Most dealers never ask that question. They focus on the front-end gross, maybe the F&I gross per vehicle, and move on. But the money flowing after the sale — the reserve premiums, the claims float, the underwriting profit — often lands in a third party's account instead of yours.

Understanding the term ceding company is how you start to see the full picture. It identifies who controls risk transfer in an insurance arrangement, who captures the profit when claims come in under budget, and whether your dealership is positioned to benefit from that structure — or just funding someone else's business.

TL;DR

- A ceding company is the primary insurer that originates policies and transfers some or all associated risk to a reinsurer.

- The ceding company pays a reinsurance premium so the reinsurer covers a share of future claims.

- Even after ceding, the primary insurer remains fully liable to the policyholder — the reinsurer operates entirely behind the scenes.

- In auto dealer F&I, the third-party provider typically controls premium flow and keeps the underwriting profit your customers generate.

- Dealer-owned reinsurance programs let you capture those profits instead.

What Is a Ceding Company?

A ceding company is the primary insurance company that originates policies and then transfers — or "cedes" — some or all of the associated risk to a reinsurer through a reinsurance agreement.

The NAIC defines it simply as the insurer that "transfers risk by purchasing reinsurance." The Reinsurance Association of America goes a step further, describing the cedent as "the issuer of an insurance contract that contractually obtains an indemnification for all or a designated portion of the risk from one or more reinsurers."

Terminology Worth Knowing

The industry uses several terms interchangeably for this same party:

- Ceding company — the most common formal term

- Cedent — shorthand used by reinsurance professionals

- Primary insurer — emphasizes the company's direct relationship with policyholders

- Direct writer — common in property and casualty contexts

All four refer to the same role: the insurer that issued the original policy and is transferring risk downstream.

How Liability Works After Ceding

A point worth clarifying: ceding risk does not transfer the obligation to the policyholder. The ceding company remains directly responsible to its insured, regardless of any reinsurance arrangement behind the scenes.

Under standard reinsurance law, the primary insurer's liability to its policyholders is not discharged by the reinsurance agreement. The policyholder has no contractual relationship with the reinsurer and cannot make a claim against it directly.

A straightforward example: if an insurer writes a $1 million property policy and cedes 50% of the risk to a reinsurer, both parties share premiums and losses proportionally. But if the reinsurer fails to pay its share of a claim, the ceding company still owes the full claim amount to its policyholder.

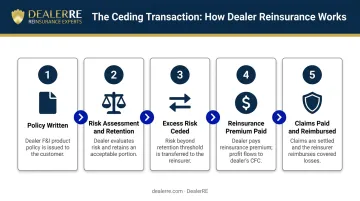

How the Ceding Process Works

The ceding transaction follows a logical sequence:

- The primary insurer writes a policy and collects premium from the policyholder.

- Risk assessment — the insurer evaluates total exposure and determines its retention limit (the maximum risk it will keep for its own account).

- The excess is ceded — risk above the retention limit is transferred to a reinsurer under either a treaty or facultative arrangement.

- A reinsurance premium is paid — carved from the original policyholder premium, this is what the reinsurer receives in exchange for assuming ceded risk.

- Claims are paid by the ceding company first — when a covered loss occurs, the primary insurer pays the policyholder directly, then seeks reimbursement from the reinsurer for its proportionate share.

The Retention Limit

The retention limit is the amount of risk the ceding company keeps for itself on any single policy or loss event. Anything above that threshold gets ceded. A company with a $500,000 retention limit on auto service contracts covers the first $500,000 in losses on any given contract and cedes everything above that to its reinsurer.

Reinsurance makes this practical: the ceding company retains only what its capital base can absorb and transfers the rest. That balance is what keeps the arrangement sustainable.

Where the Policyholder Fits

That behind-the-scenes structure extends to the policyholder relationship as well. The policyholder deals exclusively with the ceding company. Per the NAIC, "the reinsurer's obligation under a reinsurance agreement arises only when the ceding company's liability under its original insurance policy has been incurred." The reinsurer operates entirely behind the scenes.

Types of Reinsurance Arrangements for Ceding Companies

Ceding companies use two structural categories of reinsurance, and most programs layer both.

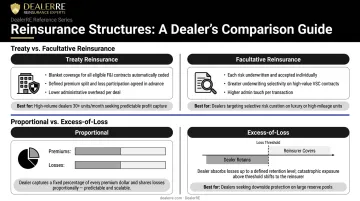

Treaty vs. Facultative

| Type | How It Works | Best For |

|---|---|---|

| Treaty | Reinsurer automatically accepts all policies within an agreed category (e.g., all VSCs written by a primary insurer) | Routine, high-volume business |

| Facultative | Reinsurer evaluates and individually accepts or rejects specific risks | High-value or unusual individual policies |

In dealer F&I contexts, treaty reinsurance is the standard structure. It lets a reinsurance program cover an entire book of service contracts without case-by-case negotiation — which is what makes volume-based programs operationally practical.

Proportional vs. Excess-of-Loss

| Structure | How It Works | Dealer Context |

|---|---|---|

| Proportional (pro rata) | Ceding company and reinsurer split both premiums and losses at a fixed ratio. In a 70/30 quota share, each party takes that same percentage of both income and claims. | Common in dealer-owned programs where the dealer entity participates directly in underwriting results |

| Excess-of-loss | Ceding company absorbs all losses up to a defined dollar threshold. The reinsurer covers losses that exceed that amount. | Protects the dealer's program from catastrophic claim events while keeping routine loss retention in-house |