Introduction

Most auto dealerships hand over underwriting profits to third-party F&I providers without realizing they can keep those profits themselves. Every time you sell a service contract, GAP policy, or ancillary protection product, a third party collects premiums, holds reserves, and earns investment income on funds your customers generated.

According to DealerRE's analysis, administrative fees typically account for just 20% of the total product cost — meaning 80%+ flows into premium reserves controlled entirely by the provider. Without your own reinsurance company, that money never comes back.

The good news: many dealerships already meet the volume threshold to qualify for a profit participation program. Getting there does require navigating decisions around legal structure, compliance, F&I product alignment, and partner selection — and each one directly affects how much you'll actually retain.

This guide covers whether your dealership qualifies, what's required before you start, the setup process step by step, what drives results once you're running, and the mistakes that most commonly limit returns.

Key Takeaways

- Profit participation programs let dealers capture underwriting profits currently kept by third-party warranty and insurance companies

- Dealerships selling as few as 10 service contracts per month can qualify, making this accessible to independents, BHPH operations, and franchise stores

- Setup involves choosing a structure (retro, CFC/PARC, or admin obligor), forming a compliant entity, aligning F&I products, and training staff

- Profitability hinges on claims ratio, product penetration, product mix, and sales consistency

- An experienced reinsurance partner handles administration, filings, and compliance so your team stays focused on selling

How to Set Up Profit Participation at Your Dealership

Step 1: Assess Your Dealership's Volume, Goals, and Readiness

Setup begins with an honest evaluation of your current monthly F&I product volume — not just vehicle sales. It's the premium generated by service contracts, GAP, and ancillary products that feeds the program, and a baseline of approximately 10 or more F&I product sales per month is generally sufficient to qualify for entry-level structures.

Identify your primary goals before choosing a structure:

- Short-term cash flow maximization – You want distributions now to reinvest in inventory, facility upgrades, or operating expenses

- Long-term wealth building – You're focused on accumulating a tax-advantaged asset over time, potentially for retirement or estate planning

These two goals lead to fundamentally different program choices. A retro commission structure delivers faster cash but is taxed as ordinary income, while a CFC/PARC program builds equity over time with favorable capital gains treatment upon distribution.

Step 2: Choose the Right Profit Participation Structure for Your Situation

The structure you select determines your tax treatment, cash flow timing, claims exposure, and long-term profitability. Here are the main options:

Retrospective Commission (Retro)

A profit-sharing arrangement where a third-party administrator returns a portion of underwriting profit after claims are paid. You don't own a separate entity. Distributions are issued via 1099 and taxed as ordinary income. This is the lowest-risk entry point but offers the least control and tax efficiency.

CFC/PARC Reinsurance

A Controlled Foreign Corporation (CFC) or Producer-Affiliated Reinsurance Company (PARC) is typically domiciled offshore and elects under IRC Section 953(d) to be taxed as a U.S. insurance company. PARC dividends are typically taxed at capital gains rates, making this structure ideal for long-term wealth building. The maximum annual premium limit is $2.85 million; exceeding this threshold triggers significant tax penalties.

NCFC (Non-Controlled Foreign Corporation)

U.S. shareholders cannot own or control 25% or more of voting rights. Typically requires at least 11 unrelated U.S. shareholders (each owning <10%). The entity is not subject to federal income taxes and typically pays a 1% federal excise tax on net written premium, making it suitable for larger dealer groups without premium caps.

Dealer-Owned Warranty Company (DOWC)

Under a DOWC, the dealer becomes the contractual obligor — directly responsible for honoring warranty claims. You retain 100% of underwriting profits and investment income.

This structure requires higher capitalization than reinsurance alternatives. You must also register as a service contract provider in each state where you operate, meeting state-specific licensing, reserve, and form-filing requirements.

Admin Obligor Reinsurance

In this structure, the third-party administrator or insurance carrier serves as the obligor to the customer, not the dealer. This insulates you from direct claims liability while preserving profit capture. The program is backed by A-rated carriers, meaning claims are supported by financially stable insurers with proven ability to meet obligations. This structure offers a balanced approach: strong profit retention without direct exposure to claims risk.

The right structure depends on:

- Monthly F&I product volume

- Risk tolerance

- Tax strategy

- Whether you want upfront cash flow or long-term asset accumulation

A qualified consultant should model these scenarios using your actual numbers before you commit to a structure.

Step 3: Form the Legal Entity and Establish Compliance

Forming the reinsurance entity requires selecting a domicile, filing articles of incorporation, meeting any state licensing requirements, and ensuring the structure matches IRS code for the program type chosen.

Domicile Options:

- Offshore: CFC programs are typically domiciled in offshore jurisdictions. The Cayman Islands is the second-largest captive insurance domicile in the world, with Turks and Caicos also popular for dealer reinsurance entities

- Domestic: Vermont is a leading U.S. captive insurance domicile for DOWC and domestic captive structures

Key Compliance Requirements:

- IRC Section 831(b): Allows a non-life insurance company to exclude underwriting gain or loss from taxable income, taxing only investment income. Net written premium must not exceed $2.3 million (adjusted annually for inflation)

- IRC Section 953(d): Allows a CFC to elect to be treated as a domestic insurance company

- IRS Notice 2016-66: Identifies certain micro-captive insurance arrangements as "transactions of interest." Requires disclosure filings by reinsurance companies, dealerships, shareholders, and potentially tax preparers. Penalty: $50,000 per nondisclosure, per entity, per year

Full-service reinsurance partners like DealerRE manage all legal forms, filings, tax returns, and annual renewals on behalf of the dealer — removing the administrative burden and compliance risk for dealerships without dedicated legal or finance teams.

Step 4: Align Your F&I Product Lineup to Feed the Program

The program only builds value when the right F&I products are consistently sold. Products must be A-rated and compatible with the reinsurance structure selected.

Eligible Products:

- Vehicle service contracts (VSCs)

- Guaranteed Asset Protection (GAP)

- Prepaid maintenance

- Ancillary protection products (tire & wheel, appearance protection, theft, windshield)

- BHPH-specific products: mechanical breakdown coverage, collateral protection insurance (CPI), debt cancellation coverage (DCC)

F&I menus, pricing strategy, and product penetration rates directly determine how much premium flows into your program each month. National service contract penetration is approximately 47%, while the top 5% of dealerships achieve approximately 84% penetration. This difference translates to a measurable gap in program value — often hundreds of thousands of dollars over the life of the program.

Step 5: Train Your F&I Team and Establish Performance Monitoring

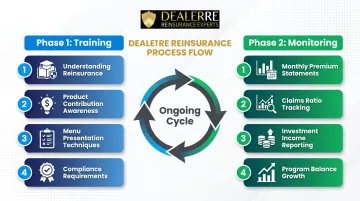

Staff training is not optional. F&I managers must understand what the program is, why product penetration matters beyond just commission, and how consistent presentations using a structured menu system convert to long-term dealer wealth.

Training should cover:

- What reinsurance is and how the dealer benefits

- How each product sold contributes to program growth

- Proper menu presentation techniques

- The connection between penetration rates and program profitability

- Compliance and documentation requirements

Ongoing performance monitoring includes:

- Monthly statements showing premiums ceded

- Claims ratio tracking

- Investment income reporting

- Program balance growth

These statements should be reviewed with a reinsurance advisor regularly — ideally monthly — to identify underperforming products, track claims trends, and keep the program on pace with your financial goals.

What You Need Before Starting Your Profit Participation Program

Preparation determines whether the program builds wealth or stalls. Dealers who skip this phase often end up in the wrong structure — or with a program that never earns out despite strong sales volume.

Minimum Volume and Product Mix Requirements

A baseline of approximately 10 or more F&I product sales per month (service contracts, ancillary products) is generally sufficient to qualify for a program. A consultant should review your current deal mix to confirm the product lineup is generating enough premium to make the program worthwhile.

According to Q1 2026 Presidio-NCM data, F&I income per retail unit averaged $1,727, up 7.1% from $1,613 in Q1 2025. Independent dealers typically target approximately $1,100 profit per retail unit for their F&I departments, according to NIADA benchmarks.

Compliance and Licensing Readiness

Once your volume qualifies, the next step is confirming you can legally and operationally launch. Before moving forward, verify:

- State licensing requirements relevant to the chosen structure

- Lender approval for the reinsurance entity if applicable

- Whether existing F&I contracts are compatible with the chosen program structure

- Whether your domicile choice (offshore vs. domestic) aligns with your tax strategy and volume profile

A Trusted Reinsurance Partner and Administrative Support

Who administers your program shapes everything that follows. The right partner provides not just entity formation but ongoing training, claims adjudication, performance reporting, bookkeeping, and IRS-compliant tax filings.

The wrong partner leaves you exposed to:

- Hidden fees that erode profitability

- Compliance gaps that create audit risk

- Programs that never earn out due to poor administration

Key Variables That Affect Your Program's Profitability

Two dealerships with identical vehicle sales volume can produce dramatically different results from the same program structure. Profitability depends on execution variables, not just enrollment.

Claims Ratio

Claims ratio (the percentage of premiums paid out in claims) is the single most critical variable. A well-managed ratio means more underwriting profit accumulates in your program; a high ratio erodes it.

Recent industry data shows loss ratios on lifetime limited warranty products have climbed, with some exceeding 100%, driven by repair cost increases of approximately 80% from 2018 to 2025.

What determines claims ratio:

- Product quality (A-rated products with realistic coverage terms)

- Vehicle profile (age, mileage, condition)

- Coverage duration and terms

- The dealer's ability to influence claims outcomes on BHPH programs

F&I Product Penetration Rate

Penetration rate — the percentage of vehicle buyers who purchase at least one F&I product — determines how much premium flows into the program each month. Low penetration means a slow-building or stagnant program.

Industry Benchmarks:

- National service contract penetration: approximately 47%

- Top 5% of dealerships: approximately 84%

- Top 20% of dealerships: approximately 66-67%

The gap between average and top-performing dealerships represents millions of dollars in underwriting profit over time.

Product Mix and PVR (Profit Per Vehicle Retail)

The types of products sold affect both dealer front-end profit and the quality of premium ceded into the reinsurance program. Not all products contribute equally to program growth.

F&I PVR reached a record $2,614 in Q4 2025, driven by improved vehicle affordability and interest rate declines that boosted penetration. By product segment in Q1 2026:

- Luxury: $1,359 per retail unit

- Import: $1,745 per retail unit

- Domestic: $1,818 per retail unit

Increasing PVR through better menu selling and product selection improves both immediate F&I income and the long-term asset value of the program.

Investment Income on Program Assets

Reinsurance programs invest the premiums held in trust, and investment income adds a second layer of return — especially in low-claims years when reserves have had time to accumulate.

Zurich offers three asset allocation models for PARC programs:

- 100% bonds

- 90% bonds / 10% S&P 500 Index funds

- 80% bonds / 20% S&P 500 Index funds

Under IRC Section 831(b), the reinsurance company is taxed only on investment income — underwriting profits are excluded. Ask your administrator which allocation model your program uses and what historical returns that model has produced.

Common Mistakes Dealers Make When Setting Up Profit Participation

Choosing the Wrong Structure for Their Goals

Selecting a retro program for wealth building — or a DOWC when cash flow is the primary need — creates structural misalignment from day one. Most dealers who "tried reinsurance and it didn't work" made this mistake. The structure must align with your volume, tax situation, and whether you need distributions now or long-term asset accumulation.

Ignoring F&I Product Quality and Penetration

Dealers focus on forming the entity but neglect to improve the F&I sales process. This results in low premium volume, poor product mix, and a program that builds slowly or not at all.

The program is only as strong as the F&I office feeding it. If your service contract penetration is 40% and your PVR is stagnant, no reinsurance structure will fix that.

Choosing a Partner Based on Admin Fee Alone

The lowest administrative fee often signals the least support. Elite FI Partners notes that "two reinsurance programs can have identical admin fees and produce dramatically different financial outcomes depending on how the rest of the program is structured."

Before signing with any reinsurance partner, these are the questions that separate strong programs from costly ones:

Key Questions to Ask Any Prospective Reinsurance Partner

- Are there hidden ceding fees, loss adjustment expenses, or post-sale charges?

- What happens to my reserves if I stop writing contracts?

- Are there termination penalties or excessive run-off fees?

- Can I trace every dollar on my balance sheet?

- Will you provide a 10-year projection of program performance?

- What level of ongoing training and support is included?

- Are your advisors (CPA or attorney) members of the AICPA or NADC (National Association of Dealer Counsel)?

Dealers who skip these questions often discover the gap between what a program promises and what it actually pays out — after it's too late to walk away cleanly.

Conclusion

Profit participation can shift a dealership from paying third parties to building real retained income — but the results depend entirely on how the program is built. The right structure for your volume, a strong F&I product lineup, and a transparent administrative partner aren't optional details. They're what separates programs that grow from programs that stall.

Most program failures trace back to three avoidable causes:

- Wrong structure selection — choosing a program that doesn't fit your volume or deal mix

- Weak F&I execution — insufficient product penetration or inconsistent presentation

- Poor partner choice — working with an administrator that lacks transparency or industry experience

Getting those three elements right from the start is what DealerRE's setup process is designed to do. If you're evaluating whether profit participation is the right move for your dealership, reach out to the DealerRE team for a no-obligation consultation.

Frequently Asked Questions

What is the most profitable department in a dealership?

F&I is consistently among the highest-profit departments per unit. Cindy Allen, CEO of StoneEagle, stated at the 2026 NADA Show that "F&I was the foundation of profitability" and "the foundation that kept the house standing" in the face of front-end margin compression. Profit participation programs allow dealers to capture an additional layer of income from the same F&I sales, turning third-party underwriting profits into a dealer-owned asset.

Are profit-sharing plans worth it?

When properly structured and fed by a strong F&I process, profit participation programs have helped dealers build multi-million-dollar assets over time. Even smaller operations benefit — the right structure depends on your volume, cash flow needs, and tax situation.

Do I pay taxes on profit-sharing?

Tax treatment varies significantly by program structure. Retro distributions are typically taxed as ordinary income. PARC/CFC dividends often receive more favorable capital gains treatment. Dealers should work with a tax advisor familiar with reinsurance structures to optimize tax efficiency.

Can small dealerships set up a profit participation program?

Lower-volume dealerships can qualify for certain program structures — entry thresholds vary by program type. For independent and BHPH dealers especially, these programs often serve as a primary wealth-building vehicle, capturing profits that would otherwise go to third-party providers.

How long does it take to set up a dealer reinsurance company?

With a full-service partner managing entity formation, filings, and compliance, most dealers can have a program operational within a few weeks to a few months. Offshore CFC structures typically take longer than domestic retro programs due to additional international filings.

What F&I products can be included in a profit participation program?

Vehicle service contracts, GAP, prepaid maintenance, ancillary protection products (appearance protection, theft, tire and wheel), and in BHPH programs, mechanical breakdown and physical damage products can all contribute premium to a dealer's participation program. The key is ensuring products are A-rated and compatible with the reinsurance structure selected.