Dealer-owned GAP programs offer a growing alternative. Dealerships across the country are setting up their own reinsurance structures to capture that underwriting profit on every GAP contract they sell, without eliminating the product from their F&I menu. This article provides a practical guide to understanding what a dealer-owned GAP program is, whether it makes sense for your dealership, and the concrete steps involved in setting one up.

Key Takeaways

- A dealer-owned GAP program routes underwriting profit into your own reinsurance company instead of a third-party provider's pocket

- Setup requires evaluating GAP volume, selecting a program structure, forming a legal entity, and establishing premium flows

- Dealers assume underwriting risk but earn underwriting profits and build long-term financial assets within their own entity

- State-level compliance and ongoing administration require a qualified reinsurance administrator

- Volume matters: programs work best when dealerships sell enough GAP contracts monthly to manage risk and generate meaningful profit

What Is a Dealer-Owned GAP Program?

A dealer-owned GAP program is one where the dealership assumes the underwriting risk for the GAP coverage sold on its vehicles. It does this through a reinsurance company the dealer owns — rather than purchasing coverage wholesale from a third-party provider and passing the underwriting profit to them.

In the standard third-party model, GAP is sold through an outside administrator who sets the terms, holds the reserves, handles claims, and keeps the underwriting profit. The dealer earns only a dealer reserve — typically a fixed markup per contract — and nothing more.

The Admin Obligor Reinsurance Structure

Most dealer-owned GAP programs use an admin obligor reinsurance structure. An A-rated insurance carrier remains the obligor on the GAP contracts sold to customers, protecting consumers and satisfying state regulations. The dealer's reinsurance company sits behind this carrier, capturing the underwriting profit through a reinsurance agreement.

This structure gives dealers the underwriting profit opportunity without removing the consumer protection layer. The A.M. Best Financial Strength Rating of the fronting carrier matters in practice: lenders and regulators require it, and it's what allows the dealer's reinsurance company to operate behind an admitted carrier rather than standing exposed as the direct obligor.

Why Set Up a Dealer-Owned GAP Program at Your Dealership

Profit Retention

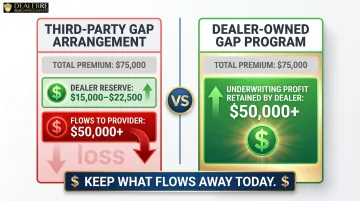

The core argument is straightforward: third-party GAP providers retain substantial underwriting profit on every contract. Consider a dealership selling 150 GAP contracts annually at $499 each — $75,000 in total premium. Here's where that money typically goes:

- Dealer reserve (third-party arrangement): $100–$150 per contract, or roughly $15,000–$22,500 total

- Flows to the third-party provider: $50,000+ to cover claims, administration, and their profit

- Dealer-owned structure: That $50,000+ stays in your reinsurance entity instead

If claims remain within expected ranges, the dealer retains a significant portion of those funds.

Tax Planning Opportunity

Earned premiums held in the dealer's reinsurance entity can offer real tax planning advantages. Under IRC Section 831(b), small insurance companies with net written premiums not exceeding $2.85 million in 2025 may elect to pay federal income tax only on investment income; underwriting income is excluded from corporate income tax.

Consult a qualified tax advisor to confirm applicability to your specific situation.

Control Over Claims Experience

Dealers running their own program can directly influence how efficiently claims are handled. A well-managed claims process protects the reserve fund and improves overall program economics. Fair, prompt claim resolution builds customer trust — and that trust drives repeat business in ways a third-party administrator has little incentive to prioritize.

Long-Term Asset Creation

Unlike a third-party arrangement where funds leave the dealership immediately, reserves accumulate within the dealer's reinsurance entity over time. These reserves become a long-term asset that can be used for reinvestment in the dealership, real estate purchases, or other wealth-building purposes — building equity outside the traditional dealership balance sheet.

Stronger Customer Experience Positioning

Owning the program gives dealers more flexibility to customize coverage terms, support customers through the claims process directly, and use GAP as a loyalty and retention tool rather than simply an income line item. That's a meaningful shift — from GAP as a transaction to GAP as part of the ownership experience.

What to Know Before You Get Started

Volume Is a Prerequisite, Not a Guarantee

A dealer-owned GAP program is most economically viable when the dealership is writing a meaningful number of GAP contracts monthly. Lower-volume operations may not generate enough premium to adequately fund reserves and absorb occasional claims.

There's no universal minimum, but industry analysis suggests these programs typically make sense at 100 or more vehicles sold monthly with solid GAP penetration. An experienced administrator can assess whether your current volume justifies the setup costs.

State-Level Regulation Is Real and Varies

GAP products are regulated differently across states. Recent state-level changes illustrate the regulatory complexity:

- Colorado HB 23-1181 effective January 1, 2024, overhauled GAP waiver regulation including fees and refunds

- Connecticut SB 1033 created new provisions for GAP and EWU waivers effective October 1, 2023

- Missouri SB 398 effective February 23, 2024, established requirements for GAP waivers and other financial protection products

- Florida SB 902 effective October 1, 2024, modified GAP provisions and created a new category for vehicle value protection agreements

Some states require specific language in waiver agreements, others have rate filing requirements or licensing considerations. New York requires prior approval of GAP insurance policy forms, and Utah requires dealerships selling GAP waivers to hold a limited line agency license.

Dealers must understand the regulatory environment in their state before launching. Proceeding without that clarity can expose the dealership to fines, forced program restructuring, or loss of the ability to sell GAP products altogether.

Once you've confirmed your regulatory footing, the next consideration is who manages the program day to day.

You'll Need a Full-Service Administrator to Run It Properly

The legal entity formation, ongoing filings, tax returns, claims adjudication, and compliance management are not tasks a dealership should handle without specialized expertise. A full-service administrator who owns these responsibilities is essential — without one, program errors compound quickly.

DealerRE manages all legal forms, filings, tax returns, and renewals on behalf of its dealer clients, allowing dealers to stay focused on selling rather than administration.

How to Set Up a Dealer-Owned GAP Program — Step by Step

These five steps cover the core process — timeline and specifics will vary by state and program type, but the sequence holds across most dealership situations.

Step 1 — Assess Your Current GAP Volume and Provider Arrangement

Start by pulling data on how many GAP contracts your dealership sells monthly and what you currently earn per deal from your third-party provider. Calculate the total income your dealership generates from GAP in a year.

Next, estimate what the underwriting profit on those same contracts would look like if it flowed to your own reinsurance entity instead of to the provider. This gap between what you earn and what the provider retains is the financial opportunity you're evaluating.

DealerRE helps dealers assess this income opportunity gap through a detailed business analysis, quantifying the profit currently retained by third-party providers and projecting potential earnings under a dealer-owned structure.

Step 2 — Select the Right Program Structure

The admin obligor reinsurance structure works as follows in practical terms:

- The dealer forms a reinsurance company

- An A-rated carrier remains the front-line obligor on the GAP contracts sold to customers

- The dealer's reinsurance company assumes the risk from the carrier and retains the underwriting profit

- This structure satisfies consumer protection requirements while keeping profits inside the dealer's entity

Decide whether the program will cover GAP exclusively or be structured to also accept other F&I products (such as vehicle service contracts) over time. Starting with one product and expanding is a common approach — many dealers begin with GAP and later add VSCs and ancillary products under the same entity once the program is running smoothly.

Step 3 — Form the Legal Entity and Address Compliance Requirements

Work with a qualified attorney and experienced reinsurance administrator to form the reinsurance company. Entity type and domicile options carry different regulatory and tax implications.

Two broad domicile categories are worth understanding:

- Domestic (Vermont, Tennessee, Utah, South Carolina, North Carolina) — regulatory stability, familiar legal frameworks, straightforward compliance

- Offshore (Turks and Caicos, Bermuda, Cayman Islands) — structural flexibility and certain tax attributes, with assets able to remain in the United States

Capital requirements commonly range from $250,000 to $1,000,000+ depending on domicile and captive type; some facilities offer lower minimums under particular arrangements.

Ensure the GAP waiver agreements, addendums, and consumer-facing documents comply with state-specific requirements. Rate filing, licensing, and disclosure obligations must be resolved before the first contract is sold under the new structure.

Step 4 — Establish Premium Flow, Pricing, and Reserve Structure

Set GAP pricing that is competitive in your market for customers while generating sufficient premium to fund the reserve account. Pricing too low leaves the reserve underfunded; pricing too high reduces penetration.

Define the mechanics of how premiums flow from each deal into the reinsurance entity, how the reserve is held and managed, and how claims will be funded when they occur. Your administrator should provide a clear framework for this.

Step 5 — Train Your F&I Team and Launch the Program

Develop an updated F&I presentation that positions GAP clearly and compellingly to customers. The product itself does not change from the customer's perspective, so the presentation should focus on coverage value, not program ownership.

Set penetration rate targets, establish a tracking system for contracts sold under the new program, and agree with your administrator on reporting cadence so you can monitor reserve levels, claims frequency, and overall program performance from day one.

F&I training — both online and in-person — is part of DealerRE's onboarding process, covering GAP presentation, menu integration, and penetration rate strategy so your team is ready before the first contract goes out the door.

Managing and Growing Your Dealer-Owned GAP Program Long-Term

Track Program Health Consistently

Review monthly performance reports to catch problems before they become reserve shortfalls. Key metrics to watch include:

- GAP penetration rate — tracks how consistently F&I is presenting the product

- Claims frequency — flags adverse loss trends early

- Reserve balance — confirms the program remains adequately funded

- Per-deal profitability — measures whether pricing is holding up against actual losses

According to StoneEagle's December 2025 benchmark data, GAP penetration reached 38% nationally, up 3 points year-over-year. That figure signals strong market demand — and that dealers with well-run programs are well-positioned to capture it.

Work With Your Administrator Annually

Annual program reviews keep your dealer-owned GAP program aligned with current performance and compliant with evolving regulations. A structured review should cover:

- Adjust pricing if loss experience has shifted

- Update F&I training as staff turns over

- Revisit coverage terms as your inventory mix or customer base evolves

- Monitor loss ratios carefully — IRS final regulations issued in January 2025 classify certain micro-captive arrangements as listed transactions if the average 10-year loss ratio falls below 30%, and as transactions of interest if below 60%

DealerRE handles ongoing compliance, legal forms, filings, tax returns, and renewals — so dealers stay focused on sales performance rather than administrative overhead.

Monitor Broader F&I Trends

Macro performance data gives your program context and helps you defend its value internally. F&I profit per vehicle retailed (PVR) among public auto retail groups averaged $2,582 in Q4 2025, up from $2,344 in Q2 2024. As front-end gross margins compress, F&I now carries more of the dealership's profit load. A well-managed GAP program isn't just a compliance checkbox — it's a direct contributor to that number.

Frequently Asked Questions

Do dealers make money on gap insurance?

Dealers typically earn a dealer reserve or markup when selling GAP through a third-party provider. A dealer-owned program allows them to capture the underwriting profit as well, which is generally a significantly larger amount per contract.

How does dealership gap insurance work?

GAP coverage sold at a dealership bridges the difference between a customer's auto insurance payout (based on actual cash value) and their remaining loan or lease balance after a total loss or theft. Dealers typically add it to the finance contract at the time of purchase.

What does Guaranteed Asset Protection cover?

GAP covers the "gap" between what a vehicle is worth at the time of total loss and what the customer still owes on their loan or lease. It does not cover mechanical repairs, missed payments, or other liabilities unrelated to a total loss event.

How to open a gap claim?

Contact the GAP administrator (or the dealership's reinsurance company in a dealer-owned program) and submit the required documentation — including the primary insurance settlement, loan payoff statement, and purchase contract. The administrator then processes the claim against the remaining balance.

What is the difference between a dealer-owned GAP program and a third-party GAP product?

In a third-party arrangement, the provider sets the terms, holds the reserves, and keeps the underwriting profit. In a dealer-owned structure, the dealer's reinsurance company assumes the risk and retains that profit. An A-rated carrier still serves as the obligor, maintaining consumer protection standards.

How long does it take to set up a dealer-owned GAP program?

The timeline varies based on program structure, state requirements, and the administrator selected. With an experienced partner managing entity formation, compliance, and documentation, most setups are completed within a few weeks to a couple of months.

Ready to explore whether a dealer-owned GAP program makes sense for your dealership? DealerRE provides comprehensive support from initial assessment through entity formation, compliance management, and ongoing administration. With 28 years of proven success helping dealers retain underwriting profits, DealerRE handles all legal forms, filings, tax returns, and renewals, so you can stay focused on sales and profitability. Contact DealerRE at (804) 824-9533 to schedule a complimentary dealership analysis.