Introduction

When a customer signs for a vehicle service contract or GAP protection in your F&I office, that premium doesn't just disappear. For most dealerships, it goes straight into a third-party provider's pocket.

That's the arrangement most dealers have accepted for decades. The third-party provider takes the premium, absorbs the risk, and pockets the underwriting profit — while your dealership walks away with a flat commission.

Reinsurance changes that dynamic. A dealer who owns their reinsurance company becomes the risk-bearer and the profit-taker. According to NADA Data 2025, F&I and other income represented roughly 26.4% of total dealership gross profit in 2024. That's a substantial pool most dealers are leaving on the table.

This article breaks down the four distinct revenue streams that dealer-owned reinsurance companies generate, and why understanding them is the first step toward evaluating whether this model makes financial sense for your operation.

TLDR

- Dealers who own their reinsurance company capture premium income instead of handing it to a third party

- Underwriting profit (premiums minus claims) is the primary revenue stream dealers currently forfeit

- Reserve funds earn investment income while held, adding a second layer of return

- Claim-free expired contracts generate passive runoff profits that compound as the program matures

What Is a Reinsurance Company?

The National Association of Insurance Commissioners (NAIC) defines reinsurance as a contract in which a reinsurer assumes all or part of the risk under policies issued by a primary insurer — the "cedent." The cedent transfers both risk and premium to the reinsurer through a process called cession. In exchange, the reinsurer agrees to pay a share of future claims.

For auto dealers, this creates a specific opportunity. A dealer can establish their own reinsurance company to receive a portion of the premiums generated from F&I products sold at their dealership. When the F&I product provider (acting as the primary insurer) cedes policies to the dealer's reinsurance company, it transfers both the risk and the associated premium income.

Dealer-Owned vs. Traditional Reinsurers

That distinction matters when comparing dealer-owned structures to traditional reinsurers:

| Type | Who it is | What it does |

|---|---|---|

| Traditional reinsurer | Large institutional company (Munich Re, Swiss Re) | Writes risk across many clients and industries |

| Dealer-owned reinsurance company | Privately held entity owned by the dealer | Captures underwriting profit from that dealer's F&I sales only |

DealerRE helps dealers establish what's called an admin obligor reinsurance company: a structure backed by A-rated insurers. The dealer's company assumes administrative obligations, while established carriers maintain ultimate liability for claims. This limits dealer exposure to formation costs plus accumulated earnings, while still allowing full participation in underwriting profits.

Revenue Stream #1: Premium Income from Ceded Policies

The foundational revenue stream for any reinsurance company is the premium it receives through cession. Each time a dealer sells an F&I contract — a vehicle service contract, GAP protection, collateral protection insurance, or an ancillary product like tire and wheel coverage — a defined portion of the retail premium flows into the dealer's reinsurance company rather than staying with the third-party provider.

How the Premium Flow Works

In a dealer reinsurance program, premiums move into a trust account as unearned premium reserves (UPR) — funds set aside to cover future claims. A fronting carrier and administrator receive contractual fees, and as time elapses without claims, those premiums are gradually "earned."

Remaining funds accumulate in a surplus account (often called a "B account") that can be invested more aggressively than the conservatively managed UPR.

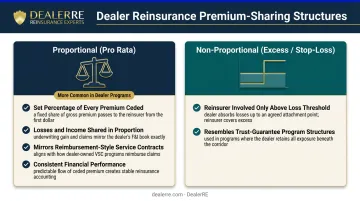

Two structural approaches govern how premium sharing is arranged:

- Proportional (pro rata): The reinsurer receives a set percentage of every premium from the ceded policies — losses and income are shared in direct proportion. This mirrors a reimbursement-style service contract policy.

- Non-proportional (excess/stop-loss): The reinsurer only becomes financially involved when losses exceed a defined threshold. This resembles a trust-guarantee program where the insurer pays after the trust is exhausted.

Proportional structures are more common in dealer reinsurance programs because they align premium and loss exposure consistently over time, making financial performance easier to monitor and project. That consistency also sets the stage for the second major revenue source: investment income generated on the reserves your program accumulates.

Revenue Stream #2: Underwriting Profit — Keeping What's Left

Underwriting profit is the difference between premiums collected and claims paid. It's the most significant revenue stream in dealer reinsurance — and third-party providers have been retaining it for years without dealers realizing how much they're leaving behind.

The math is straightforward: if your reinsurance company takes in $X in premium and pays $Y in claims, the remaining balance is underwriting profit. When you sell F&I products through an outside provider, they keep that balance. When you own your reinsurance company, you keep it.

Why Claims Management Is Non-Negotiable

Underwriting profit isn't passive. It's directly tied to how well you manage claims.

Actuarial research on extended service contracts, published in Variance journal, documents that VSC claims tend to be low-severity but higher-frequency. It also finds that mispricing can hide adverse loss development for years, particularly as back-ended claims emerge after manufacturer warranty periods expire. That's a real risk for any reinsurance program that doesn't take pricing and claims discipline seriously.

Operational decisions matter too. Keeping repairs in-network and managing deductible structures can reduce per-repair-order claim costs by roughly $400–$600. Ancillary products — tire and wheel, door ding, windshield — typically carry much lower loss ratios than VSCs, making them attractive additions to the product mix.

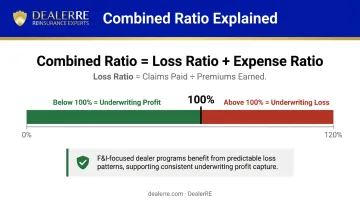

The Combined Ratio

The standard performance benchmark for reinsurance profitability is the combined ratio:

Combined Ratio = Loss Ratio + Expense Ratio (Loss Ratio = Claims Paid ÷ Premiums Earned)

A combined ratio below 100% means the reinsurance company is paying out less than it takes in — underwriting profitability. Dealer programs focused on F&I product lines like VSCs, GAP, and ancillary products tend to have more predictable loss patterns than large institutional reinsurers writing across multiple risk categories. When dealers price programs correctly and administer them well, that predictability supports favorable combined ratios.

That's the structure DealerRE uses with its admin obligor model — monthly performance monitoring with claims losses tracked and operations projected through contract earn-out, so dealers can see exactly where their underwriting profit stands.

Revenue Stream #3: Investment Income on Reserve Funds

Reinsurance companies don't immediately pay out all premiums received. Those funds sit in reserve — sometimes for the full term of a multi-year service contract — waiting to cover potential claims. That waiting period creates a second layer of return.

Conservative Reserves, Flexible Surplus

Investment strategy typically splits across two pools:

- UPR (trust account): Invested conservatively in government bonds and rated fixed-income instruments, subject to insurance regulatory requirements. Liquidity and capital preservation come first.

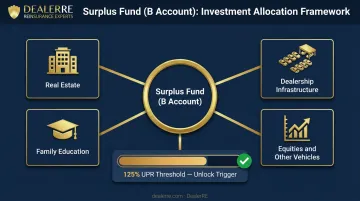

- Surplus/B account: Once accumulated cash exceeds 125% of unearned premiums, excess funds can be invested at the direction of the reinsurance company's ownership — with significantly more flexibility.

The Captive Insurance Companies Association (CICA) guidance for small captives emphasizes asset-liability matching as a core principle — aligning investment duration with the expected claim payment timeline. That discipline protects solvency while allowing the surplus account to pursue better returns.

What Dealers Can Do with Surplus Funds

DealerRE's program gives dealers meaningful flexibility once the surplus threshold is cleared:

- Purchase real estate

- Reinvest in dealership infrastructure

- Fund college education for family members

- Invest in equities or other vehicles

A dealer writing $500K in annual premiums doesn't just accumulate reserves — they build an investable asset base that grows with volume. At scale, that surplus account becomes a genuine wealth-building tool, not just a claims buffer.

Revenue Stream #4: Profits from Matured and Expired Contracts

Every F&I contract has an end date. When that date arrives without a claim, the premium reserved to cover that contract becomes pure profit for the reinsurance company. These are called runoff profits, and they're entirely passive.

This revenue stream grows predictably as a program matures:

- Year one: relatively limited runoff (contracts still in term)

- Years two through four: earlier-issued contracts begin expiring

- Years five and beyond: a growing percentage of the book expires each year, generating consistent surplus flows

The quality of products sold directly shapes this stream. F&I products with clear coverage terms, appropriate pricing, and well-defined exclusions tend to produce favorable claim ratios, meaning more contracts expire untouched.

GAP coverage illustrates this well: a GAP claim requires the joint event of a total loss and a loan balance exceeding actual cash value. Many GAP contracts will never trigger a claim, and that unused premium flows to surplus.

Once those surplus balances accumulate, access depends on reserve requirements. DealerRE's program allows withdrawal of funds exceeding required reserves once the 125% UPR threshold is met — at that point, runoff profits become accessible for distributions, reinvestment, or other uses at the dealer's discretion.

Is Reinsurance a Profitable Business for Auto Dealers?

Dealer reinsurance programs can be genuinely profitable — but the outcome depends on how the program is structured and managed.

These programs capture underwriting profit, investment income, and runoff profits that would otherwise land on a third-party provider's balance sheet. NADA and StoneEagle data reported a 14% increase in F&I profit per vehicle retailed from January through December 2025 — reinforcing that F&I remains a growing profit pool worth owning rather than outsourcing.

What Drives Profitability

The four variables that determine whether a dealer reinsurance program performs well:

- F&I sales volume — programs need consistent contract flow to build substantial premium reserves

- Claims frequency and severity — lower loss ratios produce higher underwriting profit

- Product pricing and design — properly priced products protect the program from back-ended loss development

- Program administration — monthly financial reporting, actuarial oversight, and active performance monitoring keep programs on track

DealerRE recommends dealers selling more than 30 cars per month as strong candidates, with specific program structures available for BHPH dealers and independent retailers as well.

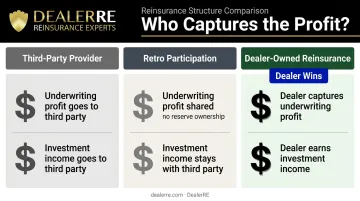

The Real Comparison

| Approach | Who captures underwriting profit | Who earns investment income |

|---|---|---|

| Third-party provider | Third-party provider | Third-party provider |

| Retro participation | Shared (no reserve ownership) | Third-party provider |

| Dealer-owned reinsurance | Dealer | Dealer |

That table reflects where the money actually goes — and the difference is significant at scale. Global institutional reinsurers operate on tight combined ratios and rely heavily on diversified investment portfolios to generate acceptable returns. Dealer reinsurance programs operate in a much narrower niche — VSCs, GAP, ancillary products — with more predictable loss patterns.

That narrower focus, combined with direct claims management and flexible investment options, means well-run dealer programs can produce strong returns. The dealers who see the best results treat their reinsurance company as a managed asset, not a passive arrangement.

Frequently Asked Questions

What is a reinsurance company?

A reinsurance company assumes insurance risk — and the associated premium — from a primary insurer in exchange for agreeing to pay a share of future claims. It functions as insurance for insurers, with the primary insurer (cedent) transferring risk to the reinsurer through a process called cession.

How does a reinsurance company make money?

The three main revenue streams are: premium income received when policies are ceded, underwriting profit (premiums collected minus claims paid), and investment income earned on reserve funds held while waiting to pay future claims. Expired contracts with no claims also contribute passive runoff profits.

Why would an insurance company buy reinsurance?

Primary insurers buy reinsurance to transfer risk, reduce capital requirements, stabilize earnings across volatile loss periods, and expand underwriting capacity beyond what their balance sheet alone would support.

Is reinsurance a profitable business?

It can be, when managed with pricing discipline, efficient claims oversight, and sound investment governance. Dealer-owned reinsurance programs tend to have narrower, more predictable loss exposure than large institutional reinsurers — which makes consistent profitability more achievable for dealers who manage their programs carefully.

What types of F&I products can be included in a dealer reinsurance program?

Most dealer reinsurance programs cover vehicle service contracts, GAP protection, collateral protection insurance, and debt cancellation coverage. Ancillary products — tire and wheel, door ding, windshield repair, and theft protection — are commonly included as well. The specific mix depends on the program structure and dealer type (franchise, independent, or BHPH).

How is a dealer-owned reinsurance company different from a standard reinsurer?

A dealer-owned reinsurance company is a privately held entity established specifically to capture underwriting profits from that dealership's F&I sales. It operates within a narrow, defined product niche — unlike large institutional reinsurers that write risk across many clients, industries, and risk categories.