically work within four program structures:

- Walkaway — no dealer participation in underwriting profit

- Retro/Retrospective — dealer receives a share of unused premiums at year-end

- CFC/Offshore — premiums cede to a dealer-owned offshore entity

- DOWC/Admin Obligor — domestic or hybrid entity where the dealer captures 100% of underwriting profit

What is Powersports F&I?

F&I (Finance and Insurance) in powersports covers the back-end products and financing sold alongside a vehicle purchase — extended service contracts, GAP protection, tire and wheel coverage, and maintenance plans. Reinsurance lets the dealer capture the underwriting profit on these products instead of passing it to a third-party provider.

How much does the extended service plan cost for a powersports dealer to reinsure?

On a typical $500 service contract, roughly $400 goes into reserves to pay claims over the contract's five-year life, and $100 covers administration fees, commissions, and pass-through costs. With a reinsurance program, the dealer captures whatever reserves remain after claims — rather than letting that surplus flow to a third-party administrator.

Is a reinsurance program worth it for a smaller powersports dealer?

Volume is the key threshold. Dealers below a certain monthly unit and contract count may be better served by a retro program, which requires no upfront investment and carries no downside risk. Dealers above that threshold typically find the cost of a dealer-owned reinsurance entity is offset many times over by captured underwriting profit within the first few years.

What is an admin obligor reinsurance program?

In an admin obligor structure, the risk of paying claims is held by the administrator (backed by an A-rated insurer via a CLIP policy), while the dealer still participates in 100% of the underwriting profit. This gives the dealer the economic upside of reinsurance without bearing direct claim liability, combining wealth accumulation with operational protection.

Worth noting: The cost of a powersports dealer reinsurance program is rarely the barrier dealers expect. At $5,000–$6,000 annually, a dealer-owned structure typically pays for itself many times over once you account for the underwriting profit that currently flows to third-party providers.