Extra-contractual obligations, or ECO, represent one of the least understood but most consequential of those exposures. A single bad faith claim or regulatory enforcement action can generate damages that dwarf the original policy payout — and without the right treaty language, the ceding insurer absorbs all of it.

This article covers what ECO is, how it differs from Excess of Policy Limits (XPL), what triggers an ECO claim, how ECO clauses are structured in reinsurance treaties, and why all of this matters specifically for dealers running their own reinsurance programs.

TL;DR

- ECO = damages imposed on an insurer for its own conduct (bad faith, negligence, deception) — not the underlying covered loss

- XPL covers damages exceeding policy limits when claims are mishandled — and often surfaces alongside ECO claims

- ECO coverage is not automatic — it must be explicitly negotiated into a reinsurance treaty

- Most ECO clauses exclude losses from intentional fraud by directors or officers

- Dealer ECO exposure most commonly arises from claims adjudication practices and point-of-sale misrepresentation

What Are Extra-Contractual Obligations in Reinsurance?

Extra-contractual obligations are liabilities that fall outside the insurance policy itself. They don't arise from the covered peril; they arise from how the insurer behaved.

Investopedia defines ECO as "expenses imposed upon the ceding insurer by regulatory, judicial, or governmental organizations." IRMI reinforces this: ECO losses stem from "the insurer's handling of claims," not the underlying policy terms.

The Punitive Nature of ECO Damages

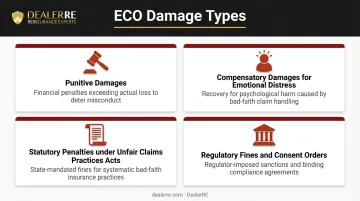

ECO damages are designed to punish insurer misconduct. They can include:

- Punitive damages awarded by courts (in states where they're insurable)

- Compensatory damages for emotional distress caused by claims mishandling

- Statutory penalties under state Unfair Claims Practices Acts

- Regulatory fines and consent order penalties from state insurance departments

These are fundamentally different from a standard claim payout. A normal claim settlement pays what the policy promised. An ECO award punishes the insurer for acting badly in the process.

The Reinsurer's Role

When a reinsurance treaty includes an ECO clause, the reinsurer agrees to share in these penalties alongside the ceding insurer. Without that clause, the ceding insurer absorbs 100% of ECO damages — no matter how large.

A practical example: An insurer misrepresents what perils a VSC covers during the sales process. The policyholder files a claim, gets denied, and sues for bad faith.

The court awards $200,000: $50,000 for the original claim and $150,000 in punitive damages for the insurer's conduct. That $150,000 is the ECO exposure. If the treaty doesn't include an ECO clause, it belongs entirely to the ceding insurer.

ECO clauses are not automatic — they must be specifically negotiated into the treaty. Without explicit ECO language, standard "follow the fortunes" provisions typically won't cover bad faith damages.

ECO vs. Excess of Policy Limits (XPL): Understanding the Difference

Treaty language often bundles these two as "ECO/XPL," but that shorthand obscures an important distinction: they're triggered by different events and carry different legal weight for your reinsurance program.

What Is XPL?

Excess of Policy Limits losses arise when an insurer mishandles a claim — typically by failing to settle within policy limits when it had the opportunity — and a judgment then exceeds the stated coverage amount. The insurer becomes liable for the amount above the limit.

For example: A policy has a $100,000 limit. The plaintiff offered to settle for $80,000. The insurer refused. The jury awards $250,000. The insurer now owes $150,000 above the policy limit. That's XPL exposure.

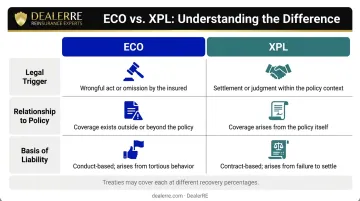

The Key Distinction

| Dimension | ECO | XPL |

|---|---|---|

| Legal trigger | Insurer's bad faith, negligence, or deception | Failure to settle a covered claim within policy limits |

| Relationship to policy | Falls entirely outside the policy | Would have been covered, but exceeds the limit |

| Basis of liability | Tort-based (insurer's wrongful acts) | Contract-based (failure to protect insured) |

ECO damages exist because the insurer acted badly, independent of the underlying claim. XPL damages exist because an otherwise covered claim exceeded its limit due to mishandling.

In practice, a reinsurance treaty may cover XPL at 100% and ECO at a lower percentage — say 80% — because ECO liability stems from the insurer's own conduct, which carriers treat as a less predictable risk. When reviewing your treaty, confirm which exposures are covered and at what recovery rate — those details directly affect how much protection your reinsurance program actually provides.

When ECO Claims Get Triggered

Bad Faith

Bad faith is the most common ECO trigger. Courts generally require two elements: (1) the insurer lacked a reasonable basis for denying benefits, and (2) the insurer knew or recklessly disregarded that lack of reasonable basis.

Common bad faith violations include:

- Unreasonable denial of a valid claim

- Failure to investigate promptly and thoroughly

- Deliberate underpayment without adequate explanation

- Ignoring policyholder communications

Negligence and Deceptive Practices

An insurer doesn't need to act deliberately to face ECO exposure. Negligent claims handling — even without malicious intent — can still produce court-imposed penalties. When an insurer (or someone acting on its behalf) misrepresents what a policy covers, either at sale or during the claims process, that deception creates its own ECO trigger.

This is especially relevant for F&I products, where the sales process is tightly connected to policy terms. The FTC's enforcement against CarShield illustrates the pattern: the agency sent $9.6 million in consumer refunds after finding CarShield had deceptively marketed VSCs and failed to provide promised coverage to 168,179 customers.

Regulatory Penalties

ECO exposure doesn't require a courtroom verdict. Regulatory bodies can impose fines, consent orders, and restitution obligations that qualify as ECO-type losses. In March 2026, the FTC warned 97 auto dealership groups about deceptive pricing practices, signaling that regulatory ECO exposure is growing for dealer-adjacent operations.

Date of Loss Assignment

One technical detail with real consequences: in treaty contexts, ECO losses are typically dated to the original underlying occurrence, not the date of the bad faith verdict or regulatory penalty. This means an enforcement action in 2025 might attach to a treaty period from 2022 — complicating which coverage responds.

How ECO Clauses Are Written Into Reinsurance Treaties

What ECO Clauses Typically Cover

A standard ECO clause provides that the reinsurer will reimburse the ceding insurer for payments arising from claim handling that fall outside the original policy terms. The BRMA sample language covers "liabilities not covered under any other provision of this Agreement" arising from handling of any claim, "including but not limited to bad faith."

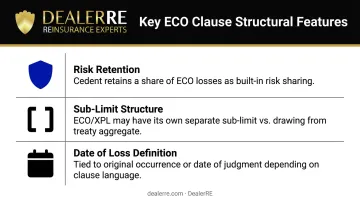

Key structural features to look for in any ECO clause:

- Cedents typically retain a share of ECO losses rather than recovering 100%, functioning as a built-in risk-sharing mechanism

- Some treaties assign ECO/XPL its own separate sub-limit rather than drawing from the treaty aggregate

- Date of loss definitions vary: some clauses tie losses to the original occurrence; others use the date of judgment

The Fraud Exclusion

Most ECO clauses exclude losses resulting from the fraud, criminal acts, or malicious intent of the reinsured's directors or officers. The logic: reinsurers aren't obligated to indemnify intentional wrongdoing at the governance level. For dealer-program operators, officer-level fraud eliminates treaty protection entirely. Don't assume the reinsurance will respond until you've confirmed the conduct falls outside this exclusion.

Treaty Limit Exhaustion Risk

Large contractual claim losses can exhaust the treaty aggregate before ECO coverage has a chance to respond. If a catastrophic underlying loss consumes the full treaty limit, there's nothing left to cover a subsequent bad faith judgment.

Simple illustration: A treaty has a $500,000 aggregate. A series of large VSC claims pays out $490,000. A bad faith lawsuit then produces a $100,000 ECO award. The treaty has $10,000 remaining — leaving the ceding insurer to absorb the $90,000 shortfall.

Dealers should evaluate whether ECO/XPL protection carries a separate sub-limit or shares the treaty aggregate.

What ECO Clauses Do NOT Cover

ECO coverage is limited to claim-handling conduct. It does not extend to:

- Underwriting decisions

- Actuarial errors or mispricing

- Loss control activities

- Premium financing decisions

- Point-of-sale misrepresentation (in many treaty formulations)

When those excluded categories create liability, a treaty ECO clause won't respond. Insurance Company Professional Liability (ICPL) policies fill that gap, functioning as standalone E&O coverage for insurance companies and covering a wider range of professional conduct than any treaty-level ECO provision.

Why ECO Matters for Dealer-Owned Reinsurance Programs

When a dealer establishes their own reinsurance company through an admin obligor structure, they step into the reinsurance chain. The fronting carrier remains the direct insurer of record, but the dealer's reinsurance entity bears the financial risk — and is subject to the same regulatory and fiduciary standards that govern any reinsurer.

Where ECO Exposure Concentrates

For dealer-owned programs, ECO exposure tends to cluster in two areas:

Claims adjudication: How VSC claims are handled matters legally, not just operationally. Denials need to be properly communicated. Investigations need to be conducted. Underpayments need to be justified. Poor claims processes — even unintentional ones — create bad faith exposure.

Point-of-sale representation: If coverage terms were misrepresented when the VSC was sold, that's a potential ECO trigger. The enforcement actions against U.S. Fidelis (whose owners were permanently barred from VSC sales across 11 states after deceiving over 400,000 consumers) and CarShield both originated in how products were marketed and explained — not just how claims were paid.

How Structured Administration Reduces Exposure

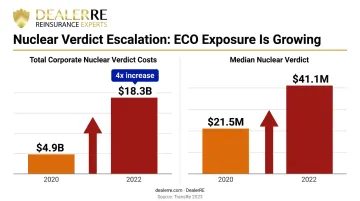

The TransRe research on nuclear verdicts shows how fast ECO exposure is escalating: total corporate nuclear verdict costs quadrupled from $4.9 billion in 2020 to $18.3 billion in 2022, with the median nuclear verdict rising from $21.5 million to $41.1 million. ECO exposure is financially escalating across all insurance lines — including VSC programs.

That context makes structured program administration a direct risk management decision. DealerRE handles the operational elements that prevent ECO exposure from compounding:

- Legal forms, filings, and regulatory renewals

- Tax returns and compliance oversight

- Claims adjudication through administrative partner AVP

- Performance reporting across every program they administer

Their stated commitment is that they "do not cut any corners to expose you as a client to compliance or tax risk." Consistent claims handling, accurate coverage representation, and current regulatory filings are what separate a well-managed program from one that becomes a liability.

Frequently Asked Questions

What is XPL and ECO coverage in reinsurance?

XPL (Excess of Policy Limits) covers losses when claims mishandling causes a judgment to exceed the policy limit. ECO (Extra-Contractual Obligations) covers penalties imposed on an insurer for bad faith, negligence, or deceptive conduct. Both can be included in a reinsurance treaty as separate exposures with different legal triggers.

What is the difference between ECO and XPL in reinsurance?

ECO is triggered by insurer behavior — bad faith, misrepresentation, or negligence — regardless of the underlying claim outcome. XPL is triggered specifically when procedural mishandling of a covered claim results in a judgment that exceeds the policy limit. Reinsurers typically pair them as "ECO/XPL" in treaty language.

What triggers an ECO claim in reinsurance?

The main triggers are: bad faith denial or underpayment of a valid claim, negligent claims handling, misrepresentation of policy coverage terms, and regulatory penalties imposed for compliance failures.

Are ECO claims automatically covered in a reinsurance treaty?

No. ECO coverage must be explicitly negotiated into the treaty through a specific ECO clause. Without that language, the ceding insurer bears 100% of extra-contractual damages. The scope of coverage — including any fraud exclusions or percentage recovery limits — depends entirely on the negotiated treaty terms.

How does an ECO clause protect a ceding insurer?

An ECO clause shifts some or all of the financial burden of extra-contractual penalties to the reinsurer. This means the ceding insurer doesn't absorb 100% of court-awarded damages or regulatory fines from covered conduct. The reinsurer's share depends on the recovery percentage and sub-limits specified in the clause.

How can a dealer running their own reinsurance company reduce ECO exposure?

The core protective measures are:

- Handle claims consistently and in good faith, with clear denial communications

- Represent coverage terms accurately at the point of sale

- Partner with an experienced program administrator who manages compliance, legal filings, and claims adjudication

Operational discipline is the most effective ECO prevention available.