Introduction

F&I is already one of the most profitable departments in your dealership. According to Haig Partners, publicly traded dealer groups averaged $2,581 in F&I gross profit per vehicle retailed in Q3 2025 — approaching historic highs. But here's what that number doesn't show: the underwriting profit sitting behind every vehicle service contract and GAP policy you sell.

In a standard third-party arrangement, you earn a front-end commission. The administrator keeps the reserves, the investment income, and the underwriting surplus. Every contract you sell generates profit for someone. In a standard arrangement, that someone is your administrator, not you.

F&I reinsurance changes that. By owning your own reinsurance company, you participate in the underwriting profits on the same products you're already selling. Dealer-owned reinsurance has been regulated and functional for decades. Most dealers still haven't taken advantage of it.

This guide covers the three main reinsurance structures, how each one maximizes profitability differently, which F&I products belong in a reinsurance program, and what it takes to get started.

TL;DR

- Dealer-owned reinsurance lets you capture underwriting profits that currently flow to third-party administrators

- The three primary structures — CFC, NCFC, and DOWC — differ in control, tax treatment, and risk exposure

- VSCs and ancillary products are generally the strongest reinsurance candidates; GAP requires careful volume analysis

- Minimum viable volume is typically 20–25 service contracts per month

- A full-service administrator handles legal setup, filings, tax returns, and ongoing compliance on your behalf

What Is F&I Reinsurance and Why Most Dealers Leave Money on the Table

When you sell a vehicle service contract or GAP policy, a portion of the customer's premium is ceded to a reinsurance company. In a traditional arrangement, that company belongs to your third-party administrator. With dealer-owned reinsurance, it belongs to you.

The Profit Leakage Problem

DealerRE frames this with a simple question worth asking yourself: If your warranty company weren't making a profit off your sales, would they keep doing business with you?

That answer explains the entire standard F&I model: you earn a commission on the contract sale, while your administrator pockets the underwriting surplus — the spread between premiums collected and claims paid.

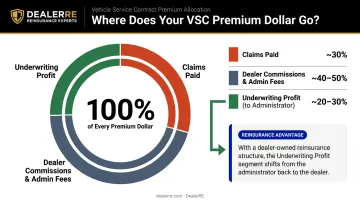

The Casualty Actuarial Society notes that VSC loss ratios at the retail premium level can be as low as 30% — meaning for every dollar a customer pays, as little as 30 cents goes toward actual claims. The remaining 70 cents covers dealer commissions, administrator fees, and underwriting profit. Reinsurance is the mechanism that puts you on the right side of that equation.

It's Not New — or Risky When Done Right

Dealer-owned reinsurance traces back to the 1950s, when Texas dealers formed domestic insurance companies to reinsure credit life and disability coverage. The model has evolved significantly since then, moving through Arizona in the 1960s and offshore in the 1980s, and it's properly regulated today.

Two points dealers often misunderstand:

- CFC structures domiciled in places like the Turks and Caicos still hold all assets in U.S. financial institutions and elect to be taxed as domestic U.S. corporations under IRC Section 953(d) — offshore location doesn't mean offshore accountability.

- Finalized micro-captive regulations from January 2025 include a Consumer Coverage Exception for Seller's Captives, a carve-out designed specifically for legitimate dealer reinsurance structures.

Confirm with qualified tax counsel that your structure qualifies under the exception before proceeding.

The Main F&I Reinsurance Structures Dealers Should Know

Reinsurance is not a single product. The right structure depends on your production volume, tax objectives, and how much control you want over claims and investments. Choosing the wrong one can cost you real profit or expose you to avoidable risk.

Controlled Foreign Corporation (CFC)

A CFC is an offshore-domiciled reinsurance company — most commonly in the Turks and Caicos Islands — that the dealer owns outright. Despite the offshore domicile, all funds are held in U.S. trust accounts. No money goes offshore.

Key advantages:

- Qualifies for the IRC Section 831(b) small insurance company election, which allows premiums up to $2.9 million in 2026 to be excluded from taxable income (the company pays tax only on investment income)

- Full dealer control over investment strategy once reserves exceed 125% of unearned premiums

- Ability to reinvest or direct accumulated funds toward personal wealth-building goals

Best suited for: Mid-to-larger volume dealerships generating substantial annual premium under the 831(b) cap. The structure carries administrative complexity and requires working with qualified tax counsel — the 831(b) election and annual 1120-PC filings require professional tax guidance.

Non-Controlled Foreign Corporation (NCFC)

An NCFC is also domiciled offshore, but ownership is spread across multiple participating dealers — no single dealer holds a controlling interest. This pooled structure lowers individual liability exposure while still building equity.

Key advantages:

- Tax-deferred growth within the entity

- Dividends are typically taxed at capital gains rates rather than ordinary income rates — a significant advantage for dealers in higher income brackets

- Lower complexity than a solo CFC for dealers not ready for full underwriting ownership

Trade-offs:

- Less investment flexibility than a solo CFC

- Subject to a 1% federal excise tax on reinsurance premiums ceded offshore (26 USC Section 4371)

- Dividends only flow when surplus is repatriated

Best suited for: Risk-averse operators, smaller dealerships entering reinsurance for the first time, or dealers who have exceeded the 831(b) premium cap and prefer capital gains treatment over full underwriting control.

Admin Obligor / Dealer-Owned Warranty Company (DOWC)

The DOWC model is domestic. The dealer owns a U.S.-based company that acts as the obligor — meaning it issues service contracts directly to customers under its own name. An A-rated insurance carrier backs the program, providing the regulatory and financial backstop that customers and lenders require.

DealerRE specializes in this structure, helping dealers establish and manage their own administrator obligor reinsurance companies to replace third-party and manufacturer F&I products.

Key advantages:

- No offshore complexity; no federal excise tax on premiums

- 100% ownership of the book of business — your company reinsures only your contracts, not a pool with other dealers

- Full control over contract terms, coverages, and pricing

- Claims handled through the program directly, keeping the customer experience in your hands

- Tax treatment as an insurance company, which can create substantial deductions — dealers should consult a tax professional for their specific situation

Best suited for: Dealers who want maximum control, domestic simplicity, and a direct connection between their F&I performance and their reinsurance profitability. Both franchise and BHPH dealers use this structure effectively.

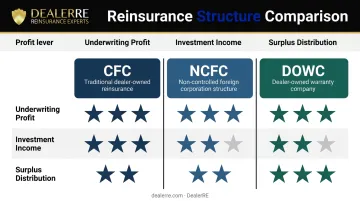

How Each Structure Maximizes Dealership Profit Differently

Every reinsurance structure accesses three core profit levers. Understanding which levers each structure pulls — and how hard — is what separates a well-designed program from a mediocre one.

The Three Profit Levers

| Lever | What It Is | Which Structures Access It Best |

|---|---|---|

| Underwriting profit | Premiums minus claims and expenses | All structures; DOWC offers most direct control |

| Investment income | Returns earned on held reserves | CFC (most flexible); DOWC (trusteed arrangement) |

| Surplus distribution | Withdrawing accumulated equity over time | CFC and DOWC (dividends/distributions); NCFC (repatriated dividends at capital gains rates) |

Claims Control as a Profit Driver

This is where the DOWC/admin obligor model has a distinct edge. When your company is the obligor, your team — or your chosen administrator — manages the claims philosophy. That philosophy directly affects both your loss ratio and your customers. When a third-party administrator handles claims, your customer's experience is out of your hands. A slow approval, a denied claim, or a poor interaction reflects on your dealership even though you had no involvement. With dealer-owned reinsurance, you control that interaction — and DealerRE clients consistently point to this as a driver of repeat and referral business.

Tax Planning as a Multiplier

The 831(b) election available to qualifying CFCs is the most powerful single tax advantage in dealer reinsurance. Premiums up to $2.9 million (2026 threshold, indexed annually) are excluded from taxable income — the company pays tax only on investment income. For dealers generating significant premium volume, this creates a tax-advantaged accumulation opportunity that ordinary business income simply cannot match.

That accumulated income can then be directed toward real estate purchases, dealership reinvestment, college funding, or other personal wealth-building goals. Dealers operating under a well-structured 831(b) program have captured six-figure underwriting profits that would otherwise have gone to third-party providers. The key is working with a tax professional who specializes in insurance company elections — few general CPAs handle this area.

Managing Loss Ratio Risk

The primary financial risk in any reinsurance program is claims exceeding reserves. The main controls are:

- Product selection — only reinsure products with favorable and predictable loss patterns

- Proper reserving — conservative initial reserves protect against adverse claim emergence

- Regular performance reviews — monthly cession statements and claims reports identify negative trends early before they compound

Dealers who treat loss ratio management as an ongoing discipline — not a one-time setup task — consistently outperform those who don't. DealerRE's full-service model builds performance reporting and claims monitoring into the program from day one, so negative trends get caught before they compound.

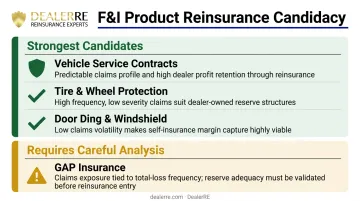

Which F&I Products Work Best in a Reinsurance Program

Not every F&I product belongs in your reinsurance company. Product selection directly determines profitability — put the wrong products in and you're absorbing risk without the return to justify it.

Strongest Candidates

Vehicle Service Contracts (VSCs) are the backbone of most dealer reinsurance portfolios. Loss patterns are actuarially predictable, with new car claims emerging slowly over a five-year contract — roughly 5% in year one, building to peak losses in years three and four. This gives reserves time to accumulate before significant claims emerge. For dealers building a reinsurance program, VSCs are consistently one of the most lucrative products to include.

Ancillary products — tire and wheel, door ding, windshield repair, paint and fabric protection — carry "extremely low" loss ratios according to Zurich and are strong wealth-building contributors. DealerRE recommends bundling these into a Multi-Shield package that boosts F&I penetration while feeding the reinsurance pool.

Products Requiring Careful Analysis

GAP insurance carries higher and more variable losses because it depends on total loss events, lender LTV ratios, and payoff timing — none of which you fully control. Many experienced operators run GAP as a "walkaway" product rather than reinsuring it, unless volume is sufficient to spread risk across a large book.

For BHPH dealers, though, GAP represents a distinct opportunity. Many BHPH operators already absorb the remaining balance after a total loss by writing it off. If you're providing that coverage informally anyway, you should be capturing the premium and the underwriting profit through your reinsurance company.

The BHPH Opportunity

DealerRE's admin obligor program for BHPH dealers is built around a practical reality: customers won't keep paying on a car that doesn't run. By selling VSCs through their reinsurance company, BHPH dealers build a customer-funded pool to cover mechanical breakdowns.

The mechanics work in the dealer's favor at every stage:

- Repair costs come out of the pool, not the dealer's operating account

- Premiums are financed over the contract term and billed monthly as payments come in

- Contracts that expire without claims leave surplus in the dealer's reinsurance company

Is Your Dealership Ready? Key Factors to Evaluate

Production Volume

Reinsurance becomes financially viable once you're selling a consistent volume of service contracts — industry practitioners generally cite 20 to 25 contracts per month as the practical threshold. Below that level, premium income won't cover administration fees and claims.

DealerRE works with dealers selling more than 30 vehicles per month as a general starting point, though the actual viability analysis looks at F&I penetration rates, product mix, and average contract values — not just unit volume.

Dealers not yet at that threshold still have options:

- Retroactive profit-sharing programs require no entity formation and no underwriting risk

- Profits are taxed as ordinary income and no equity accumulates — but it's a practical starting point

- These programs can serve as a bridge while volume grows toward reinsurance viability

What the Setup Process Actually Involves

Once you've confirmed the volume and structure fit, getting started is more straightforward than most dealers expect — especially with a full-service administrator:

- F&I and tax analysis — review product mix, volume, penetration rates, and your tax situation to identify the right structure

- Tax structure selection — CFC, NCFC, or DOWC based on volume, tax goals, and how much control you want

- Entity formation — legal entity creation, domicile filings, tax elections (including 831(b) if applicable), and trust account setup

- Staff training — onboarding your F&I team on product presentation, program mechanics, and performance expectations

- Program launch — claims adjudication, monthly reporting, and ongoing compliance management begin

DealerRE manages all legal forms, filings, tax returns, and renewals on behalf of clients — with no hidden additional fees. The goal is a turnkey setup where the administrative burden stays with the administrator, not the dealer.

What Ongoing Support Should Look Like

A reinsurance program is not a "set it and forget it" structure. The right administrator provides:

- Monthly financial statements and cession reports

- Claims adjudication and loss monitoring

- Annual tax return preparation (1120-PC for insurance companies)

- License renewal and regulatory compliance

- F&I training — both online and in person — to sustain penetration rates

- Periodic program reviews to adjust reserving, product mix, and investment direction

DealerRE has served over 400 dealers nationwide since 1994. Several clients have gone on to earn National Quality Dealer of the Year recognition and hold NIADA board positions — results that come from consistent program management, not just the reinsurance structure itself.

Frequently Asked Questions

What are F&I products in insurance?

F&I (Finance and Insurance) products are protection products sold in the dealership's finance office — including vehicle service contracts, GAP coverage, tire and wheel protection, and appearance products. They protect the customer's vehicle investment while generating back-end income for the dealership.

What is the difference between a CFC and a DOWC reinsurance structure?

A CFC is an offshore-domiciled reinsurance company that offers 831(b) tax potential and investment flexibility. A DOWC is a dealer-owned domestic warranty company backed by an A-rated carrier, offering stronger claims control without offshore complexity. CFCs tend to favor dealers at higher volume levels where the tax treatment makes a meaningful difference.

Can independent or BHPH dealers participate in F&I reinsurance?

Yes. Both dealer types can participate, and BHPH dealers in particular benefit from admin obligor programs that build a customer-funded pool for mechanical breakdown coverage — turning a traditional dealer expense into a profit center.

How do dealers access profits from their reinsurance company?

It depends on the structure. Trust arrangements allow withdrawals above required reserves with underwriting approval. CFC and DOWC programs permit distributions and, in some cases, loans against the account. Tax implications vary, so consult a qualified tax advisor for your specific situation.

What F&I products work best in a dealer-owned reinsurance program?

VSCs and ancillary products (tire and wheel, door ding, windshield) are typically the strongest candidates due to predictable loss ratios and low claims frequency. GAP requires sufficient volume to spread risk before inclusion makes sense.

How long does it take to set up a dealership reinsurance company?

Timelines vary by structure and domicile. Working with a full-service administrator that manages legal forms, filings, and compliance reduces setup time considerably. The more important factor is choosing a partner equipped to run the program long-term, not just complete the initial paperwork.