Introduction

Most dealers send underwriting profits to third-party warranty and insurance companies every month. Those profits could stay in your dealership instead. Every F&I product sold generates reserve premiums that someone captures. The question is whether that someone is a third-party administrator or your own reinsurance company.

Choosing the wrong dealer reinsurance company can lock you into a structure that limits profit, flexibility, and control. The right partner transforms F&I into a self-sustaining profit center that also improves the customer experience. According to Haig Partners, F&I gross profit reached $2,501 per vehicle retailed in Q4 2024 — and F&I PVR rose 14% across 2025. With front-end margins tightening, the reinsurance decision has real financial consequences.

Key Takeaways

- Dealer reinsurance captures underwriting profit currently kept by third-party warranty companies

- Program structure (CFC, DOWC, or admin obligor) affects tax treatment, control, and long-term profitability

- Evaluate fee transparency, compliance support, investment flexibility, F&I training, and provider track record

- Red flags include undisclosed fees, refusal to meet advisors, and lack of onboarding support

- A full-service partner handles setup, filings, claims, and training so you stay focused on running your dealership

What is a Dealer Reinsurance Company?

Dealer reinsurance is a structure where the dealer owns or participates in a reinsurance company that captures reserve premiums from F&I products — vehicle service contracts, GAP, collateral protection, and ancillary coverage — instead of letting a third-party provider keep those profits.

How the premium flow works:

- Customer purchases an F&I product

- Dealership retains a front-end commission

- Remaining premium goes to the administrator or fronting carrier

- After admin fees are deducted, net premium is ceded to the dealer's reinsurance company

- The captive holds funds in reserve to pay future claims

- After the contract period, remaining funds (underwriting profit) plus investment income belong to the dealer

In a traditional setup, the dealer earns a flat commission while the contract administrator keeps the underwriting profit and investment income. Reinsurance changes that equation: the dealer's company assumes the risk and retains the profits that would otherwise flow to third parties.

Types of Reinsurance Structures

The three main structure types differ meaningfully in tax treatment, dealer control, and capital access — and choosing the wrong one has real financial consequences:

Controlled Foreign Corporation (CFC)

An offshore corporation (commonly domiciled in Turks and Caicos or Bermuda) owned by the dealer that reinsures F&I contracts. The primary advantage is the IRC Section 831(b) election, which allows small insurance companies to be taxed only on investment income — underwriting profit is excluded from taxable income. For 2026, the IRS set the annual net written premium threshold at $2,900,000, adjusted annually in $50,000 increments for inflation. CFCs require Form 5471 filing and are subject to Subpart F income rules.

Dealer-Owned Warranty Company (DOWC)

A domestic (U.S.-based) C-Corporation where the dealer's company is the obligor — the entity legally responsible for the warranty or service contract. DOWCs pay standard corporate tax rates on profits but can deduct reserves for future claims. They offer greater front-end cash flow access than offshore CFCs and avoid certain insurance-specific regulations.

Admin Obligor

The dealer's reinsurance company is listed as the obligor on F&I contracts, making the dealer contractually responsible for fulfilling coverage. The program is backed by an A-rated fronting insurer that underwrites the risk, combining dealer control with insurer-backed security. Fronting carriers typically retain 5–15% of premium for regulatory compliance and claims infrastructure.

| Structure | Tax Treatment | Cash Flow Access | Best For |

|---|---|---|---|

| CFC (Offshore) | 831(b): taxed on investment income only | Deferred (offshore) | High-volume dealers seeking maximum tax advantage |

| DOWC (Domestic) | Standard corporate rates; reserve deductions allowed | Greater front-end access | Dealers prioritizing domestic simplicity |

| Admin Obligor | Varies by setup; insurer-backed compliance | Flexible | Dealers wanting control with A-rated insurer backing |

Benefits of Owning a Dealer Reinsurance Company

- Recapture underwriting profits currently going to third parties

- Tax-advantaged income treatment under IRC 831(b) for eligible companies

- Control over claims decisions and customer experience

- Wealth-building through investable reserves that compound over time

- Supports succession planning and employee retention strategies

With service contract penetration averaging 47% nationally but reaching 84% at top-performing dealerships, the gap between average and elite F&I performance represents real underwriting income — income that either flows into a dealer's reinsurance company or straight to a third party.

Key Factors to Consider When Choosing a Dealer Reinsurance Company

Not all reinsurance companies offer the same level of program design, support, or transparency. The right partner should align with your F&I production volume, tax situation, business goals, and tolerance for administrative involvement.

Program Structure Fit

Matching the right program structure to your dealership's situation matters because F&I production volume, ownership structure, and long-term financial goals all affect which structure performs best.

The $2.9 million annual net premium threshold for IRC 831(b) elections is a critical benchmark. Dealers approaching this cap should model whether a DOWC or hybrid structure better serves their volume trajectory. A good reinsurance company should analyze your current business before recommending a structure — not push a one-size-fits-all solution.

Factors that influence structure choice:

- Annual F&I production volume and premium flow

- Current tax situation and long-term wealth-building strategy

- Desired level of cash flow access versus tax deferral

- Tolerance for offshore regulatory complexity

- Growth trajectory and volume projections

Fee Transparency and Total Cost

Admin fees are just the starting point. Dealers must ask about all layers of cost to understand actual net profit.

Fee categories to evaluate:

- Ceding fees — retained by the administrator before funds move to your entity (often 6–10%)

- Claims administration fees — percentage charged against the net claim amount

- Loss adjustment fees — per-claim charges assessed at settlement

- Run-off fees — costs incurred when contracts wind down

- Annual maintenance fees — ongoing operational charges

- Non-disclosed fees — hidden charges that erode returns without disclosure

According to a CBT News analysis, hidden fees can consume 22% of deposits before any claims are paid. For a dealer writing 100 contracts per month, this can total $264,000 annually.

The best reinsurance companies operate on a single all-in fee model with no hidden charges, making it easier to project actual net profit. Two programs with identical admin fees can produce dramatically different financial outcomes depending on ceding fees, loss ratios, and claims handling.

Tax Treatment and Compliance Infrastructure

CFCs that make the 831(b) election are taxed only on investment income. However, CFC income is subject to Subpart F rules — underwriting income is generally taxed currently to U.S. shareholders as a deemed dividend even if not distributed. CFCs require Form 5471 filing.

DOWCs are domestic C-Corporations taxed at standard corporate rates on profits. They can deduct reserves for future claims, which creates a timing advantage — but not the outright exclusion of underwriting income that 831(b) offers.

Beyond the CFC versus DOWC distinction, recent IRS rule changes add another layer of compliance your provider must be equipped to handle.

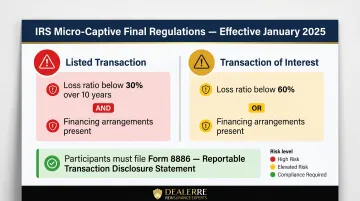

IRS micro-captive final regulations effective January 2025 classify captive arrangements as "listed transactions" when loss ratios fall below 30% over 10 years AND financing arrangements exist, or as "transactions of interest" when loss ratios fall below 60% OR financing is present. Participants must file Form 8886 (Reportable Transaction Disclosure Statement).

The reinsurance company should handle all legal filings, tax returns, renewals, and compliance requirements — and should be willing to work alongside your CPA and legal advisors. Refusal to do so is a red flag.

Investment Control and Capital Flexibility

Unearned Premium Reserve (UPR) funds are restricted in how they can be invested. These reserves are typically held in conservative government bonds or qualifying instruments that meet regulatory guidelines. UPR funds cover covered repair claims, limited professional fees, income taxes, and excess fund withdrawals above required reserves (with approval).

Once the balance sheet cash exceeds 125% of unearned premiums, surplus or "earned" funds can often be invested in higher-yield instruments at the discretion of company ownership.

Ask any provider:

- How they manage both UPR and surplus accounts

- What investment options are available for each

- Whether you can borrow against unearned premiums or surplus funds, and under what conditions

Loan flexibility is a critical operational advantage that varies significantly by provider and structure.

F&I Training and Staff Support

A reinsurance program only performs as well as the F&I products sold to support it. StoneEagle data shows a nearly 2x gap between national average service contract penetration (47%) and top-performing dealerships (84%). This performance gap represents the exact underwriting income that flows into or bypasses your reinsurance company.

A strong reinsurance partner should provide:

- F&I menu training and product sales coaching

- Onboarding for dealership staff

- Ongoing support to ensure adequate premium volume

- Data review protocols (weekly or daily) used by top performers

Providers who only set up the company and disappear leave dealers with a structurally sound program that underperforms because the front-end sales process isn't optimized.

Provider Track Record and Industry Credibility

Past performance is the most reliable predictor of how a provider will manage your program long-term. Before committing, ask direct questions — and push for specifics.

Questions to ask:

- How many dealers have you successfully set up?

- How long have you been operating?

- Are any of your clients NIADA National Quality Dealer recipients or state association award winners?

- Are you a member of NIADA or relevant state dealer associations?

- Can you provide references from dealers with similar profiles (same dealer type and volume)?

A provider who declines to offer references from comparable dealers is telling you something. Responsive account management after setup matters just as much as the quality of initial program design.

Red Flags to Watch for When Evaluating Reinsurance Providers

Not every reinsurance provider operates with your best interests in mind. These warning signs should give you pause before signing anything.

Hidden or layered fees: A provider that won't disclose all fees upfront — or buries costs in a complex structure without clear explanation — is a problem. Your net profit depends on knowing the full cost picture before you commit.

Resistance to advisor review: Walk away from any provider that won't sit down with your CPA, attorney, or wealth manager. Legitimate reinsurance companies welcome advisor involvement — proper tax and legal planning is fundamental to getting the most out of the program.

Product loading without analysis: Recommending every available product before running a risk and profitability analysis is a shortcut that benefits the provider, not you. Product selection should be built around your specific portfolio.

Vague exit provisions: Before signing, ask exactly what happens to your trust if you sell the dealership, retire, or drop below a volume threshold. Programs that void profit sharing under those conditions can cost you significantly in the long run.

How DealerRE Can Help

DealerRE is a full-service admin obligor reinsurance partner founded in 1994, with over 28 years of experience helping more than 400 auto dealers (franchise, retail, independent, and BHPH) build and manage profitable reinsurance programs. The admin obligor structure means your reinsurance company is backed by A-rated insurers, pairing security with profitability.

Comprehensive service model:

- Handle company setup, all legal filings, tax returns, and renewals

- Provide F&I training (online and in-person), F&I menus, and staff onboarding

- Manage claims adjudication through Assured Vehicle Protection (AVP)

- Deliver monthly performance reports and annual financial statements

- Offer bookkeeping and compliance management — all with no hidden fees and a single transparent cost structure

The DealerRE team includes members with direct dealership F&I experience, giving them practical insight that desk-only consultants lack. The mission is straightforward: DealerRE only succeeds when you do, making this a true partnership rather than a vendor transaction.

As a NIADA member and sponsor, DealerRE serves dealers nationwide. Their client roster speaks for itself:

- National Quality Dealer of the Year recipients

- State Quality Dealer of the Year recipients

- NIADA Board Members, State Presidents, and State Board Members

Contact DealerRE to schedule a no-cost business analysis and get a clear picture of how much underwriting profit your dealership could be retaining.

Frequently Asked Questions

What is the difference between a CFC and a dealer-owned warranty company (DOWC)?

A CFC is a foreign-domiciled corporation taxed only on investment income under IRC 831(b) from year one. A DOWC is a U.S.-domiciled entity that may defer taxes for several years but eventually faces regular corporate taxation or must make an 831(b) election. Cost, tax treatment, and flexibility differ meaningfully between the two — consult your CPA before choosing.

How much annual premium volume do I need to make dealer reinsurance worthwhile?

Under IRC 831(b), small P&C companies with less than $2.9 million in annual net premiums are taxed only on investment income. Dealers averaging 15–20 F&I products per month can generate meaningful underwriting profit — the exact break-even depends on your cost structure and program design.

What is an admin obligor reinsurance structure?

In an admin obligor structure, the dealer's reinsurance company is listed as the obligor on F&I contracts, meaning the dealer is contractually responsible for fulfilling coverage. The program is backed by an A-rated fronting insurer that underwrites the risk, combining dealer control with insurer-backed security.

Can small or independent dealers benefit from a dealer reinsurance program?

Reinsurance is not exclusively for large franchise groups. Independent, used car, and BHPH dealers can participate and benefit, particularly once they hit a minimum F&I production level. Even modest monthly volume can generate significant compounding underwriting profit — most dealers underestimate this.

How long does it take to set up a dealer reinsurance company?

A full-service provider can typically complete company formation, legal filings, and initial onboarding within a few weeks. Timelines vary by structure and provider — ask for a written milestone plan before committing.

What questions should I ask a reinsurance company before agreeing to work with them?

Key questions to ask any prospective provider:

- What fees apply beyond the admin fee?

- Will you meet with my CPA and attorney?

- Who handles compliance, tax filings, and renewals?

- What F&I training and ongoing support is included?

- What happens to the trust if I sell or retire?