Introduction

F&I is the last major dealership function still largely anchored to a physical office visit — and that gap is becoming a liability. According to Cox Automotive's 2024 Car Buyer Journey Study, 83% of car buyers want to complete at least one step of the purchase process online, yet the F&I conversation still happens almost exclusively in person at most dealerships.

For franchise dealers, independent dealers, and BHPH operators, this creates a real problem. Buyers are researching financing options, comparing products, and in some cases submitting credit applications before they ever walk through the door. Dealers without a digital F&I pathway are entering that conversation after buyers have already formed opinions, compared alternatives, and in some cases moved on entirely.

What follows is a practical breakdown of how to build an online F&I process that holds up on product penetration, compliance, and customer experience — without gutting the finance office that makes it work.

TL;DR

- An online F&I process lets dealers present financing, product menus, and contracts to customers remotely — via video, digital menus, and e-signature tools.

- 83% of buyers want at least one purchase step online; dealers without a digital F&I path leave those buyers underserved.

- Building it requires five sequential steps: process audit, technology selection, menu development, compliance workflow, and remote delivery training.

- Structured menus, clear product presentations, and documented declines still drive performance online — the principles are the same, but delivery is video-first.

- Dealers using dealer-administered VSCs and GAP through reinsurance close remote deals more profitably — lower product costs mean more flexibility on price without sacrificing margin.

What Is an Online F&I Process?

An online F&I process is a documented, repeatable sequence that allows a dealership's finance and insurance function to operate digitally: pre-qualification, product education, menu presentation, deal structuring, and contract execution — all handled without the customer sitting in the F&I office.

It replicates every revenue-generating function of traditional F&I — arranging financing, presenting and closing products, and finalizing deal paperwork — in a different environment.

What It Is Not

This distinction matters: an online F&I process is not simply listing products on a webpage. There's a meaningful difference between:

- Passive digital presence: product descriptions buried in a website footer, a generic financing page, or a "contact us for details" CTA

- Active online F&I process: a structured sequence with defined steps, assigned responsibilities, digital tools, and measurable outcomes

A dealer who uploads a PDF of their menu and calls that "online F&I" will see exactly the results that approach deserves. A true online process gives the customer a defined experience from credit inquiry through signed contract, with every step tracked and documented.

The goal is a process that functions consistently, produces the same revenue outcomes, and creates the documentation a compliant dealership requires — whether the customer is across town or across the country.

Why Auto Dealers Are Moving F&I Online

The consumer behavior data here is unambiguous. Cox Automotive's "F&I for an Ecommerce Future" report found that 71% of car shoppers want to see specific F&I product pricing online before visiting a dealership — and 76% say they're open to completing the purchase entirely online.

These numbers reflect what the majority of buyers now expect before they walk through the door.

What Happens When F&I Doesn't Meet Buyers Where They Are

Dealers without an online F&I pathway experience several compounding problems:

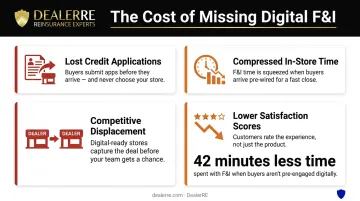

- Lost credit applications — buyers submit online pre-approvals through lenders or competitors when the dealership doesn't offer a clear digital pathway

- Compressed in-store time — buyers who've already spent time researching resist a lengthy F&I office visit, reducing product presentation time and acceptance rates

- Competitive displacement — with nearly half of buyers visiting only one dealership before purchasing, first contact with a digitally capable competitor often ends the opportunity

- Lower satisfaction scores — Cox Automotive's data shows that buyers who complete key steps online spend 42 minutes less at the dealership, and that efficiency gain directly correlates with satisfaction and repurchase intent

The Regulatory Dimension

The operational case for online F&I is clear — but the compliance case is equally compelling. The FTC's CARS Rule was vacated in January 2025, yet the FTC has continued enforcement under existing authority. In March 2026, it sent warning letters to 97 dealership groups regarding deceptive pricing practices.

Digital F&I processes, when built correctly, create auditable records of every product presentation and customer decision. That documentation trail protects dealers operationally and serves as a concrete compliance asset during any regulatory review.

How to Set Up Your Online F&I Process

Setting up an online F&I process requires a structured sequence of five steps — each one depends on the previous being completed correctly before moving forward.

Step 1: Audit and Document Your Current F&I Process

Before moving anything online, map your existing in-store process end-to-end. Document:

- What happens from the moment a sale is agreed to through the final signed contract

- Who does what at each step

- Which products are presented, in what order

- How customer decisions — acceptances and declines — are currently recorded

Gaps in your in-store process don't disappear online — they get worse. Any workflow that relies on informal handoffs, unwritten steps, or manager discretion will produce wildly inconsistent results in a remote environment. Fix the gaps before you digitize anything.

DealerRE's onboarding process includes a business analysis component specifically designed to surface these gaps — reviewing product mix, sales performance, and process structure before any program changes are implemented.

Step 2: Select Your Digital Tools and Technology Stack

Online F&I requires a minimum set of integrated tools. Evaluate each category on the criteria below — not on vendor brand names:

| Tool Category | Core Function | What to Evaluate |

|---|---|---|

| Video conferencing platform | Live remote F&I presentations | Screen sharing, recording capability |

| Digital F&I menu software | Product presentation and menu delivery | Shareable links, payment impact display |

| E-signature solution | Remote contract execution | ESIGN Act compliance, consumer consent workflow |

| CRM integration | Lead capture and follow-up | Speed-to-lead tracking, automated notifications |

| Identity verification | Remote ID authentication | Red Flags Rule compliance, fraud prevention |

The technology is the easy part. Building a documented, repeatable process around it is where most dealers fall short — investing in tools before standardizing workflow produces expensive software with inconsistent outcomes.

Step 3: Build Your Online F&I Menu and Product Presentation

Your in-store menu needs meaningful adaptation for digital delivery. A menu that works when you're sitting across a desk from a customer doesn't automatically translate to a shared screen.

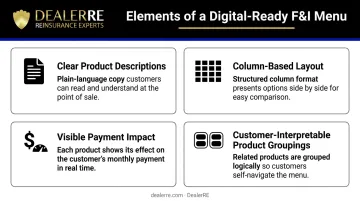

A digital-ready F&I menu should have:

- Clear product descriptions — plain language, not insurance jargon. Customers reading independently need to understand what they're buying without verbal explanation

- Column-based layout — four visible protection levels that remain readable as a PDF or shared screen

- Visible payment impact — each protection level should show both total cost and monthly payment change, calculated against the actual deal structure

- Product groupings customers can interpret — grouping VSC, tire & wheel, and appearance protection together helps buyers evaluate options without needing line-by-line explanation

The products offered online can be exactly what you offer in-store. Dealer-administered vehicle service contracts, GAP, tire & wheel, debt cancellation, and ancillary products like door ding and windshield repair all translate to remote delivery. DealerRE provides F&I menu development and training support to help dealers build menus structured for both in-person and remote presentation.

Step 4: Establish Your Compliance and E-Signature Workflow

Online F&I is legally sound. The federal ESIGN Act gives electronic contracts and signatures the same standing as paper, and most states have adopted the Uniform Electronic Transactions Act to align at the state level. New York is a notable exception and requires state-specific legal review.

What dealers frequently get wrong:

- Skipping affirmative consumer consent — buyers must explicitly agree to conduct the transaction electronically before any documents are signed

- Incomplete decline documentation — every product presented must have a signed acceptance or decline on file, just as in-store

- Inadequate record retention — electronic F&I documents must be accurate, accessible, and reproducible; a folder of PDF attachments in an email thread is not a records management system

- Remote identity verification — Red Flags Rule compliance doesn't stop because the customer isn't physically present

Compliance failures in this step create regulatory exposure that no gain in product penetration can offset. Get legal review for your e-signature workflow and records retention policy before your first remote deal closes.

Step 5: Train Your F&I Team for Remote Delivery

This is where most online F&I initiatives stall. An F&I manager who performs well in person will not automatically perform well on screen. The skills don't transfer automatically.

Remote F&I training needs to cover:

- On-screen menu navigation — sharing the menu confidently, walking through columns without losing the customer's attention

- Pacing adjustments — remote customers lose interest faster than in-person buyers; presentations need to be tighter and more structured

- Digital objection handling — the same principles apply (acknowledge, connect to stated needs, don't stack rebuttals), but the pacing must account for the absence of physical presence

- Structured needs assessment — asking how long the customer keeps vehicles, typical mileage, and primary concerns before presenting the menu; this can't be skipped because the conversation is remote

- Engagement maintenance — without body language and physical proximity, eye contact with the camera and deliberate verbal check-ins carry more weight

DealerRE's F&I training programs cover both in-person and remote delivery, giving your team the specific skills each channel requires.

Key Elements That Make or Break an Online F&I Process

Getting the five steps right builds the infrastructure. These execution details determine whether it actually produces results.

Start Before the F&I Conversation

The online F&I process should begin on your website, well before any customer interaction with your finance office. Publish:

- Available financing sources and approximate rate ranges

- F&I product descriptions in plain language

- A clear pre-approval or credit inquiry pathway

Buyers who encounter F&I products for the first time during the remote closing conversation are less likely to accept them. Buyers who've already read about VSC coverage and GAP protection arrive at the menu presentation informed and far more receptive.

Respond to Digital Leads Immediately

Those website-primed leads only convert if your team follows up fast. Lead response speed directly affects whether a digital F&I interaction ever happens at all. Research from MIT and the Kellogg School of Management found that a lead contacted within 5 minutes is 21 times more likely to enter the sales cycle than one contacted after 30 minutes. The average dealer response time to an online lead is approximately 42 hours.

In an online F&I process, delayed follow-up between a digital credit application and the F&I conversation doesn't just reduce satisfaction — it kills deals. Buyers who don't hear back quickly submit their application somewhere else.

Document Everything

Every online F&I interaction must produce a complete digital record of:

- Which products were presented

- Which were accepted (with signed agreement)

- Which were explicitly declined (with signed decline)

- When each interaction occurred (timestamp and channel)

This documentation protects the dealership in a regulatory review and establishes accountability equivalent to a well-run in-store process. Without it, the online process is both operationally inconsistent and legally exposed.

Common Mistakes Dealers Make When Going Online With F&I

Three mistakes consistently derail dealers when they move F&I online:

1. Assuming in-store techniques carry over. Long verbal explanations, physical paperwork handoffs, and body language cues don't work on a screen. The remote process needs to be simpler and more structured — not the same routine delivered over video.

2. Buying technology before documenting process. Dealers who purchase a digital menu tool or e-signature platform before documenting their F&I workflow end up with expensive tools producing inconsistent results. Technology is only as effective as the process supporting it.

3. Presenting products that don't explain themselves. Some F&I products were designed for high-pressure, in-person closing environments. Online, customers can exit the conversation instantly. Products with clear, transparent, customer-value-focused descriptions close more reliably in a remote setting. Dealer-administered products — where the dealer controls coverage terms and the claims experience — give the F&I manager something concrete to present without relying on pressure tactics.

Frequently Asked Questions

What technology do you need to run an online F&I process?

The core stack is four tools: a video or virtual meeting platform, digital F&I menu software, an ESIGN-compliant e-signature solution, and a CRM that captures online interactions. The technology is straightforward — the process built around it determines whether it actually produces results.

Is it legal to present and sign F&I documents online?

Yes. The federal ESIGN Act establishes that electronic contracts and signatures carry the same legal validity as paper. Dealers must obtain affirmative consumer consent to transact digitally and maintain accurate, accessible records. Most states align through the Uniform Electronic Transactions Act, though New York has not adopted UETA and warrants separate legal review before going fully digital.

Can online F&I achieve the same product penetration as in-store F&I?

Yes, when the process is structured, the menu is clear, and the F&I manager is trained for remote delivery. Industry benchmarks place VSC penetration at 45–50% and products per deal at 1.3–1.7 — dealers running disciplined digital menus consistently reach those numbers.

How do you handle customer objections during a remote F&I presentation?

The core approach is the same as in-store: acknowledge the objection, connect your response to what the customer told you during the needs assessment, and don't stack rebuttals. Pacing is the critical remote adjustment. Long pauses and slow responses lose remote customers faster than in-person buyers.

What F&I products work best in an online or remote process?

Products with clear, easily explained value tend to close best remotely: vehicle service contracts, GAP, and maintenance plans. Dealer-administered products — where coverage terms are transparent and the dealer controls the claims experience — give F&I managers something straightforward to explain and close, without relying on high-pressure tactics that don't translate to a screen.

How do you train F&I managers to handle the online process effectively?

Start with role-play using live on-screen menu sharing, add timed presentation exercises to build delivery discipline, and include coaching on screen-specific skills: camera eye contact, pacing, and digital objection handling. Remote F&I delivery is a distinct skill set from in-store selling. Treating it as identical to standard training is the most common reason online F&I programs underperform.