Introduction

Most primary insurers couldn't write large commercial policies, survive a catastrophic hurricane season, or satisfy capital requirements without transferring significant risk elsewhere. That's the job of reinsurance: letting carriers offload portions of their exposure to specialized companies built to absorb it. A handful of large American firms dominate that function.

Understanding who those companies are, what they specialize in, and how they differ helps insurers, brokers, and risk managers structure better protection programs. For auto dealers evaluating reinsurance options, it also clarifies the difference between institutional carriers serving Fortune 500 risks and the dealer-owned programs designed specifically for F&I profitability.

This article covers the five biggest American reinsurance companies by net premiums written, what sets each one apart, and how to evaluate them against your specific needs.

TL;DR

- Reinsurers act as "insurers for insurers," accepting risk from primary carriers in exchange for a share of the premium

- The top five American reinsurers by scale: RGA, Berkshire Hathaway, Swiss Re America, Everest Re, and Munich Re America

- Specializations vary: RGA leads in life/health, Swiss Re in catastrophe modeling, and Munich Re in complex emerging risks

- Evaluating a reinsurer requires looking beyond brand — financial strength ratings, combined ratios, and product alignment matter more

- Auto dealers have a separate path: dealer-owned reinsurance structures let dealerships keep F&I underwriting profits, a model DealerRE has supported since 1994

Overview of Reinsurance in the American Market

Reinsurance is a contractual arrangement in which a reinsurance company accepts a portion of the risk from a primary insurer in exchange for a share of the premium, effectively insuring the insurer.

The NAIC describes it simply: "the insurance company — the cedent — transfers risk to the reinsurance company, and the latter assumes all or part of one or more insurance policies issued by the cedent." The Insurance Information Institute adds that reinsurance "increases the capacity of the insurance industry to provide coverage for large and complex risks" that individual insurers couldn't handle alone.

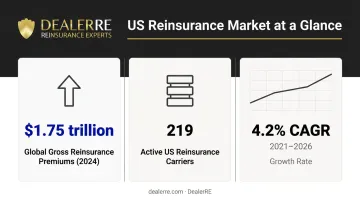

The scale is significant. According to the IAIS Global Insurance Market Report, global gross reinsurance premiums reached $1.75 trillion by the end of 2024. In the US alone, IBISWorld counts 219 active reinsurance carrier businesses, with the industry growing at a 4.2% CAGR between 2021 and 2026.

By spreading risk globally, reinsurance prevents single catastrophic events from bankrupting primary carriers and destabilizing the broader financial system. The risks involved include:

- Hurricanes and coastal weather catastrophes

- Wildfires and widespread natural disasters

- Pandemics affecting large insured populations simultaneously

- Mass casualty or liability events exceeding a single insurer's capacity

A Separate Path for Auto Dealers

Institutional reinsurers serve insurance carriers. They're not built for dealership-level F&I programs. A completely different model exists for auto dealers: dealer-owned reinsurance, sometimes called admin obligor reinsurance, where the dealership establishes its own reinsurance company to underwrite the F&I products it sells — vehicle service contracts, GAP, CPI, and ancillary coverage.

Instead of sharing profits with third-party product providers, the dealer retains 100% of the underwriting income. This is the model DealerRE has specialized in since 1994, and it's distinct from everything covered in the sections below.

The Biggest American Reinsurance Companies

These five companies were selected based on net reinsurance premiums written, US market presence, and breadth of products offered to American insurers.

Reinsurance Group of America (RGA)

Founded in 1973 and headquartered in Chesterfield, Missouri, RGA trades on the NYSE (ticker: RGA) and holds a unique position in the global reinsurance market: it is the only major international reinsurer focused almost exclusively on life and health-related risks.

RGA reported $17.8 billion in total net premiums for FY2024 — an 18.3% year-over-year increase — with its US and Latin America segment alone contributing $7.5 billion. The company ranks #225 on the Fortune 500 and holds an A+ (Superior) rating from AM Best and AA- from S&P.

That specialization defines RGA's competitive position. No other reinsurer of comparable size focuses so narrowly on life and health, covering mortality, longevity, critical illness, disability, and living benefits across 26+ countries.

| Factor | Detail |

|---|---|

| Primary Focus | Life and health reinsurance (mortality, longevity, disability, critical illness) |

| Net Premiums Written | $17.8 billion (FY2024) |

| AM Best Rating | A+ (Superior) |

| Key Differentiator | Only major global reinsurer exclusively focused on life and health |

Berkshire Hathaway Reinsurance Group

Berkshire Hathaway's reinsurance operations run through four main subsidiaries: National Indemnity (NICO Group), General Re, Transatlantic Reinsurance (TransRe), and Berkshire Hathaway Life Insurance of Nebraska. The group is headquartered in Omaha, Nebraska. Gregory Abel became CEO effective January 1, 2026, succeeding Warren Buffett, who remains Chairman.

The numbers here are in a category of their own. BHRG reported $26.9 billion in total net premiums written for FY2024 (P&C: $21.9B; L&H: $5.0B), with a P&C combined ratio of 82.9%. The group's insurance float — premium reserves held for investment — stood at approximately $176 billion at year-end 2025.

That $176 billion float gives Berkshire a competitive edge few can match: the ability to deploy premium reserves into long-duration investments and absorb catastrophic or unusual risks that other reinsurers can't hold on their balance sheets. Its AM Best rating of A++ (Superior) is the highest on the scale.

| Factor | Detail |

|---|---|

| Primary Focus | P&C, life/health, structured reinsurance, and retrocession |

| Net Premiums Written | $26.9 billion (FY2024) |

| AM Best Rating | A++ (Superior) |

| Key Differentiator | Unmatched capital depth and $176B float; underwrites risks others won't |

Swiss Re America

Swiss Re America is the US arm of Swiss Re Group, headquartered in Armonk, New York, with the parent based in Zurich. It covers US insurers across property, casualty, life, and health lines, and holds group ratings of A+ (Superior) from AM Best and AA- from S&P.

The company is best known for catastrophe risk modeling and alternative risk transfer. In December 2025, Swiss Re Capital Markets structured and placed a $400 million catastrophe bond for Farmers Insurance Group — protection against named storms, earthquakes, and severe weather — one of the larger ILS placements of 2025. Swiss Re's P&C Reinsurance division produced a combined ratio of 79.5% in Q1 2026, reflecting tight underwriting performance.

US-specific net premium figures aren't separately disclosed in public filings; Swiss Re reports at the group level.

| Factor | Detail |

|---|---|

| Primary Focus | Property, casualty, life, health, catastrophe, and alternative risk transfer |

| AM Best Rating | A+ (Superior) |

| Key Differentiator | Catastrophe modeling expertise and ILS/alternative risk transfer leadership |

Everest Re

Everest Re (NYSE: EG) operates from Warren, New Jersey, with legal domicile in Bermuda. It offers one of the broadest reinsurance product portfolios in the US market — spanning treaty property, treaty casualty, facultative, surety and credit, marine, aviation, engineering, political violence, and accident and health.

Everest's reinsurance segment reported $11.97 billion in net premiums written for FY2024, with a combined ratio of 89.7%. AM Best rates Everest Reinsurance Company A+ (Superior). In FY2025, the company sold renewal rights on approximately $2 billion of retail commercial insurance to AIG — a strategic move sharpening its focus on wholesale, specialty, and reinsurance lines.

| Factor | Detail |

|---|---|

| Primary Focus | Property, casualty, specialty, surety, marine, aviation, accident/health |

| Net Premiums Written | $11.97 billion (FY2024 reinsurance segment) |

| AM Best Rating | A+ (Superior) |

| Key Differentiator | Highly diversified portfolio across both treaty and facultative structures |

Munich Re America

Munich Re America — formerly American Re-Insurance Corporation, founded in 1917 — is the US subsidiary of Munich Re, the world's largest reinsurance group. Headquartered in Princeton, New Jersey, with regional offices in San Francisco, Chicago, and New York City, it was acquired by Munich Re in 1996 for approximately $3.8 billion. The parent group reported global gross written premiums of $47.8 billion in 2024 with a combined ratio of 83.0%.

Munich Re America holds an A+ (Superior) AM Best rating. AM Best cited the company's "balance sheet strength, which AM Best assesses as strongest, as well as its strong operating performance."

The company's specialty is technical depth in complex and emerging risk categories — cyber, climate-related property exposure, political violence, and healthcare liability — backed by Munich Re's global research and underwriting infrastructure.

| Factor | Detail |

|---|---|

| Primary Focus | Property, casualty, specialty (cyber, climate, healthcare liability, political violence) |

| AM Best Rating | A+ (Superior) |

| Key Differentiator | Deep expertise in emerging and complex risk categories |

What Sets These Reinsurers Apart — And How to Choose the Right One

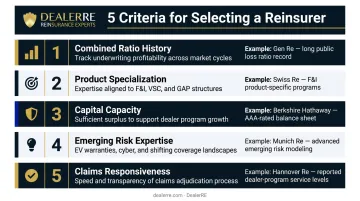

With all five companies holding A+ or A++ AM Best ratings, creditworthiness alone isn't a differentiator. The decision becomes about fit.

Key Evaluation Criteria

- Combined ratio history — Below 100% signals underwriting profit. Berkshire's 82.9% (FY2024 P&C) and Swiss Re's 79.5% (Q1 2026 P&C) indicate exceptional discipline. Everest's 89.7% (FY2024) and Munich Re's group-level 83.0% are similarly strong

- Product specialization — A life insurer should not default to a P&C-heavy reinsurer. RGA's exclusive life/health focus serves a fundamentally different segment than Everest's property-casualty mix

- Capital capacity — For very large or unusual risks, Berkshire's $176 billion float creates options no other reinsurer can match

- Emerging risk expertise — Cyber and climate-related exposure require underwriters who have modeled those categories deeply. Munich Re and Swiss Re lead here

- Claims responsiveness: Financial strength ratings don't measure how quickly a reinsurer responds when losses mount. Track record matters as much as the AM Best letter

Common Selection Mistakes

- Prioritizing brand recognition over product alignment

- Ignoring claims-paying history in favor of premium savings

- Choosing a P&C specialist to reinsure a life or health-heavy book

- Failing to assess scalability — whether the reinsurer can grow with your needs through hard and soft market cycles

A Note for Auto Dealers

The five reinsurers above serve insurance carriers. They're built around carrier-level volumes, regulatory relationships, and risk models that have nothing to do with dealership F&I operations.

Dealers looking to retain the underwriting profits from vehicle service contracts, GAP, and ancillary products aren't shopping for a relationship with Berkshire Hathaway or RGA. They're candidates for a dealer-owned reinsurance structure: a model where the dealership itself becomes the reinsurer for its own F&I book. DealerRE helps dealers build and manage those programs, backed by A-rated insurers, with full administration including claims, tax filings, compliance, and financial reporting.

Conclusion

RGA, Berkshire Hathaway, Swiss Re America, Everest Re, and Munich Re America each represent a different configuration of financial strength, product depth, and risk specialization. The right choice for any primary insurer depends on book composition, risk concentration, and the specific lines requiring protection — not just which name appears most often in industry rankings.

When all five carry top-tier ratings, financial size stops being the deciding factor. What separates a productive reinsurance relationship from a frustrating one is how well the reinsurer's expertise maps to your specific risk portfolio — and how they perform when a claim actually needs to be paid.

For auto dealers, the question looks different. Rather than sourcing reinsurance from an institutional carrier, dealers can structure their own reinsurance company and capture 100% of the F&I underwriting profits currently flowing to third-party providers. DealerRE has been building those programs since 1994 and has helped more than 400 dealers nationwide do exactly that.

If you sell more than 30 cars a month and want to understand what a dealer-owned reinsurance program could mean for your operation, reach out to DealerRE for a complimentary business analysis.

Frequently Asked Questions

What does a reinsurance company do?

A reinsurance company accepts a portion of the risk from a primary insurer for a share of the premium. This protects the primary insurer from catastrophic losses and allows it to write more policies than its balance sheet alone could support — preserving solvency when large claims hit.

Who is the largest reinsurance company in America?

By total net premiums written, Berkshire Hathaway Reinsurance Group reported $26.9 billion in FY2024 — the highest of the five companies covered here. Reinsurance Group of America (RGA) leads specifically in life and health reinsurance, reporting $17.8 billion in total net premiums for the same period.

What is the difference between insurance and reinsurance?

Insurance protects individuals and businesses from financial loss. Reinsurance protects the insurance companies themselves by transferring a portion of their risk to a reinsurer — enabling primary insurers to remain solvent even after large-scale loss events like hurricanes or widespread liability claims.

What is the difference between treaty and facultative reinsurance?

Treaty reinsurance covers an entire portfolio or category of policies under a standing agreement — for example, all of an insurer's commercial auto business. Facultative reinsurance is negotiated individually for specific high-value or unusual risks. Most large institutional reinsurers offer both structures.

What is dealer-owned reinsurance?

Dealer-owned reinsurance (also called admin obligor reinsurance) is a structure where an auto dealership establishes its own reinsurance company to underwrite the F&I products it sells — vehicle service contracts, GAP, and ancillary coverage. Instead of sharing profits with third-party providers, the dealer retains the underwriting income directly.

How do reinsurance companies make money?

Reinsurers earn income two ways: underwriting income (premiums collected minus claims paid) and investment income from deploying premium reserves into bonds, equities, and other instruments. Berkshire Hathaway's $176 billion float generated $13.7 billion in insurance investment income in 2024 — showing how powerful that second revenue stream can become.