That third party did none of the selling. They have none of the customer relationship. They just collect the underwriting profit — the surplus left after claims are paid — while the dealer moves on to the next deal.

F&I reinsurance changes that equation entirely. It's one of the most overlooked income opportunities in independent automotive retail, and it's been accessible to dealers of all sizes for over 30 years.

This article covers what dealer-owned reinsurance actually is, how the profit mechanics work, why independent and BHPH dealers have the most to gain, and what to look for in a reinsurance partner.

TL;DR

- Traditional third-party F&I arrangements send underwriting profits to the provider, not back to your dealership

- Dealer-owned reinsurance captures those profits, plus investment income on held reserves

- Independent dealers, including BHPH stores, are particularly well-positioned to benefit

- Admin obligor structures give dealers direct profit participation, backed by A-rated carriers

- Volume doesn't need to be massive — dealers selling 30+ units per month are often viable candidates

F&I and Reinsurance 101: What Every Independent Dealer Should Know

The F&I Department

F&I — Finance and Insurance — is the dealership department that helps customers arrange financing and purchase protection products. Common products include:

- Vehicle service contracts (VSCs)

- GAP insurance

- Tire and wheel coverage

- Collateral protection insurance (CPI)

- Debt cancellation coverage (DCC)

- Ancillary products like windshield repair, door ding protection, and theft deterrent packages

For most dealerships, F&I is consistently the highest-margin department. NADA Show data from StoneEagle showed F&I per-vehicle retailed (PVR) rose 14% across 2025, and public dealer groups were averaging around $2,505 PVR in Q1 2025 according to Haig Partners.

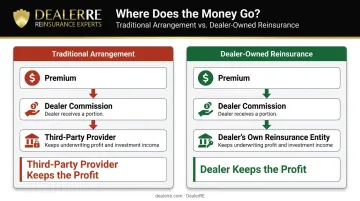

The Traditional Arrangement (and Its Problem)

When dealers sell F&I products through third-party providers, the typical structure looks like this:

- The dealer earns a commission or dealer participation fee

- The provider retains the underwriting profit — the surplus remaining after claims are paid

- The provider also earns investment income on the reserves held between premium collection and claim payment

The dealer does all the work of building customer trust and presenting products. The provider keeps the most valuable part of the income.

What Dealer-Owned Reinsurance Changes

That profit doesn't have to leave the dealership. Dealer-owned reinsurance is the financial structure that flips this arrangement — the dealer establishes their own reinsurance entity to assume the underwriting risk and capture the profits that would otherwise flow to outside providers.

The concept dates to the 1970s, with dealer-owned credit life and disability reinsurers among the earliest examples. It's a well-tested strategy with decades of documented results behind it.

How F&I Reinsurance Works: The Profit Mechanics

Premium Flow Step by Step

When a customer purchases an F&I product, the premium is collected and allocated across several line items:

- Dealer commission — the front-end income the dealer earns immediately

- Administration fees — charged by the program administrator for managing the contract

- Net premium/reserves — the remaining amount ceded to the dealer's reinsurance company to fund future claims

In a dealer-owned structure, those reserves don't go to a third-party insurer. They go into the dealer's own reinsurance entity, held in a U.S.-based trust account.

Claims and Underwriting Profit

Claims are paid from the reserves held in the dealer's reinsurance company. Because the dealer owns that entity, claims are adjudicated on behalf of that dealer's own customers — not pooled across an unknown book of business.

Underwriting profit is what remains when total premiums collected exceed total claims paid over the contract term. Where that surplus goes depends entirely on the program structure:

- Traditional arrangement — surplus belongs to the third-party provider

- Dealer-owned reinsurance — surplus belongs to the dealer

Investment Income: The Second Profit Layer

From the time premiums are collected to the time claims are paid, those reserve funds are invested. That investment income belongs to the dealer's reinsurance company.

DealerRE holds all reserve funds in U.S.-based trust accounts and invests conservatively — typically in government bonds. Once accumulated reserves exceed 125% of unearned premiums, the dealer can redirect those excess funds into other priorities — real estate, dealership reinvestment, or other assets chosen by ownership.

That flexibility is made possible by the structure itself — specifically, how DealerRE sets up the dealer's reinsurance company as the named obligor on customer contracts.

The Admin Obligor Structure

In DealerRE's admin obligor structure, the dealer's reinsurance company is the named obligor on customer contracts. An A-rated insurance carrier provides the financial backing, meaning:

- The dealer captures underwriting profits and investment income

- The program maintains regulatory soundness and financial credibility

- If the dealer's reinsurance company cannot meet obligations, the A-rated carrier backstops the liability

For independent dealers, this means meaningful profit participation without taking on uncapped financial exposure. The A-rated carrier handles the downside; the dealer keeps the upside.

Why Independent Dealers Are Leaving the Most Profit Behind

The Margin Reality

Independent dealers typically operate with narrower front-end margins than franchise counterparts. That makes F&I income more critical to overall dealership profitability. Yet independents are often the group most reliant on third-party product providers, sending underwriting profits out the door on every deal.

Historical data from Colonnade Advisors shows VSC attach rates at independent dealers were approximately 30% compared to 50% at franchise dealers — meaning fewer products sold and less reinsurance profit being captured.

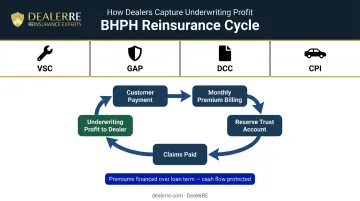

The BHPH Opportunity

Buy Here Pay Here dealers have a particularly compelling case for reinsurance. Their customers frequently purchase protection products, and those premiums create a consistent, predictable volume:

- Vehicle Service Contracts (VSCs)

- Guaranteed Asset Protection (GAP)

- Debt Cancellation Coverage (DCC)

- Collateral Protection Insurance (CPI)

BHPH dealers also know their inventory better than any third-party insurer ever will. They've assessed the mechanical profile of each vehicle before it hits the lot. Reinsuring VSCs and mechanical breakdown coverage on those cars means controlling claims on vehicles they've already evaluated — not subsidizing losses for an unknown pool at someone else's company.

With DealerRE's BHPH programs, VSC premiums are financed over the loan term and billed monthly as customer payments come in, protecting cash flow while the dealer captures full underwriting profit at contract conclusion.

The Misconception About Volume

Many independent dealers assume reinsurance is only viable for large dealer groups. It isn't. DealerRE works with independents nationwide, and dealers moving 30+ units per month are frequently solid candidates. Most reinsurance providers have overlooked smaller dealers in favor of high-volume franchise stores — which means the opportunity for independents who do engage is often larger, not smaller.

The Compounding Cost of Doing Nothing

That accessible entry point makes timing a real factor. Every year without a reinsurance program is another year of underwriting profits and investment income accumulating for a third-party provider instead of the dealer's own balance sheet. One DealerRE client put it plainly: "I wish I had done this when I first started out." Those prior years of lost surplus don't come back.

The Real Benefits of F&I Reinsurance for Independent Dealers

Profit Recapture

The primary benefit is straightforward: the dealer captures 100% of the underwriting profits on F&I products they're already selling. Those profits no longer disappear into a provider's balance sheet.

DealerRE's certified pre-owned reinsurance clients have realized hundreds of thousands of dollars in underwriting profit they didn't know was available. The profit pool exists whether or not the dealer participates — the only question is who keeps it.

Customer Experience Control

When the dealer's own reinsurance entity handles claims adjudication, the claims process reflects on the dealership — not on a faceless third party. DealerRE's administrator, AVP (Assured Vehicle Protection), adjudicates claims with the dealer's retention goals in mind — not a third-party provider's loss ratios.

For independent dealers whose repeat and referral business depends heavily on post-sale experience, this matters. A customer whose claim is handled well comes back. A customer who feels like they were denied unfairly doesn't.

Tax Efficiency and Wealth Building

Profits accumulate within the reinsurance entity in a tax-advantaged manner. DealerRE structures programs under IRS Code 831(b), which allows qualifying small non-life insurers to be taxed only on investment income — with the premium limit set at $2.9 million for 2026 per current IRS guidance.

Accumulated profits can be deployed in multiple directions:

- Real estate purchases

- Dealership facility or inventory reinvestment

- Education funding for family

- Retirement planning

- Other personal assets

For a dealer writing $2.9 million in annual premiums, that's a substantial pool of capital compounding inside a structure they own and control.

Income Diversification

Beyond the tax advantages, reinsurance income adds a second layer of financial stability that retail sales alone can't provide. Profits derive from reserves development and investment returns that build over time — not from last month's unit count. During slower retail periods, which independent dealers feel more acutely than franchise stores, the reinsurance entity keeps accumulating value. When the showroom slows down, the reinsurance account doesn't.

Choosing the Right Reinsurance Structure

The main structural options available to dealers each carry different implications:

| Structure | Obligor | Key Characteristics |

|---|---|---|

| Admin Obligor | Administrator | Lower barrier to entry; dealer participates in profits via reinsurance; A-rated carrier provides backing |

| CFC (Controlled Foreign Corporation) | Dealer-affiliated reinsurer | Offshore domicile with U.S. trust custody; 953(d) election treats as domestic; 831(b) eligible within limits |

| DOWC (Dealer-Owned Warranty Company) | Dealer-owned entity | Onshore; maximum control; higher capitalization required |

| Retro Profit-Sharing | Administrator/carrier | Simplest structure; no equity building; 24–36 month surplus lookback |

For most independent dealers, the admin obligor structure is the practical starting point. The dealer's reinsurance company is the obligor on customer contracts — creating a direct brand association — while being backed by A-rated insurers. Compliance filings, licensing, and contract approvals are managed through the administrator, reducing the regulatory burden on the dealer.

Domicile selection is part of that structural decision. DealerRE recommends the Turks and Caicos Islands — a jurisdiction with minimal capital requirements and well-defined reinsurance formation regulations. All funds remain in U.S.-based trust accounts; nothing moves offshore.

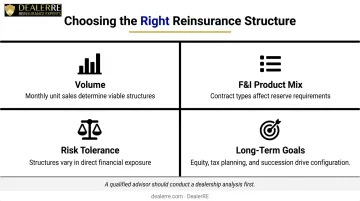

No structure fits every dealer. The right choice depends on several factors:

- Volume: Monthly unit sales determine which structures are financially viable

- F&I product mix: Current contract types affect reinsurance reserve requirements

- Risk tolerance: Some structures carry more direct financial exposure than others

- Long-term goals: Equity building, tax planning, and succession planning each point toward different configurations

A qualified reinsurance advisor should conduct a dealership analysis before any recommendation is made.

What to Look for in a Reinsurance Partner

Essential Criteria

A reinsurance partner worth working with should offer:

- Full-service administration — claims adjudication, compliance management, tax filings and renewals, monthly performance reporting, and staff training all included

- Transparent fees — no hidden costs buried in the program structure

- Genuine alignment — the advisor's success should depend on the dealer's success, not on program volume or provider revenue

Red Flags to Avoid

Watch for these warning signs when evaluating partners:

- Recommending every product into reinsurance regardless of individual risk profiles

- No regular performance analysis or financial reporting

- Programs where the dealer lacks visibility into their own account

- Structures that don't comply with IRS 831(b) requirements or proper state licensing — creating audit exposure

DealerRE publishes an "Audit Issues to Avoid" resource covering the specific compliance and tax structure pitfalls that put dealer programs at risk.

Why DealerRE

DealerRE has been serving independent dealers since 1994 — founded by Tim Byrd in Southeast Virginia and now supporting 400+ dealers nationwide. The criteria above aren't abstract ideals; they describe how DealerRE operates. A few points worth knowing:

- NIADA member and sponsor since the company's early years

- Clients have been named National Quality Dealer of the Year and served on NIADA's board

- 5-star rated across 36 client reviews

The admin obligor structure DealerRE uses is insured by A-rated carriers, with all legal filings, compliance, training, and financials handled in-house. Dealers capture the profits without absorbing the administrative burden. Taylor Byrd, DealerRE's President and a regular speaker at NIADA events, is known for making reinsurance concepts practical for dealers encountering them for the first time.

The company operates on one clear principle: "We Only Succeed If You Do."

Frequently Asked Questions

What does F&I mean in car sales?

F&I stands for Finance and Insurance — the dealership department that assists customers with vehicle financing arrangements and offers protection products such as vehicle service contracts, GAP coverage, tire and wheel protection, and ancillary coverages. It's typically the highest-margin department in a dealership.

What is an independent auto dealer?

An independent auto dealer is a dealership that operates without a franchise agreement with a vehicle manufacturer, typically selling used vehicles. This includes BHPH dealers, used car lots, and retail independent stores — a segment representing roughly 47% of used vehicle sales nationally according to NIADA data.

What is dealer-owned reinsurance and how does it work?

Dealer-owned reinsurance is a financial structure where the dealer forms their own reinsurance entity to capture underwriting profits on F&I products they sell. Premiums build reserves in a U.S.-based trust account, claims are paid from those reserves, and the surplus belongs to the dealer's company rather than a third-party provider.

How much sales volume does an independent dealer need to start a reinsurance program?

Volume requirements vary by structure and provider, but dealers selling 30+ units monthly are generally viable candidates. DealerRE specifically works with independent dealers who have been overlooked by providers focused on high-volume stores. A personalized analysis is the best way to evaluate fit.

What are the tax advantages of dealer-owned reinsurance?

Profits accumulate within the reinsurance entity in a tax-advantaged manner under IRS Code 831(b), which allows qualifying small insurers to be taxed only on investment income up to the premium limit. Program domicile and structure choices further influence tax treatment. Consult a qualified reinsurance advisor and tax counsel for specifics.

How do independent dealers get started with an F&I reinsurance program?

The first step is a dealership analysis with a qualified reinsurance advisor to evaluate your current F&I product mix and volume. From there, the appropriate structure is selected, the reinsurance entity is established, and staff training begins. With DealerRE as your partner, compliance, administration, and ongoing performance reporting are handled from setup through daily operations.