Yet while front-end profits eroded, F&I gross profit per vehicle retailed held steady near record highs. Publicly owned dealerships reported $2,501 per vehicle in F&I gross in Q4 2024, just 3.9% below the all-time peak. That gap represents a fundamental shift: F&I is no longer a supplementary revenue line—it's the profit engine.

This guide covers how used car dealers can maximize F&I revenue through high-impact products, penetration rate optimization, dealer-owned reinsurance structures, and the metrics that matter most. If you're still sending underwriting profits to third-party providers, you're funding someone else's wealth instead of building your own.

Key Takeaways

- Front-end vehicle margins have fallen 36.6% since 2021 while F&I profits remain near record highs

- Vehicle Service Contracts and GAP deliver the highest profit impact for used vehicle buyers

- Track F&I PVR and product penetration rates monthly to identify revenue leakage

- Dealer-owned reinsurance captures 100% of underwriting profit rather than passing it to third-party providers

- Over 400 dealers nationwide use reinsurance to capture underwriting profits and build long-term dealership wealth

Why F&I Has Become the Most Critical Profit Center for Used Car Dealers

The market has fundamentally restructured used car dealership economics. Front-end gross margins have returned to pre-pandemic levels, yet consumer affordability continues to erode. Higher interest rates, elevated insurance costs, and rising repair expenses create a real paradox: buyers need protection products more than ever, but they're also more budget-constrained.

That squeeze actually works in dealers' favor. When repair costs exceed $4,700 and parts prices climb 6.6% annually, protection products stop feeling like add-ons and start delivering genuine value. Recent data backs this up:

- 58% of buyers trust the F&I manager more than a salesperson when evaluating post-sale products

- 79% of buyers report being satisfied with their F&I experience

- Used vehicle buyers face immediate repair exposure—unlike new car buyers covered by manufacturer warranties

That mechanical risk is the used car dealer's structural advantage. Vehicle Service Contracts and GAP insurance are easier to justify—and easier to sell—than nearly any franchise dealer product because the need is immediate and tangible. Dealers with strong F&I programs can match franchise stores on per-vehicle profitability even when front-end margins don't allow it.

DealerRE has observed this shift firsthand across its 400+ dealer network. When dealers control their F&I programs through dealer-owned reinsurance, they capture underwriting profits that third-party providers previously retained—turning F&I from a one-time markup into a compounding profit stream that builds dealer net worth over time.

The Most Profitable F&I Products for Used Car Dealerships

Vehicle Service Contracts (VSCs)

VSCs are the cornerstone F&I product for used car dealers. Over 50% of used car buyers purchase VSCs, compared to 42% of new car buyers—a penetration premium driven entirely by mechanical risk.

Coverage matching determines whether that penetration translates to profit or chargebacks. Match contract type to vehicle condition:

- Low-mileage program vehicles: 72-month exclusionary wrap coverage

- High-mileage inventory: Short-term powertrain plans

- Mismatched contracts: Generate chargebacks and damage customer trust

Average VSC profit on financed deals reached $1,253.53 between September 2024 and February 2025, making this the single highest-margin F&I product for most dealers.

GAP Insurance

GAP insurance addresses the single greatest financial risk for financed used car buyers: owing more than the vehicle is worth after a total loss. In Q2 2025, 53% of used vehicle loans carried loan-to-value ratios above 120%, with independent finance companies averaging 139% LTV. That means more than half of your financed buyers are upside down before they leave the lot.

Total loss frequency has also climbed—22% of all claims in 2024 were total losses, driven by declining used vehicle values and an aging vehicle pool. GAP is no longer a luxury product; it's financial protection buyers genuinely need.

The F&I conversation is straightforward: "If something happens to this vehicle, GAP ensures you won't owe thousands of dollars on a car you can't drive."

Pre-Paid Maintenance Plans

Pre-paid maintenance plans create a recurring revenue touchpoint and lock in return service visits. PPM plan holders visit their servicing dealer at a 72% rate, compared to roughly 20% for non-plan holders. When they return, 90% purchase additional retail service, spending an average of $128 per visit.

For BHPH and independent dealers trying to build long-term customer relationships, maintenance plans are a retention tool disguised as an F&I product.

Ancillary Protection Products

That retention logic extends to ancillary products — but here the play is margin, not loyalty. Appearance protection, tire and wheel coverage, theft protection, and windshield repair all carry high margin and low cost, and they complement the primary sale when bundled strategically.

However, product selection and sequencing matter. 49% of buyers purchase one to two F&I products, but penetration drops sharply beyond two—only 10% purchase three or four products. Flooding buyers with options creates decision fatigue and lowers overall conversion.

Debt Cancellation and Credit Insurance

For BHPH dealers, credit life and disability products protect the dealer's portfolio while providing genuine value to customers. It's also a category where third-party providers pocket significant profit that dealers can recapture directly — which is exactly what dealer-owned reinsurance programs like those administered by DealerRE are structured to do.

How to Maximize F&I Penetration Rates and Per-Vehicle Revenue

Track two metrics religiously: F&I penetration rate (percentage of deals where a specific product is sold) and F&I PVR (total F&I gross profit divided by total vehicles retailed). Tracking these separately for each product category pinpoints which products are underperforming and where the fastest gains are available.

Use Menu-Based Selling to Drive Consistency

A well-designed menu presentation ensures every customer sees every product at every deal. 63% of consumers are more likely to purchase F&I products if they can research them before finalizing the purchase, and electronic menus automate compliance while eliminating inconsistency among sales staff.

Dealers who present every product on every deal consistently see measurable gains in both penetration and PVR — the industry benchmark is 100% product presentation, 100% of the time.

Train Sales Staff to Introduce Protection Early

Don't leave F&I entirely to the F&I office. When buyers are mentally preparing for total cost of ownership rather than just sticker price, F&I products feel like part of the solution rather than an upsell.

A salesperson can plant the seed during the vehicle walk-around:

- Reference mileage: "This truck has 78,000 miles — most of the factory warranty is gone."

- Bridge to F&I: "Our finance team will show you how to protect yourself from repair costs."

- Set the expectation early so the buyer arrives at the F&I desk prepared, not surprised.

Frame Products in Monthly Cost, Not Total Price

Financed buyers are statistically more receptive to F&I products because the additional monthly cost impact is minimal. Vehicle service contracts are 2.5X more likely to be sold on a finance deal, and financed vehicles generate an average of $170.59 more in F&I profit.

Present products in monthly terms: "$18 per month for GAP coverage" feels manageable; "$499 total" feels like sticker shock.

Invest in Ongoing F&I Manager Training

Unlike franchise dealers, independent used car dealers often have F&I managers wearing multiple hats. Regular training on objection handling, product knowledge, and compliance directly impacts revenue outcomes. Both online and in-person programs are widely available, and the dealers who invest consistently in training are the ones with the highest PVR numbers to show for it.

Key F&I Metrics Every Used Car Dealer Must Track

F&I PVR (Per Vehicle Retailed)

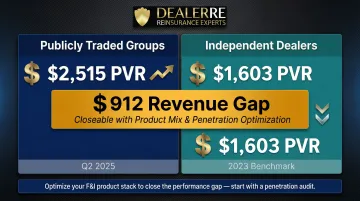

This is the single most important F&I performance metric. Calculate it by dividing total F&I gross profit by total vehicles retailed. Publicly traded auto retail groups reported an average F&I gross profit PVR of $2,515 in Q2 2025.

Independent dealers averaged $1,603 PVR in 2023—a $912 gap that points directly to product mix and penetration as the levers to pull. Monitor monthly trends. A declining PVR almost always signals a breakdown in process, not just in performance.

Products Per Deal (PPD)

PPD reveals whether your F&I team is presenting all products or defaulting to their comfort zone. The benchmark PPD range is 1.3 to 1.7 products.

When PPD falls below that range, two culprits are usually responsible:

- Low VSC or GAP penetration — signals that F&I staff aren't presenting all products consistently

- Cash deals mixed into your data — these naturally suppress PPD and distort your benchmarking

Track cash deals separately to keep your analysis clean.

Product Penetration Rate by Category

Break penetration down by product — VSC %, GAP %, maintenance % — instead of total F&I revenue alone. Industry averages for extended warranty penetration run between 40–50%.

A dealer with strong VSC numbers but weak GAP penetration doesn't have an F&I problem — they have a sequencing problem. Adjusting when and how GAP is introduced in the presentation often closes the gap without any additional training investment.

Common F&I Mistakes That Kill Used Car Dealer Profits

Relying Entirely on Third-Party F&I Providers

Most dealers using third-party warranty and insurance companies are funding the profits of those providers rather than their own balance sheet. The gap between what customers pay and what dealers retain is where significant money disappears.

Here's how the math works against you in a standard commission model:

- VSC loss ratios typically run 40–65%

- An insurer with a 25% expense ratio and 65% loss ratio yields a 10% underwriting margin

- The third-party insurer keeps 100% of that underwriting profit — plus 100% of investment income on reserves

You funded those reserves. They collect the return.

This is the primary profit leakage problem for independent dealers. A dealer-owned reinsurance structure — like the admin obligor model DealerRE administers — routes those underwriting profits back to the dealer's own company.

Offering Too Many Products in a Single Presentation

Purchase rates drop sharply beyond two products. Flooding buyers with options creates decision fatigue and lowers overall conversion. Quality of presentation beats quantity of products every time.

Focus on VSC and GAP as your foundation, then layer in one ancillary product if it fits the customer's needs.

Neglecting F&I Compliance

Non-compliant F&I practices — undisclosed markups, improper disclosures, payment packing — expose dealerships to regulatory risk and chargebacks. The FTC issued warning letters to 97 auto dealership groups in March 2026 targeting deceptive pricing, hidden fees, and mandatory add-ons. (The FTC's CARS Rule was separately vacated and withdrawn, but enforcement attention has not eased.)

Chargebacks and regulatory penalties erode margin faster than most dealers realize. Clean process documentation and consistent disclosure practices are the cheapest insurance a dealer can buy.

Beyond Standard F&I: How Dealer-Owned Reinsurance Unlocks the Full Profit Potential

Instead of selling third-party F&I products and watching providers keep the reserve and claims profit, a dealer-owned reinsurance company allows the dealer to capture 100% of those profits. The premiums customers pay fund the dealer's own insurance structure rather than enriching an outside provider.

The Financial Benefits

Reinsurance income includes three streams:

- Underwriting profits when claims are lower than premiums collected

- Investment income on held reserves

- Tax planning advantages through IRC Section 831(b) elections

These are revenue streams completely invisible to dealers using standard third-party arrangements.

A mid-size independent dealer selling 50 vehicles monthly with a 45% VSC attachment rate and 39% GAP penetration generates approximately $567,000 in annual premium. Under a dealer-owned reinsurance company, 100% of the underwriting profits and investment income on that premium pool returns to the dealer — not a third-party administrator. That income can then be reinvested into the dealership, real estate, college education, or other assets.

The Admin Obligor Structure

An A-rated insurer backs the program, meaning the dealer's reinsurance company is protected. This is not a self-insured risk but a structured program with legitimate insurance backing. If the dealer's reinsurance company becomes unable to meet its financial obligations, liability rests entirely with the direct writing insurance company. The dealer's personal liability is limited to formation costs plus accumulated earnings.

Reserves are held through a Trust Agreement involving the direct underwriting insurance company, the reinsurance company, and a Trust Company as Trustee. All funds remain in U.S.-based accounts — nothing is sent offshore. The Trust Agreement permits withdrawals only for:

- Payment of covered repair claims

- Limited professional fees

- Payment of income taxes

- Withdrawal of funds exceeding required reserves

DealerRE's Role

DealerRE has spent 28 years helping independent, franchise, and BHPH dealers establish and manage their own dealer-owned reinsurance companies. The company handles all legal forms, filings, tax returns, renewals, claims adjudication, and F&I training so dealers can focus on running their dealership rather than managing administrative complexity.

Over 400 dealers nationwide have used this model to capture underwriting profits they were previously passing to third-party providers. DealerRE's target market is dealers selling more than 30 cars per month, though the largest misconception is that high volume or high startup costs are required — neither is the case.

Frequently Asked Questions

What is the average F&I profit per vehicle for a used car dealership?

F&I PVR benchmarks vary by dealer type and product mix. Publicly traded groups averaged $2,515 in Q2 2025, while independent used car dealers averaged $1,603 in 2023. Independent dealers can reach or exceed franchise dealer F&I PVR with the right products, training, and reinsurance structure.

What F&I products are most important for used car dealers?

Vehicle Service Contracts and GAP insurance are the two highest-priority products given the mechanical risk and financing dynamics of used vehicle transactions. Ancillary products like tire and wheel, appearance protection, and pre-paid maintenance play a supporting role but should not replace the core two.

What is a good F&I penetration rate for a used car dealership?

Penetration benchmarks differ by product and dealer volume. A VSC penetration rate above 40-50% is generally considered strong for used car dealers, while GAP penetration varies based on financing mix. Track trends over time rather than focusing on any single month's number.

How can independent used car dealers improve F&I performance without a dedicated F&I manager?

Three practical starting points:

- Use menu-based selling tools to structure every product presentation

- Cross-train sales staff on product basics so F&I coverage is never a single point of failure

- Partner with an F&I training resource — DealerRE's programs are accessible via mobile device

Part-time and virtual F&I solutions are also available for smaller operations that aren't ready for a dedicated hire.

What is the difference between standard F&I income and reinsurance income?

Standard F&I income is the profit retained on the sale of each product. Reinsurance income captures the reserve and claims profit that third-party providers currently keep. Reinsurance lets dealers retain both streams at once: front-end gross profit and back-end underwriting profit.

Is dealer-owned reinsurance right for every used car dealer?

Reinsurance is best suited to dealers with sufficient F&I volume to fund reserves—typically those selling more than 30 cars per month. Consult with a reinsurance specialist like DealerRE at (804) 824-9533 to evaluate whether your current F&I program is leaving money on the table.