Dealer reinsurance changes that equation. It's the structure that lets you own a piece of the insurance business you're already funding — capturing the underwriting profits, controlling the claims experience, and building a separate financial asset alongside your dealership. Many dealers treat it as a fifth business unit. The ones who've done it longest often say it's their best one.

This guide covers what dealer reinsurance is, how it works step by step, its key benefits, the main structure types available, and what to look for in a partner.

TL;DR

- Dealer reinsurance lets you own a captive company that keeps F&I underwriting profits for yourself instead of sending them to a third party

- Eligible products include VSCs, GAP, tire and wheel, dent/appearance, windshield, and BHPH-specific coverages like DCC and CPI

- Core benefits include higher profitability, customer experience control, tax advantages, and long-term wealth building

- Three main structures exist — CFC, DOWC, and NCFC — each with different tax treatment and investment flexibility

- Choosing a full-service partner for compliance, filings, training, and claims administration is critical to program success

What Is Dealer Reinsurance?

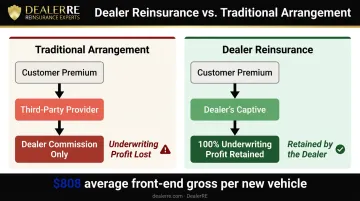

Dealer reinsurance is a financial structure where you create a separate entity — a reinsurance company you own — to retain the underwriting risk and profits on F&I products sold at your dealership. Instead of a third-party provider collecting the spread between what your customer pays and what claims actually cost, that profit flows into your company.

The Admin Obligor Model

The structure best suited for dealers who want full ownership of their profits is the admin obligor model. Your reinsurance company is backed by an A-rated insurer, keeping the program properly insured and compliant while you capture the underwriting profits. This is what separates a true dealer-owned reinsurance program from a basic profit-sharing arrangement — with profit sharing, you get a cut; with admin obligor, you own the entity receiving the profits.

DealerRE has operated on this model since 1994, helping dealers establish and manage their own administrator obligor reinsurance companies as an alternative to relying on third-party and manufacturer F&I products.

What Products Can Be Reinsured?

Once your structure is in place, product selection determines where the profit opportunity is largest. Most standard F&I products are eligible, including:

- Vehicle Service Contracts (VSCs) — the highest-volume reinsurance opportunity for most dealers

- GAP Insurance — covers the shortfall between an insurance settlement and the remaining loan balance on total losses

- Tire & Wheel Protection — road hazard coverage with non-prorated benefits

- Door Ding / Dent Protection — paintless dent repair for minor cosmetic damage

- Windshield Repair — covers chip and crack repairs caused by road hazards

- Theft Protection — window etching and anti-theft labeling that reduces total loss exposure

- Debt Cancellation Coverage (DCC) — a BHPH-specific waiver covering total debt on total loss

- Collateral Protection Insurance (CPI) — force-placed insurance for BHPH portfolios where borrowers lapse coverage

Which products make sense depends on your sales volume, customer profile, and whether you operate a traditional retail or BHPH model.

Is It Complicated?

Less than most dealers expect. Programs domiciled offshore elect under IRC Section 953(d) to be taxed as U.S. domestic insurance companies, keeping the compliance framework straightforward. The IRS issued final micro-captive regulations in January 2025 that created a "Seller's Captive" exception — F&I reinsurance companies insuring at least 95% third-party risk (your customers) are not classified as listed transactions. With a qualified partner managing the filings, most dealers find day-to-day operations far simpler than anticipated.

How Dealer Reinsurance Works

The process follows a clear five-step flow from the moment a customer buys a product to the moment underwriting profit lands in your account.

Step 1 — Customer Purchase A buyer elects an F&I product at the time of vehicle purchase. They pay a premium. Your dealership processes the sale exactly as it normally would.

Step 2 — Premium Allocation The premium is split to cover administrative fees, third-party management costs, and reserves set aside for future claims. The net underwriting exposure (what remains after those allocations) is what gets ceded to your reinsurance entity.

Step 3 — Ceding to Your Captive Those allocated reserves move into an account your reinsurance company controls, held at a U.S. trust company. Despite offshore domicile options like the Turks & Caicos, no funds are sent offshore — everything stays in U.S. financial institutions. Domestic options like the Delaware Tribe of Indians domicile are also available for dealers preferring a stateside structure.

Step 4 — Claims Activity and Underwriting Profit As contracts age, claims are paid from reserves. When claims run lower than the premiums collected — and strong product selection is what drives that outcome — the remaining funds represent underwriting profit. That profit stays in your reinsurance entity, not a third party's.

Step 5 — Investment Income Between premium deposit and claims payout, those reserves can be invested. Once balance sheet cash exceeds 125% of unearned premiums, the ownership can deploy those funds more aggressively. This investment income compounds on top of underwriting profit — a second layer of return most dealers never capture through third-party arrangements.

Key Benefits of Dealer Reinsurance

Enhanced Profitability

F&I gross profit represents roughly 25% of total dealership gross profit for publicly owned dealer groups, with national averages running $1,700–$1,900 per vehicle retailed across franchise stores. Under a traditional arrangement, the dealer earns a commission — the spread between retail and the administrator's cost. The underwriting profit (what's left after claims) stays with the provider.

With reinsurance, your captive captures 100% of that underwriting profit. Dealers working with DealerRE have realized hundreds of thousands of dollars in underwriting profit that they didn't know was available to them. That money was always being generated by your customer base. It was simply flowing to someone else.

Control Over the Customer Experience

When a third party handles claims, your customer's experience is out of your hands. A denied claim or a slow resolution reflects on your dealership even though you had no involvement in the decision. With a dealer-owned reinsurance company, you influence how claims are adjudicated — ensuring the customer experience stays consistent with what your store stands for.

Customers who see a claim resolved quickly and fairly are far more likely to return for their next vehicle — and refer others.

That's a direct connection between claims management and long-term revenue, which makes control over this process more than an operational preference. It's a competitive advantage.

Income Diversification and Financial Resilience

Reinsurance income isn't tied to this month's sales floor. It accumulates on a long-tail basis from previously sold contracts — so when vehicle sales slow down, reinsurance income keeps flowing. F&I performance demonstrated this during the pandemic: F&I PVR hit an all-time high of $2,603 in Q3 2022 even as inventory shrank. Reinsurance earnings follow that same countercyclical dynamic.

Tax Advantages

Properly structured reinsurance programs let dealers accumulate wealth more efficiently than taking ordinary distributions and paying income tax immediately. Programs domiciled in tax-advantaged jurisdictions amplify that effect further.

Programs structured under IRC Section 831(b) allow qualifying small insurance companies to be taxed only on investment income rather than underwriting income, provided annual written premiums don't exceed $1.2 million.

Tax treatment varies based on structure and individual circumstances. Consult a qualified tax advisor before making decisions based on tax benefits.

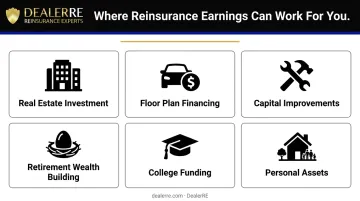

Wealth Building and Reinvestment Flexibility

Earnings accumulated in your reinsurance entity aren't locked up. Dealers use those funds for:

- Real estate investment

- Floor plan financing and working capital

- Dealership capital improvements

- Retirement wealth building

- College funding for their children

- Personal asset and lifestyle purchases

This creates a flexible long-term financial asset that exists independently of the dealership itself — a meaningful distinction when it comes to succession planning or a future buy-sell transaction.

Types of Dealer Reinsurance Structures

Three primary structures exist for dealer-owned reinsurance, and choosing the right one affects your tax strategy, investment control, and how much risk you carry. Here's how each one works.

Controlled Foreign Corporation (CFC)

The most common and flexible option. A CFC is domiciled offshore — typically in the Turks & Caicos — but elects under IRC 953(d) to be taxed as a U.S. domestic insurance company. The Turks & Caicos has hosted over 2,700 restricted-license reinsurers and built its regulatory framework specifically for this purpose.

Key features:

- Dealer maintains full control over investments held at U.S. financial institutions

- Can borrow against the account balance

- Operates as a personal book of business for the dealer principal

- No funds actually sent offshore — reserves stay in U.S. trust accounts

Best for: dealers wanting maximum investment flexibility and full control over their captive.

Dealer-Owned Warranty Company (DOWC)

A domestic structure where the dealer or dealer group owns an administrative corporation that acts as the obligor on the contracts. Treated as an insurance company for tax purposes, it keeps everything within U.S. regulatory frameworks.

Key features:

- Domestic setup within U.S. regulatory framework

- Dealer retains 100% of underwriting profit and investment income

- Allows product customization tied directly to the dealership

- No offshore components

Best for: dealers who prefer a purely domestic structure or dealer groups with more complex multi-state operations.

Non-Controlled Foreign Corporation (NCFC)

The most conservative option. An NCFC requires a minimum of 11 unaffiliated U.S. shareholders; no single owner controls the entity. The structure returns underwriting profits as dividends rather than retaining them in full.

Key features:

- Lower risk exposure than a fully controlled structure

- Subject to a 1% federal excise tax on premiums

- Less investment flexibility than a CFC

- Income is not classified as Subpart F income — shareholders are taxed only when distributions occur

Best for: risk-averse dealers who want some participation in underwriting profits without full ownership responsibility.

What to Look for in a Reinsurance Partner

Choosing the right structure is only half the equation. The partner managing that structure determines whether it actually performs.

Full-Service Administration

A reinsurance partner should handle all of the following — not just set up the structure and leave:

- Legal forms, filings, and renewals

- Compliance management across jurisdictions

- Tax returns and regulatory reporting

- Claims adjudication

- Monthly financial statements and performance reporting

- Accounting records and annual report preparation

Dealers who are left to manage these details independently often fall out of compliance or underperform on profitability. DealerRE manages every one of these components on behalf of their dealer clients, with no hidden additional fees.

F&I Training and Ongoing Support

Strong back-office administration keeps the program legal and organized — but the revenue comes from the F&I desk. Look for a partner that provides:

- In-person and online F&I training classes

- F&I menu support and development

- Ongoing dealer development and performance reviews

DealerRE offers both online (via their training platform) and in-person F&I training as part of their full-service model. Dealers who combine strong program administration with consistent F&I training tend to see measurably better product penetration and per-deal income.

Track Record and Dealer-First Alignment

Ask how long the company has been in business, how many dealers they've helped, and — critically — whether their business model only works when yours does.

DealerRE was founded in 1994 by Tim Byrd in Southeast Virginia and has since helped more than 400 auto dealers build profitable reinsurance programs. Their client roster includes National Quality Dealers of the Year, NIADA Board Members, and multiple state association presidents. The company's stated principle: "We only succeed if you do."

Frequently Asked Questions

What is dealer reinsurance and how does it work?

Dealer reinsurance allows a dealership to own a captive company that retains underwriting profits from F&I products — rather than sending those profits to a third-party provider. The dealer controls reserves held in U.S. trust accounts, directs claims handling, and captures investment income earned while funds are held.

What F&I products can be included in a dealer reinsurance program?

Common eligible products include vehicle service contracts, GAP insurance, tire and wheel protection, dent repair, windshield coverage, and appearance products. BHPH dealers can also reinsure Debt Cancellation Coverage (DCC) and Collateral Protection Insurance (CPI).

What is the difference between a CFC and a Dealer-Owned Warranty Company (DOWC)?

A CFC is an offshore structure domiciled in a jurisdiction like the Turks & Caicos, offering maximum investment flexibility while electing U.S. tax treatment under IRC 953(d). A DOWC is a domestic structure where the dealer acts as the direct obligor on contracts — each carries different tax treatment and compliance requirements.

Is dealer reinsurance right for smaller or independent dealerships?

Yes, though higher-volume stores see the strongest economics. Independent and BHPH dealers selling more than 30 vehicles per month can benefit — particularly with a partner who sizes the program appropriately and structures BHPH premiums to be financed over the contract term rather than paid upfront, protecting cash flow.

How long does it take to set up a dealer reinsurance program?

With a full-service partner managing filings and compliance, most programs are established within a few weeks to a couple of months. The Turks & Caicos licensing process, for example, takes approximately 30 days.

What should Southeast auto dealers look for in a reinsurance partner?

Prioritize full-service administration, F&I training support, transparent fee structures, and a proven track record with both independent and franchise dealers. Look for a partner who manages compliance, tax filings, and renewals on your behalf — and whose success depends on yours, not just on setup fees.