Introduction

Front-end vehicle profits have been shrinking for two years straight. According to VisionAST's 2025 dealership profitability report, sales profit per unit has dropped 67% since Q3 2023 — and F&I now accounts for 73% of total dealership profit, up from 56% just a year earlier.

That shift changes the math on reinsurance. Most dealers are already selling vehicle service contracts, GAP, and ancillary products — and handing the underwriting profits to third-party providers. Dealer reinsurance is how you stop doing that.

This article covers the four main reinsurance structures and how they compare across tax treatment, control, and cost:

- CFC (Controlled Foreign Corporation)

- NCFC (Non-Controlled Foreign Corporation)

- DOWC (Dealer-Owned Warranty Company)

- Retrospective Commission

Whether you're a single-point independent or running a multi-rooftop group, the opportunity is the same: treat reinsurance as a fifth business unit alongside sales, service, parts, and F&I.

TL;DR

- Dealer reinsurance lets you share in the underwriting profits of F&I products you already sell, instead of letting third parties keep them

- The four main structures (CFC, NCFC, DOWC, and Retro) each differ in tax treatment, control level, setup cost, and premium capacity

- CFCs work best for independent and mid-sized dealers; NCFCs fit high-volume groups; DOWCs offer domestic ownership; Retros need no upfront capital

- Your best structure depends on premium volume, tax strategy, how much control you want, and capital on hand

What Is Dealer Reinsurance?

Dealer reinsurance is a financial arrangement where a dealership establishes or participates in an insurance entity to capture the underwriting profits on the F&I products it already sells. Instead of all that premium flowing to a third-party administrator or carrier, a portion is ceded to the dealer's own reinsurance company.

Those products typically include:

- Vehicle service contracts

- GAP coverage

- Credit life and disability

- Ancillary protection products (tire & wheel, door ding, windshield, theft)

The concept has been around since the 1950s, when Texas-domiciled insurance companies were first formed to reinsure credit life and disability products. As state regulations evolved, the industry migrated first to Arizona, then eventually to offshore domiciles for lower regulatory costs. The Tax Reform Act of 1986 formalized the tax framework that most CFC programs operate under today.

Reinsurance as a Fifth Business Unit

Sales, service, parts, and F&I each get monthly performance reviews, KPIs, and dedicated management attention. A well-run reinsurance program earns the same. When managed with proper product mix analysis, loss ratio monitoring, and regular cession statement reviews, it functions as a standalone profit center, not just a passive tax structure.

Dealers who treat it as "set it and forget it" consistently leave money on the table. Those who actively manage it — tracking product eligibility, reviewing investment income, and monitoring claims — build programs that grow in value year over year.

The Four Main Dealer Reinsurance Structures Explained

All four structures let dealers participate in underwriting and investment income. They differ significantly in ownership, domicile, tax election, control, and who they're best suited for.

Controlled Foreign Corporation (CFC / PARC)

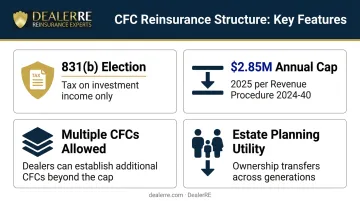

A CFC — sometimes called a Producer-Affiliated Reinsurance Company (PARC) — is a foreign-domiciled corporation owned by the dealer. In its first year, it makes an 831(b) tax election, meaning it pays federal income tax only on investment income, not underwriting profits. The IRS set the 2025 annual net premium cap at $2.85 million per company under Revenue Procedure 2024-40.

Despite the "foreign" label, assets and reserves are held in U.S. financial institutions through trust accounts — nothing goes offshore. The CFC makes an election under IRC Section 953(d) to be taxed as a U.S. domestic insurance company.

Key structural features:

- 831(b) election — federal tax applies only to investment income, not underwriting profits

- $2.85 million annual net premium cap (2025, per Revenue Procedure 2024-40)

- Multiple CFCs allowed — dealers who exceed the cap can establish additional CFCs with slightly differing ownership structures, each qualifying independently

- Estate planning utility — ownership transfers cleanly across generations, making CFCs a practical vehicle for family succession

Non-Controlled Foreign Corporation (NCFC)

An NCFC is a multi-owner foreign reinsurance company with at least 11 unaffiliated U.S. shareholders. The dealer purchases preferred shares but is not an officer, director, or controlling shareholder. Premiums are ceded monthly with no annual cap, making this structure attractive for large groups that have outgrown the 831(b) threshold.

The key tradeoffs:

- No premium ceiling — accommodates unlimited premium volume

- Limited control — the dealer participates but doesn't direct the company; a Board of Directors governs decisions

- 1% federal excise tax under IRC Section 4371 applies to all ceded premiums

- Personal tax returns of shareholders require additional disclosure filings

Dealer-Owned Warranty Company (DOWC / DHWC)

A DOWC is a domestic corporation owned by the dealer that acts as the obligor on service contracts sold. It qualifies as an insurance company for federal income tax purposes, allowing it to utilize insurance-company tax treatment — often resulting in minimal taxable income in early years due to net operating losses and administrative expenses.

At the state level, however, it's not regulated as an insurance company; instead, it must comply with state-level service contract provider standards.

Key distinctions:

- No premium ceiling, but requires significant upfront capitalization — typically $100,000–$250,000 (GPWA)

- Limited to non-insurance products (VSCs and service contracts; not GAP or credit life)

- Tax deferrals in early years shift to full corporate income tax liability over time — dealers need a clear plan for that transition

Retrospective Commission (Retro / Contingent Commission)

Unlike the three structures above, the Retro plan requires no company formation and no upfront capital. Dealers participate in the underwriting bottom line through a commission paid after claims and expenses are settled — the lowest barrier to entry of all four options.

The tradeoffs:

- Distributions taxed as ordinary income (not capital gains)

- No ownership stake, no investment income accumulation

- No control over the entity or claims decisions

- Fastest cash flow, lowest long-term wealth-building potential

Comparing Reinsurance Structures: CFC, NCFC, DOWC, and Retro

The right structure depends on the dealer's specific financial picture. Here's where each option actually differs.

Tax Treatment Comparison

| Structure | Tax on Underwriting Income | Tax on Distributions | Excise Tax |

|---|---|---|---|

| CFC | None (831(b) election) | Often capital gains rate | None (953(d) election) |

| NCFC | None (foreign corp.) | Varies | 1% on premiums (§4371) |

| DOWC | Deferred early; full C-Corp later | Corporate income tax | None |

| Retro | N/A (commission model) | Ordinary income | None |

A qualified CPA or tax attorney should be part of any structure decision — the differences above create meaningfully different long-term tax pictures.

Control and Flexibility Comparison

- CFC: Full ownership, officer/director status, ability to borrow against surplus or unearned premiums, estate planning utility

- NCFC: Participation without directional control; Board governs investment and operational decisions

- DOWC: Full domestic ownership with complete contract customization; claims control

- Retro: No ownership, no management responsibility, no claims involvement

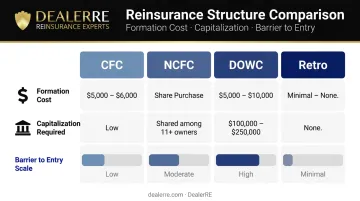

Setup Cost and Capital Requirements

| Structure | Formation Cost | Capitalization |

|---|---|---|

| CFC | ~$5,000–$6,000 | Low (varies) |

| NCFC | Share purchase | Shared among 11+ owners |

| DOWC | $5,000–$10,000 | $100,000–$250,000 |

| Retro | Minimal/none | None |

CFC formation costs of approximately $5,000–$6,000 are confirmed by AutoSuccessOnline. The DOWC's substantially higher capitalization requirement is the primary reason many dealers start with a CFC instead.

Investment Income Potential

That capital commitment to an ownership structure — CFC, NCFC, or DOWC — earns returns. All three accumulate investment income on reserves held in trust between premium transfer and claim or dividend payment. Retro programs generate no investment assets for the dealer.

According to Captive.com, captive investment income commonly falls in the mid-single-digit percentage range, while captive combined ratios typically run in the high-80s — compared to the high-90s for commercial insurers. That spread is where the compounding happens.

Over a 5–10 year program, investment income on reserves becomes a second revenue stream on top of underwriting profits. For dealers evaluating which structure fits their operation, that return potential is worth factoring alongside setup costs and tax treatment.

Key Factors to Consider When Choosing Your Structure

No two dealerships have identical tax situations, premium volumes, family structures, or growth plans. Use these factors as a decision checklist — each one narrows your options based on your actual numbers and goals.

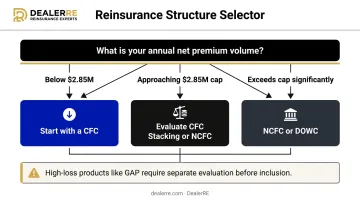

Annual Net Premium Volume

The $2.85M 831(b) cap is the clearest structural decision point. A dealership retailing 1,100–1,570 vehicles annually at an average F&I PVR of $1,818–$2,534 approaches or exceeds that threshold — meaning structure selection isn't just arbitrary, it's mathematical.

- Comfortably below $2.85M: Start with a CFC

- Approaching or exceeding cap: Evaluate CFC stacking, an NCFC, or a DOWC

- Product mix matters too: GAP carries historically higher and more volatile loss ratios. CBT News reports that longer loan terms, higher LTV ratios, and depreciation patterns have driven claim frequency upward — meaning GAP exposure requires active evaluation before including it in a reinsurance program

Ancillary products like tire-and-wheel and environmental protection, by contrast, carry extremely low loss ratios and can strengthen overall portfolio performance.

Tax Goals and Advisor Relationships

Involve a CPA, attorney, and wealth manager before selecting a structure:

- CFC: Clearest long-term tax picture for most dealers — no tax on underwriting income, dividends often treated at capital gains rates

- DOWC: Defers taxes early but creates a future liability that requires deliberate planning

- Retro: Income is ordinary and taxed immediately — no deferral, no preferential rate

Desired Level of Control

Your preferred involvement level matters as much as the numbers:

- Full ownership and control (investment decisions, loan access, claims involvement, estate planning): CFC or DOWC

- Turnkey with minimal oversight: NCFC or Retro

- Claims control — the ability to influence how customer claims are handled — is only available in structures where you own the entity

Long-Term Goals: Wealth Building vs. Cash Flow

Retro distributions come faster. CFC and NCFC reserves compound over time and can fund retirement, real estate, dealership reinvestment, or education. Align your structure with a 5–10 year financial plan, not just this year's tax calendar.

Since 1994, DealerRE has worked with dealers who've used accumulated reinsurance profits for real estate, college funding, and dealership expansion — because the structure was built around long-term goals from day one.

How to Build a Successful Dealer Reinsurance Program

Selecting the right structure is step one. The program still has to be actively managed.

Many dealers leave significant money on the table by not reviewing cession statements regularly, ignoring loss ratio trends, or letting product mix drift without analysis. A program that made sense at startup may need adjustment as volume grows, product penetration shifts, or claim patterns change.

Product selection matters as much as structure selection. Not every F&I product belongs in a reinsurance program. High loss ratio products can erode underwriting profits quickly. A good provider will analyze individual product performance separately from total volume and help build a mix that balances premium income with manageable claim exposure.

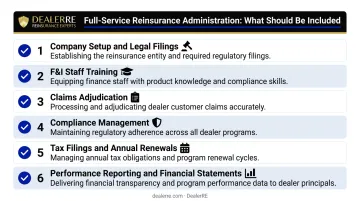

What Full-Service Administration Should Include

A reinsurance partner should cover the full scope of program operations. The full stack includes:

- Company setup and legal filings

- F&I staff training (online and in-person)

- Claims adjudication

- Compliance management

- Tax filings and annual renewals

- Performance reporting and financial statements

DealerRE's admin obligor model covers all of this in a single integrated program. Dealers get an insured reinsurance company backed by A-rated carriers, with claims management, legal filings, financial reporting, and F&I training handled by one team. That lets the dealer stay focused on selling.

The structure also carries a built-in liability safeguard: if the dealer's reinsurance company can't meet an obligation, ultimate liability rests with the direct writing insurance company, not the dealer.

Frequently Asked Questions

What is dealer reinsurance and how does it work?

Dealer reinsurance is a financial arrangement where a dealership participates in its own insurance entity to capture the underwriting profits on F&I products it sells. Premiums are ceded into the entity monthly, profits accumulate alongside investment income, and distributions are returned to the dealer — rather than staying with a third-party provider.

What is a controlled foreign corporation?

A CFC (also called a PARC) is a foreign-domiciled corporation owned by the dealer that takes an 831(b) tax election, meaning it pays taxes only on investment income — not underwriting profits. Despite the offshore domicile, all assets and reserves are held in U.S. financial institutions through trust accounts.

What is an example of a controlled foreign corporation?

A single-point independent dealer generating $1.5M in annual net F&I premiums sets up a CFC, cedes premiums monthly, earns investment income on accumulated reserves, and takes dividends at capital gains rates — all while paying no federal tax on underwriting profits.

What is the difference between a CFC and a dealer-owned warranty company?

A CFC is foreign-domiciled, takes an 831(b) election from day one, and requires no large capitalization — unlike a DOWC, which is domestic, defers taxes early but becomes fully taxable later, and needs $100,000–$250,000 upfront. CFCs also cover insurance products; DOWCs are limited to non-insurance service contracts.

What F&I products can be included in a dealer reinsurance program?

Vehicle service contracts, powertrain warranties, GAP, credit life, tire-and-wheel, door ding, theft protection, and windshield repair are all commonly reinsured. Each product carries different loss ratio risk, so selection should be evaluated individually before inclusion.

Is dealer reinsurance a good option for independent or BHPH dealers?

Yes — reinsurance isn't limited to franchise dealers. Independent and BHPH dealers can establish admin obligor programs to cover mechanical breakdown and fund insurance losses through their customer base. BHPH programs can also be structured with monthly premium billing to protect cash flow.