Introduction

Every dealership sells Vehicle Service Contracts (VSCs), but most dealer principals don't realize the provider they choose determines how much F&I profit the dealership actually keeps. According to StoneEagle data, national VSC penetration hovers around 47% — but the real gap isn't about selling more contracts.

It's about the financial structure behind them. With F&I profit per vehicle reaching a record $2,612 in Q4 2024, every percentage point of VSC profit retained directly impacts your bottom line.

Too many dealers default to a third-party VSC administrator without evaluating whether they're leaving substantial money on the table. This guide walks through exactly what to look for — from insurer backing and claims handling to profit structure — and explains why the arrangement you choose today shapes your F&I profitability long-term.

Key Takeaways

- A VSC provider administers and underwrites the service contract your F&I office sells — not all provider structures deliver equal profitability

- Provider structures range from third-party reseller (lowest profit) to profit sharing/reinsurance to dealer-owned admin obligor reinsurance (100% profit capture)

- Evaluate providers on insurer backing (A-rated minimum), claims fairness, profit structure, and F&I training support

- The wrong provider costs you customer trust, F&I gross, and thousands in underwriting profit handed to a third party

What Is a VSC Provider, and Why Does Your Choice Matter?

A VSC provider is the company that administers, underwrites, and pays claims on the service contracts your F&I office presents to customers. This is distinct from both the manufacturer warranty and the dealership itself. The provider handles financial backing, claims processing, and customer service after the sale. Customers, however, associate every part of that experience — good or bad — with your dealership, not the administrator behind the contract.

The VSC Ecosystem: Three Key Roles

Every VSC involves three distinct participants:

- The Insurer — Provides financial backing and guarantees payment on approved claims

- The Administrator — Processes claims, manages contracts, and handles day-to-day operations

- The Seller — Your dealership, which presents the VSC to customers in F&I

In traditional arrangements, the dealer simply sells the contract and earns a markup. But in dealer-owned reinsurance structures, the dealer takes on a role in the profit layer, not just the selling layer. That distinction turns VSCs from a one-time commission line into a recurring revenue stream with compounding financial upside.

Why Your Provider Choice Impacts Reputation

A poorly backed VSC provider that denies claims or pays slowly creates customer complaints that land directly on your dealership's reputation, even though you had no part in adjudicating those claims. When a customer's transmission repair gets delayed for weeks or denied entirely, they don't blame the administrator they've never heard of. They blame your dealership.

Regulators have taken direct action against providers operating outside the law:

- In 2024, the FTC sued American Vehicle Protection for illegal telemarketing and false coverage claims, resulting in $449,000 in consumer refunds and a permanent industry ban

- California regulators ordered Elite Integrity LLC to stop selling new contracts after finding the company operated without proper licensing

These cases aren't outliers. The VSC space attracts undercapitalized and unscrupulous operators, and your dealership's name is on the contract. Vetting your provider's financial backing, licensing status, and claims track record isn't optional — it's the first line of defense for your reputation and legal standing.

The Main Types of VSC Provider Arrangements for Dealerships

The provider structure you choose directly determines how much of each VSC premium your dealership retains — and this is where most dealers underestimate their options. The three main arrangements range from standard reselling (lowest dealer profit) to full reinsurance ownership (highest dealer profit).

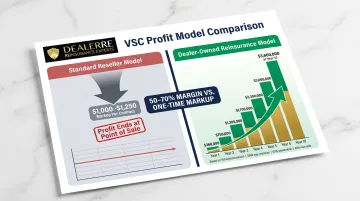

Third-Party Administrator (Standard Reseller Model)

In this model, you sell the VSC, earn a markup on the retail price, and the administrator collects the reserve and keeps all underwriting profit.

This is the most common arrangement. Typical VSC commissions range from 40-50% of the selling price — for example, $1,000 to $1,250 gross on a $2,500 contract. The administrator takes the remaining premium, holds reserves for claims, and retains any profit from lower-than-expected claims.

Key limitation: You earn once, at the point of sale. If claims run light, the administrator keeps the surplus — you have no control over claims handling and no ongoing profit participation.

Reinsurance / Profit Participation

In this arrangement, the administrator shares a portion of the claims reserve back with the dealer at year-end if claims come in below projections.

This beats standard reselling because you participate in underwriting profits. But you still don't control the underwriting entity. The administrator determines when and how much profit gets returned, and dealers have limited visibility into reserve management or claims decisions.

Dealer-Owned Admin Obligor Reinsurance

In this structure, the dealer establishes their own reinsurance company — insured by an A-rated carrier — that sits in the profit layer of every VSC sold.

Instead of sharing profit with a third party, the dealer captures 100% of the underwriting profit, including premium reserves that can be invested. Dealer-owned plans can generate 50-70% margin, higher than standard reseller arrangements.

DealerRE specializes in this structure. Since 1994, the company has helped more than 400 dealerships nationwide set up and manage dealer-owned admin obligor reinsurance companies. DealerRE's full-service administration covers:

- Company formation and legal filings

- Tax returns, compliance, and renewals

- Claims adjudication and reserve management

- Financial reporting and bookkeeping

Dealers get the profitability of owning the underwriting entity without building the infrastructure themselves.

Long-term wealth example: A dealership selling 100 vehicles per month with $500 average F&I premium and 65% penetration generates $600,000 annually in premium. With a 40% loss ratio, approximately $360,000 per year is retained as profit. Over 10 years, that's roughly $3.6 million in retained profit — compared to a single markup collected at point of sale.

The dealer-owned warranty company (DOWC) structure has been in the marketplace since the 1970s, giving it more than four decades of industry use. It's also the only domestic model that achieves results comparable to offshore Controlled Foreign Corporations (CFCs), without requiring a third-party insurer in the profit layer.

Key Factors to Consider When Choosing a VSC Provider

These five factors determine whether a VSC provider will protect your dealership's reputation, keep customers satisfied, and deliver the F&I performance your operation needs.

Insurer Financial Strength and Backing

The insurer behind the contract matters because if the administrator becomes insolvent, your dealership faces customer calls about unpaid claims. Confirm the backing insurer holds at minimum an A- rating from A.M. Best and that the program is fully insured, not just bonded.

A.M. Best's rating scale indicates an A- or A (Excellent) insurer has an excellent ability to meet ongoing insurance obligations. Ratings below this — such as B+ (Good) or lower — signal increasing vulnerability to adverse underwriting or economic changes.

No state law explicitly mandates a minimum A.M. Best rating for VSC backing, but industry best practice consistently points to A- or better as the standard.

Some programs label themselves "fully insured" under definitions that vary by state. Request written confirmation of the insurer's rating and the structure of coverage behind the contract. California, for example, requires all VSC providers to show the name and address of a backup insurance company authorized by the state Department of Insurance. If a provider or dealer fails to pay claims due to insolvency, the backup insurer must step in.

Coverage Plan Variety and Flexibility

A strong VSC provider should offer multiple coverage tiers — at minimum powertrain, named component, and named exclusion — so your F&I office can match coverage to each vehicle's age, mileage, and customer budget without losing the sale.

Common coverage tiers include:

- Powertrain Coverage — Basic coverage for engine, transmission, driveshaft, axles, and differentials

- Named Component Coverage — Lists specific covered parts by name; scope falls between powertrain and exclusionary

- Named Exclusion Coverage — The broadest level; covers every mechanical part except specifically excluded items (wear-and-tear items, brake pads, tires, wiper blades, fluids, glass)

If your inventory includes high-end imports, high-mileage vehicles, diesel engines, or lifted trucks, confirm the provider covers them competitively. Some administrators exclude these vehicle types entirely or price them prohibitively. Research the most common vehicle types in your portfolio and verify coverage availability before committing to a provider.

Claims Handling Process

Claims handling directly reflects on your dealership. Even if the customer signed with a third-party provider, when a claim is denied or delayed, the customer often returns to the selling dealer with complaints.

Ask providers these questions:

- Who authorizes claims?

- What is the average claim approval time?

- Is there a live claims adjuster available during business hours?

- How are "gray area" claims handled — situations where coverage isn't clearly defined in the contract?

The best VSC providers have a discretionary fund and a senior adjuster who can approve borderline claims proactively rather than defaulting to denial. According to J.D. Power's 2026 U.S. Customer Service Index, when overall dealer service satisfaction is 950 or higher, 86% of mass market customers say they "definitely will" return to the dealer for paid service.

Claims satisfaction plays a direct role in driving that loyalty — which means how your VSC provider handles disputes directly affects your service lane retention.

Profit Structure and Dealer Revenue Opportunity

Three arrangement structures determine how much revenue your dealership actually keeps:

- Standard reseller markup — One-time gross per contract sold

- Profit participation — Partial year-end return based on claims performance

- Dealer-owned reinsurance — Full underwriting profit retained when claims come in below reserves

Over 3-5 years, the gap between these arrangements is significant. In the standard model, a dealer might earn $1,000 gross per contract sold. In a dealer-owned structure, that same contract generates the upfront markup plus underwriting profit when claims come in below premium reserves — potentially doubling or tripling the total return per contract over time.

Chargeback considerations: Ask whether the provider offers a no-chargeback option for cancellations, and understand your liability for refunding markup if a contract is cancelled early. Aftermarket product chargebacks from early cancellations — primarily driven by loan refinancing — are squeezing already tight F&I profits, forcing large dealer groups to hire additional staff to manage cancellations and refunds.

F&I Training, Staff Support, and Technology Integration

The best VSC product won't perform if your F&I office doesn't know how to present it. Look for a provider that offers:

- In-person and online F&I training

- Menu-selling tools

- Ongoing performance reporting to track penetration rates and gross per deal

Menu selling shifts the customer mindset from a "Yes/No" decision to a "Which Option?" decision, which drives measurable close rate improvement. Three-tier menus (Good/Better/Best) convert 15-20% of customers to the top tier. A 15-point VSC penetration improvement — from 35% to 50% — at an average VSC gross of $1,200 across 100 monthly deals equals $18,000 in additional gross per month.

Ask whether the provider's platform integrates with your DMS or F&I menu software, and whether they have dedicated account managers who visit or communicate regularly — not just a 1-800 number for problems.

How DealerRE Helps Dealerships Capture More F&I Profit

Founded in 1994 by Tim Byrd, DealerRE has spent three decades helping dealerships across the country move beyond the standard third-party VSC model and into dealer-owned admin obligor reinsurance — a structure where the dealer's own reinsurance company, backed by A-rated insurers, sits in the profit layer of every F&I product sold.

DealerRE sets up and manages each dealership's reinsurance company from formation through ongoing operations, including legal filings, tax returns, compliance, claims adjudication, financials, and bookkeeping. Dealers get the profitability of owning the underwriting entity without having to build the infrastructure themselves.

F&I Development and Training Support

DealerRE provides F&I training (in person and online), F&I menus, and performance analysis so dealers not only capture more profit per contract but also increase overall VSC penetration. The company has helped more than 400 dealers nationwide improve their F&I programs, with several clients earning National Quality Dealer of the Year recognition through NIADA.

Investment and Wealth Building

Better training drives higher VSC penetration — and that income doesn't have to sit idle. Earned reinsurance premiums can be reinvested however the dealer principal chooses:

- Real estate purchases

- College funding for family

- Dealership facility upgrades or inventory

- Watercraft or other personal assets

This gives dealers a long-term wealth-building vehicle tied directly to their F&I volume.

DealerRE's admin obligor reinsurance model is available to a broad range of dealer types:

- Franchise dealers

- Independent and used car dealers

- Buy Here Pay Here (BHPH) dealers

Coverage extends across the full F&I product mix — VSCs, GAP, collateral protection insurance, and ancillary products like tire and wheel or windshield coverage — so dealers capture underwriting profits on every product they sell, not just service contracts.

Conclusion

Choosing a VSC provider is a business structure decision — one that determines how much of every contract's premium stays in your dealership for years to come. The arrangement you select shapes whether you earn a one-time markup or build a multi-million-dollar profit stream over the life of your business.

Before signing with any VSC provider, push past the surface pitch and ask the questions that actually matter:

- Who holds the profit reserve — you or the provider?

- What happens to unearned premium at cancellation?

- Does your current structure include a reinsurance option that lets you own the underwriting upside?

- What is your total revenue potential per contract, not just the front-end markup?

The gap between a standard reseller model and a dealer-owned reinsurance structure is not a matter of degree. A standard resell arrangement caps your income at the point of sale. A properly structured reinsurance program lets you capture 100% of the underwriting profit you've already earned.

Companies like DealerRE work specifically with dealers to evaluate which structure fits their volume, risk tolerance, and long-term goals. Whichever direction you go, choose a provider who can show you — with real numbers — what you're keeping and what you're giving away.

Frequently Asked Questions

What are the two types of vehicle service contracts?

VSCs are generally categorized as named component coverage (which covers only specifically listed parts) and named exclusion coverage (which covers everything except what is explicitly excluded). Named exclusion provides the broadest protection and is generally the stronger option for customers.

Who is the administrator of the vehicle service contract?

The administrator is the company responsible for adjudicating and paying approved repair claims, separate from the insurer who backs the contract financially and the dealership that sells it.

Is offering a VSC worth it for a dealership?

VSCs are one of the most profitable F&I products a dealership can offer, particularly when structured with a profit participation or dealer-owned reinsurance arrangement that allows the dealer to retain underwriting profit beyond the initial markup.

Who is the best VSC provider for auto dealers?

The best provider depends on the dealership's inventory mix and profit goals. Dealers focused on maximum financial return should evaluate whether a dealer-owned reinsurance structure makes more sense than reselling a third-party product.

What is dealer-owned reinsurance and how is it different from selling a third-party VSC?

Dealer-owned reinsurance means the dealership establishes its own reinsurance company (insured by an A-rated carrier) that sits in the profit layer of each VSC sold, allowing the dealer to capture underwriting profits that would otherwise go to the third-party administrator.