Understanding earned premium is fundamental for any dealer running a reinsurance program. Get this wrong, and you're reading your own financials incorrectly: overstating income, underestimating reserves, or misreading the loss ratio that tells you whether your program is actually building wealth.

This article breaks down what earned premium means in the reinsurance context, how it differs from written and unearned premium, how it's calculated, and why it directly shapes the profitability of a dealer-owned reinsurance company.

TL;DR

- Earned premium is the share of reinsurance premium allocated to the portion of the policy period that has already elapsed—what the reinsurer has actually "earned" by bearing risk during that time

- Reinsurance premiums are paid at policy inception but recognized as revenue incrementally as the coverage period passes

- The two primary calculation methods are the pro-rata method (time-based) and the exposure method (risk-distribution-based)

- In dealer-owned reinsurance programs, earned premium shapes revenue recognition, loss ratio tracking, and how reserves get deployed

What Is Earned Premium in Reinsurance?

Earned premium is the portion of total written premium that corresponds to the coverage period already elapsed. It's the premium the reinsurer has actually earned by bearing risk during that time — nothing more.

In a reinsurance structure, the ceding insurer—typically the fronting or obligor carrier—issues the policy to the consumer and passes a portion of the premium to the reinsurer at or near policy inception.

That reinsurer cannot book the full amount as revenue on day one. Instead, it sits as unearned premium—a liability representing the reinsurer's obligation to provide coverage through the remainder of the term.

As coverage is provided month by month, that liability converts—premium moves from unearned to earned. The vehicle service contract analogy below makes this concrete for dealer-owned reinsurance.

The Auto Dealership Analogy

Consider a customer who purchases a 3-year vehicle service contract. The full premium flows to your reinsurance company at inception. But on day one, you haven't covered three years of mechanical breakdown risk—you've covered none of it. The NAIC's SSAP No. 53 is explicit here: premiums "shall be recognized as revenue over the period of the contract in proportion to the amount of insurance protection provided."

That $1,500 premium earns month by month. The reinsurer holds the unearned balance as a liability until coverage obligations are fulfilled.

Why the Reinsurance Layer Matters

General insurance and reinsurance earned premium follow the same mechanics, but the reinsurance layer adds a structural step. Risk is first assumed by the fronting/obligor carrier, then shared with the dealer's reinsurance company. This structural step has a direct implication for how your reinsurance entity records income:

- Premium receipt date does not trigger revenue recognition

- Earning follows the underlying consumer contract's schedule — month by month as coverage is provided

- Unearned balances remain a liability on your books until the corresponding coverage period has passed

- Ceded premium timing from the fronting carrier may differ from the consumer policy's start date, requiring careful tracking

Understanding this sequence is the foundation for reading your reinsurance company's financial statements accurately.

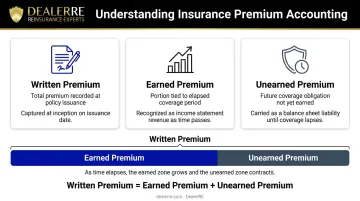

Earned Premium vs. Written Premium vs. Unearned Premium

These three metrics are related but measure completely different things. Every dealer principal running a reinsurance program needs to track all three.

| Metric | What It Measures | Balance Sheet Treatment |

|---|---|---|

| Written Premium | Total premium charged when the policy is issued | Recorded at contract inception |

| Earned Premium | Portion corresponding to elapsed coverage time | Revenue on the income statement |

| Unearned Premium | Portion corresponding to future coverage not yet provided | Liability on the balance sheet |

The relationship is simple: Written Premium = Earned Premium + Unearned Premium at any point in a policy's life.

Why Unearned Premium Is a Liability

Unearned premium isn't just an accounting concept—it represents a real obligation. If a VSC is cancelled mid-term, the unearned portion is typically owed back to the policyholder or ceding party. The Insurance Information Institute frames it plainly: unearned premium is "the amount that the company would owe its policyholders if the company suddenly went out of business."

A Concrete Example

Take a 12-month VSC reinsurance premium of $1,200:

- After 3 months: $300 earned (25%), $900 unearned (75%)

- After 6 months: $600 earned (50%), $600 unearned (50%)

- After 12 months: $1,200 earned (100%), $0 unearned

For a dealer-owned reinsurance company, miscalculating either position distorts your income statement, creates compliance exposure, and makes it impossible to accurately gauge whether your program is actually profitable.

How Earned Premium Is Calculated

Two methods govern earned premium calculation. Most dealer reinsurance programs use the first; understanding both helps you grasp why certain products earn differently.

Accounting (Pro-Rata) Method

The pro-rata method assumes risk is distributed evenly across the policy term and divides premium proportionally by time elapsed.

Formula: Earned Premium = Total Premium × (Elapsed Days ÷ Total Policy Days)

Worked example for a VSC:

- Contract: 36-month (1,095-day) VSC with $1,500 ceded premium

- After 12 months (365 days): $1,500 × (365 ÷ 1,095) = $500 earned

- Unearned balance: $1,000

The Casualty Actuarial Society's Premium Accounting study note confirms this is the most common approach, as it "assumes that the insurance protection is evenly spread over the policy term." NAIC SSAP 53 also recognizes both daily and monthly pro-rata variants.

Exposure Method

The exposure method earns premium as risk is actually incurred rather than uniformly over time. It's used when loss distribution across the policy term is clearly uneven across the term.

CAS research published in Variance documents a meaningful difference between contract types:

- New-car VSC contracts: "Heavily back-ended": losses cluster in later years because OEM factory warranties absorb early failures. Pro-rata earning may overstate earned premium relative to actual early-term risk.

- Used-car VSC contracts: "Front-loaded": claims emerge sooner. Pro-rata may understate earned premium relative to actual early-term risk.

Practical takeaway: Most dealer reinsurance programs use pro-rata for administrative simplicity and regulatory clarity. But if your book is heavily skewed toward used vehicles, your loss ratios may look worse than reality in early months—a nuance worth discussing with your program administrator.

How Reinsurance Earned Premium Timing Works

Upfront Cash, Deferred Revenue

In a dealer-owned reinsurance structure, the full ceded premium typically transfers to the reinsurance trust at or near policy inception. The money arrives early. However, accounting treatment requires that revenue be recognized gradually — matching earned premium to the actual risk period covered by each policy, not the date the cash was received.

This timing gap matters. Cash sitting in the trust is not the same as income you can claim. Until the underlying policy risk has been "used up" through elapsed coverage time, that premium remains unearned on the books.

Why the distinction matters for dealers:

- Unearned premium represents funds held in reserve against future claims — it stays on the liability side of your reinsurance company's balance sheet

- Earned premium is the portion that has been recognized as revenue, corresponding to the coverage period that has already passed

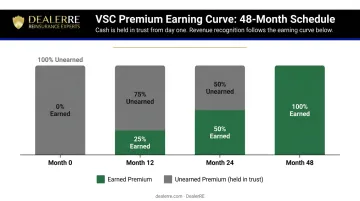

- The earning curve typically follows a pro-rata schedule, releasing premium ratably over the policy term (often 12–60 months depending on the product)

For a vehicle service contract written with a 48-month term, only one-48th of the ceded premium earns each month. After 12 months, roughly 25% of that policy's premium has been earned — the remaining 75% stays classified as unearned reserve.

This is not a cash flow problem. Your trust holds the full premium from day one. It is an accounting classification that determines when revenue flows to your income statement and how your program's financial reports reflect profitability over time.