Neither outcome is acceptable when you're managing your own reinsurance company.

This article breaks down what each term means, how they interact, how the calculation works, and what goes wrong when dealers misunderstand them. Whether you're setting up a new program or managing an established one, getting these mechanics right is foundational to running a profitable, well-structured program.

TL;DR

- Deposit premium is a periodic advance payment—typically quarterly—based on estimated F&I volume, not actual figures

- Minimum premium is the contractual floor the reinsurer will accept for the period, regardless of actual volume

- The two work together: deposits keep cash flowing while the minimum protects the program if volume falls short

- Year-end reconciliation determines whether you owe additional premium, receive a partial refund, or land at the minimum floor

- Accurate upfront estimates are the most effective way to avoid large year-end adjustments in either direction

What Minimum and Deposit Premiums Mean in Dealer-Owned Reinsurance

Deposit Premium

The IRMI defines deposit premium as the amount the ceding company pays to the reinsurer on a periodic basis during the contract term, "determined as a percentage of the estimated amount of premium that the contract will produce based on the rate and estimated subject premium." IRMI lists "provisional premium" as a direct synonym—which is precisely what it is: a provisional advance, not a final settled figure.

In practice, these payments flow quarterly, though some programs use monthly or semi-annual installments depending on program size and structure. The deposit is not an extra charge on top of the actual premium—it is the premium payment, made in advance before exact figures are confirmed.

Subject Premium

In the auto dealer context, subject premium is the underlying pool of F&I product premiums—VSCs, GAP, credit life, ancillary products—to which the reinsurance rate is applied. A dealer's F&I contract volume directly drives this number:

- Higher volume + strong penetration rates → higher subject premium

- Slower months or lower penetration → compressed subject premium

This number is the foundation both the deposit and minimum premium are built on.

Minimum Premium

The Reinsurance Association of America's glossary defines minimum premium simply as "the least amount of premium to be paid to the reinsurer under the terms of the treaty." It's a contractual floor, not a penalty clause. The reinsurer priced the contract assuming a certain level of risk and volume—the minimum premium ensures that pricing remains viable even if the dealership has a slow year.

The deposit is calculated from an estimated subject premium. The minimum is a floor set against the actual subject premium at year-end. That gap—between the estimate used at contract start and the real figures confirmed at reconciliation—is where dealers are most often caught off guard by an unexpected true-up.

How Minimum and Deposit Premiums Are Calculated and Set

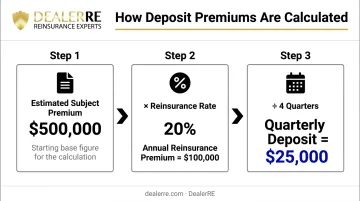

The Basic Calculation

The deposit premium formula is straightforward:

Estimated Annual Subject Premium × Reinsurance Rate = Annual Reinsurance Premium ÷ 4 = Quarterly Deposit

For illustration, assume a dealer estimates $500,000 in annual subject premium and the contract rate is 20%:

- Annual reinsurance premium = $500,000 × 20% = $100,000

- Quarterly deposit = $100,000 ÷ 4 = $25,000 per quarter

That $25,000 flows to the reinsurer each quarter throughout the policy year. At year-end, the actual subject premium is confirmed, and the math gets recalculated against real numbers.

How the Minimum Is Set

Minimum premium is typically set at the same dollar amount as the deposit premium—in the example above, $100,000—though some contracts negotiate a different figure based on risk profile, program history, or dealer volume. IRMI confirms that the deposit premium "is often the same as the minimum premium but may be higher or lower," making clear these are distinct contractual elements that happen to coincide in many standard programs.

Year-End Reconciliation: Three Outcomes

After the policy period closes, actual subject premium is confirmed through audit or reporting. The reconciliation produces one of three results:

| Scenario | What Happens |

|---|---|

| Actuals exceed estimate | Additional premium is owed to the reinsurer |

| Actuals below estimate, above minimum | Partial refund may be due to the dealer |

| Actuals fall below minimum premium | Minimum stands; no refund applies |

This adjustment process is routine, not a penalty or a sign of program failure. Dealers who plan for it treat reconciliation as a normal part of annual program management.

That planning starts with the initial estimate. DealerRE works with dealers to set accurate projections based on historical F&I volume and program composition, then handles premium tracking, filings, and year-end adjustments so reconciliation stays predictable rather than reactive.

Minimum Premium vs. Deposit Premium: Key Distinctions

These two terms are related but serve completely different functions. Conflating them leads to poor planning.

Deposit premium = a timing mechanism. It governs when and how premium flows throughout the contract year. It starts as an estimate and adjusts to reality at reconciliation—meaning it carries built-in variability tied to F&I performance.

Minimum premium = a floor mechanism. Unlike the deposit, it governs how low the total premium can go. It's fixed at contract inception and doesn't move with volume.

The Adjustment Mechanism

After the policy period ends, actual subject premium is audited or confirmed. The outcome depends on where actual volume lands:

- Actual exceeds deposits paid: additional premium is owed

- Actual falls below deposits but stays above the minimum: a refund may apply

- Actual falls below the minimum: the minimum holds, no refund

This is a normal contract cycle event. Dealers who treat it as an unexpected problem typically haven't been monitoring their running F&I volume against their estimates during the year.

One important dynamic in dealer-owned programs: unlike a third-party insurance arrangement, the dealer has a direct economic stake in this adjustment. A higher-than-expected additional premium at year-end often signals F&I volume growth, which is good news for the program's reserve pool and long-term profitability.

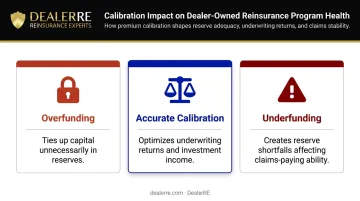

Interaction with Program Profitability

Premium in a dealer-owned program isn't simply a cost that leaves the building. As Mercer Capital explains, dealer-owned programs generate income through two channels: underwriting profits when claims run below premiums collected, and investment income earned on reserves while they're held.

That means accurate premium setting has a direct line to profitability:

- Overfunding ties up capital unnecessarily in reserves

- Underfunding creates reserve shortfalls that affect claims-paying ability

- Accurate calibration keeps the program well-positioned for both underwriting returns and investment income

What Happens When Actuals Diverge from Estimates

When Volume Exceeds Estimates

The dealer owes additional premium at year-end. If that amount wasn't budgeted for, it can create a cash flow demand at an inconvenient time. The solution isn't complicated—monitor running F&I volume quarterly against the original estimate and flag any significant upward trend before year-end.

Dealers who track this proactively can set aside the likely additional premium in advance rather than scrambling when the reconciliation arrives.

When Volume Falls Below the Minimum

The dealer's reinsurance company still pays the minimum premium regardless. No refund applies to the shortfall. In a dealer-owned structure, this isn't a loss—the funds remain within the dealer's program structure funding reserves—but it does affect program economics and should be factored into projections.

Volume dips that trigger the minimum floor can stem from several sources:

- Seasonal sales patterns

- Temporary inventory shortages

- Shifts in product penetration rates

- Broader economic conditions

The Haig Report's Q2 2025 data puts the variance in concrete terms: F&I PVR ranged from roughly $2,048 at Penske to $2,742 at AutoNation, showing how much volume can shift even among large, well-managed dealer groups.

Compliance Implications

The financial impact is one concern. Consistently wide deviations between estimated and actual subject premium can also create issues beyond cash flow. They can flag program management concerns to regulators, affect the A-rated insurer backing that gives dealer-owned programs their credibility, or require contract renegotiation. Maintaining accurate, well-documented premium estimates is part of responsible program stewardship and a core part of keeping the program in good standing.

Common Misconceptions About Minimum and Deposit Premiums

"The deposit premium is an extra charge on top of actual premium"

It isn't. The deposit premium is the premium payment, made provisionally before actual figures are known. At year-end, it reconciles against actuals. There's no double-charging—it's a timing structure, not an additional cost layer.

"Falling below the minimum premium means the program is failing"

Not necessarily. Hitting the minimum floor can reflect a temporary dip from seasonal slowdowns, an inventory shortage, or a product mix change mid-year. These are recoverable situations when addressed early.

The real problem isn't falling below the minimum once — it's consistently missing volume estimates without revisiting program parameters. Common causes worth monitoring include:

- Sustained inventory shortages reducing contract volume

- A shift in product mix that lowers average premium per deal

- Seasonal sales cycles that weren't factored into original projections

"Dealers can waive or informally renegotiate the minimum premium"

The minimum premium is a contractual commitment tied to the reinsurer's pricing and risk assumptions. Arbitrarily reducing it without a formal renegotiation affects program terms, loss ratios, and the dealer's reinsurance relationship.

When business circumstances change — sustained volume decline, major product mix shift — the right path is a structured conversation with your program administrator. That's exactly the kind of proactive guidance DealerRE provides: helping dealers address parameter issues before they become compliance problems or strain the insurer relationship.

Frequently Asked Questions

How does a minimum and deposit premium work?

The deposit premium is a periodic advance payment based on estimated F&I volume; the minimum premium is the contractual floor the reinsurer will accept. At year-end, actual subject premium is confirmed and reconciled against both figures to determine whether an additional premium is owed or a refund applies.

What is the difference between minimum premium and deposit premium in reinsurance?

Deposit premium is a timing mechanism — it governs when and how premium is paid throughout the year, based on volume estimates. Minimum premium is a floor mechanism — it sets the lowest total the reinsurer will accept regardless of actual volume.

What happens if my actual F&I premium falls below the minimum premium?

If actual subject premium produces a reinsurance premium below the contractual minimum, the dealer's reinsurance company must still pay the minimum. No refund is issued for the shortfall, which is why accurate upfront volume estimates matter.

Can deposit premiums be refunded if my dealership's F&I volume decreases?

A partial refund may apply if actual premium falls below the deposits paid but remains above the minimum premium. If actuals fall below the minimum, the minimum stands and no refund is issued.

How are deposit premium amounts determined at the start of a contract?

Deposit premiums are calculated by applying the contract reinsurance rate to estimated subject premium (projected F&I volume for the period), then dividing into installment payments. An accurate upfront volume estimate is critical to avoiding large year-end adjustments.

How do minimum and deposit premiums affect the profitability of a dealer-owned reinsurance company?

Because the premium pool funds reserves and generates investment returns, accurately calibrated minimum and deposit premiums ensure the program is neither over- nor under-funded. That calibration directly affects long-term profitability and the program's ability to build sustainable financial value for the dealer.