Introduction

Non-compliance in sales and F&I can result in multi-million dollar fines, class action lawsuits, and permanent reputational damage. The FTC, state attorneys general, and plaintiff attorneys are all actively pursuing auto dealers — and recent cases make clear that no dealer is too big or too small to be targeted.

In December 2024, the FTC and Illinois Attorney General secured a $20 million settlement against Leader Automotive Group for deceptive pricing and charging for add-ons without consent. Just months later, Lindsay Automotive Group faced a $75 million consumer redress order for similar violations. In March 2026, the FTC sent warning letters to 97 dealership groups about deceptive pricing practices — a clear signal that enforcement is accelerating, not slowing down.

This guide defines the scope of sales and F&I compliance — from advertising to deal-signing — and provides practical checklists and program-building strategies for independent dealers, franchise dealers, BHPH operators, and F&I managers navigating this high-stakes regulatory environment.

TLDR:

- Compliance spans the full deal cycle — from advertising to the signed contract, not just F&I disclosures

- TILA, ECOA, and the FTC Safeguards Rule remain enforceable regardless of any regulatory changes

- Written compliance programs, trained staff, and documented deal files are your core defenses

- Compliant dealerships build customer trust that translates to repeat business and stronger F&I profits

What Is Sales and F&I Compliance?

Sales and F&I compliance refers to the full set of legal obligations a dealership must meet — from the moment a car is advertised through the final signing of financing documents. That scope covers:

- Truthful advertising and accurate price disclosures

- Fair lending practices under ECOA and TILA

- Proper disclosure of voluntary protection products (VSCs, GAP, ancillary products)

- Customer data protection under the Safeguards Rule

- Accurate documentation at every customer touchpoint

Why Independent and BHPH Dealers Face Unique Exposure

Independent and BHPH dealers face the same federal and state obligations as large franchise groups but often lack dedicated compliance resources. Despite smaller teams, these dealers remain equally visible to regulators and plaintiffs' attorneys. The playing field is level when it comes to enforcement: a 10-unit BHPH lot faces the same ECOA and TILA requirements as a 500-car franchise store.

F&I Compliance vs. General Business Compliance

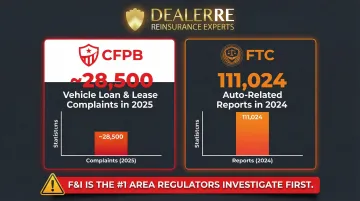

F&I compliance is specifically regulated because it combines consumer credit, insurance products, and high-value purchases — making it a priority target for the FTC, CFPB, and state attorneys general. The CFPB received approximately 28,500 vehicle loan or lease complaints in 2025, while the FTC logged 111,024 auto-related reports in 2024. For dealers, that volume of complaints means F&I is one of the highest-risk areas regulators investigate first — not general sales operations.

Key Federal and State Regulations Every Dealer Must Know

Truth in Lending Act (TILA) / Regulation Z

Reg Z requires dealers to disclose the APR, total finance charge, and total cost of credit in all credit transactions. A frequently overlooked violation: if a dealer charges more for an F&I product on financed deals versus cash deals (surcharging financed customers), the difference must be included in the finance charge and reflected in the APR. Failing to do so understates the true cost of credit and violates TILA.

Key requirement: Dealers must provide accurate APR disclosures that include all finance charges, not just interest rates.

Equal Credit Opportunity Act (ECOA) and Fair Credit Reporting Act (FCRA)

ECOA prohibits discriminatory credit decisions based on race, sex, national origin, or other protected characteristics. Dealer markup policies on interest rates create ECOA exposure if not applied consistently. In October 2022, Passport Automotive Group settled with the FTC for $3.38 million after Black and Latino customers were charged higher markups due to inconsistent discretionary pricing.

FCRA requires dealers acting as lenders to issue Adverse Action Notices whenever credit is denied or terms are countered and the customer does not accept. Deal files must contain evidence of compliance, including copies of notices sent.

Key requirement: Markup policies must be documented, consistently applied, and audited regularly to avoid both ECOA and FCRA exposure.

FTC Safeguards Rule and Red Flags Rule

Beyond credit decisions, dealers face significant obligations around data security. The FTC Safeguards Rule requires dealerships to maintain a written information security program covering encryption, access controls, employee training, and third-party vendor oversight. As of May 2024, dealers must report breaches involving 500+ consumers' unencrypted data within 30 days.

The Red Flags Rule mandates a written Identity Theft Prevention Program and OFAC checks on every deal. These two rules are among the most commonly audited today.

State "Junk Fee" and UDAP Laws

State-level enforcement has intensified around undisclosed fees, pre-loaded add-ons, and bait-and-switch advertising. Even without a federal CARS Rule in effect, the FTC actively enforces Unfair and Deceptive Acts and Practices (UDAP) authority. State attorneys general are following suit. Pennsylvania's AG secured $130,000 from the Rosado Group in August 2025 for inflating vehicle prices with undisclosed add-ons.

Critical rule: All fees beyond taxes, title, and registration must be clearly disclosed in advertised prices. No exceptions.

IRS Form 8300 and Cash Reporting

Federal law requires dealers to report cash transactions over $10,000 using IRS Form 8300. Dealers frequently miss nuances like structuring rules — when multiple related cash transactions aggregate above the threshold, they must be reported. BHPH dealers handling higher cash volumes should prioritize staff training on these rules.

The Sales and F&I Compliance Checklist Every Dealer Needs

Advertising and Pricing Transparency

All advertised prices must include every dealer fee, excluding only government taxes, tags, and registration. Online listings, window stickers, and supplemental addendums should match the Buyer's Order. Any dealer-added products pre-installed on vehicles must be fully disclosed and separately priced.

Deal Documentation Requirements

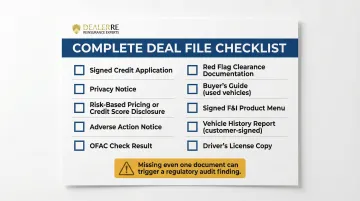

Every deal file should contain:

- Signed credit application

- Privacy Notice

- Risk-Based Pricing or Credit Score Disclosure

- Adverse Action Notice (if applicable)

- OFAC check result

- Red Flag clearance documentation

- Buyer's Guide (for used vehicles)

- Signed F&I product menu

- Vehicle history report (customer-signed)

- Legible copy of driver's license

Missing even one of these documents can trigger findings in a regulatory audit or expose the dealership in litigation.

F&I Product Presentation and Disclosure

Every customer must be presented with an F&I products menu that clearly lists each product, its cost, and its optional nature. Never bundle products into a payment without explaining each one and obtaining customer consent. If a customer declines a product, document it.

NADA recommends a uniform VPP (Voluntary Protection Products) policy to ensure consistent pricing across all customers and reduce fair lending exposure.

Identity Verification and Fraud Prevention

A legible driver's license copy must be in every deal file. It serves two purposes: confirming the customer's identity and verifying their name matches the credit application and contract. OFAC checks are required on every deal.

For BHPH dealers, synthetic identity fraud is an elevated risk. Effective safeguards include multi-factor verification and cross-checking credit application details against government-issued IDs.

Record Retention

- Deal files: Retain for at least 7 years (signed documents and disclosures)

- Dead deals: Retain for at least 5 years (credit applications that didn't result in a sale)

- OFAC records: Extended to 10 years as of March 2025

- ECOA adverse action files: Retain for 25 months

Proper storage (secure, organized, and accessible for audits) is as important as the retention period itself.

Consistent Fee Application

Dealer doc fees must be consistent across all deals. Inconsistent application, even when unintentional, creates ECOA and UDAP exposure. Key steps to protect the dealership:

- Set a single doc fee amount applied to every transaction

- Document the uniform fee policy in writing

- Review fee application during deal audits to catch drift early

In states without mandatory doc fee caps, a written policy is the primary defense against discrimination allegations.

How to Build an F&I Compliance Program at Your Dealership

Appoint a Compliance Overseer

Every dealership needs a designated compliance officer or manager — even if it's a dual-role position. Responsibilities include reviewing deal files, managing the written compliance program, handling customer complaints, and staying current on regulatory changes. Without clear ownership, compliance gaps go undetected until they become liabilities.

Create Written Policies and Procedures

A compliance program isn't a verbal agreement — it must be documented. Essential written policies include:

- F&I policy covering VPP pricing consistency, menu use, and fair lending

- Employee code of conduct

- Complaint resolution process

- Cash reporting policy

Regulators view the absence of written policies as evidence that compliance is not a priority. In the Passport Auto case, the FTC noted the dealer had an anti-discrimination policy but failed to enforce or monitor it, leading to discriminatory markups.

Train Staff Continuously

Compliance training cannot be a one-time onboarding event — it must be ongoing. F&I managers should be trained on:

- Every product they sell (not just given a script)

- Fair lending principles

- Cash reporting nuances

- Proper documentation requirements

Sales staff need training on truthful advertising and permissible sales practices. Earning third-party certifications takes that training a step further — formalizing it in a way that signals credibility to both customers and regulators:

- AFIP (Association of Finance & Insurance Professionals) offers F&I Professional certification with recertification every two years

- ADCO (Association of Dealership Compliance Officers) administers the Dealership Compliance Officer Professional (DCOP) Certification covering F&I regulations and CMS framework

- ACE (Automotive Compliance Education) provides role-specific certifications for Compliance Officers and F&I Specialists with annual recertification

For dealerships building or upgrading their programs, DealerRE offers F&I training classes — both online and in-person — designed to meet dealers where they are.

Conduct Regular Internal Audits

Set up a periodic (minimum quarterly) deal file review process — pull a random sample of deals and check against a compliance checklist. Audits should evaluate:

- Front-end: Advertising, stickers, menus

- F&I process: Documentation, disclosures, identity verification

Issues found should trigger immediate corrective action, retraining, and documentation of remediation.

Communicate Compliance to Customers

Compliance efforts have marketing value when shared with customers. Best practices include:

- Prominently posting certifications

- Displaying a code of ethics

- Providing an easy complaint pathway

- Training staff to verbally reinforce the dealership's commitment to transparency

Car salespeople rank near the bottom of Gallup's annual honesty and ethics survey — below lawyers and lobbyists. Dealerships that proactively communicate their compliance practices give customers a concrete reason to trust them before the negotiation even starts.

How Compliance Strengthens Your F&I Profitability

Dealers who operate transparent, compliant F&I programs avoid fines, litigation costs, and remediation expenses that can erase years of F&I income. Despite regulatory pressures, compliant F&I practices remain highly profitable — public dealer groups reported an average F&I Gross Profit per Vehicle Retailed (PVR) of $2,515 in Q2 2025.

Customers who trust the dealership are more likely to accept F&I product presentations. When information is clear and transparent, customers feel more at ease and have a better buying process — meaning compliance and product penetration rates are positively correlated.

The Link Between Dealer-Controlled Products and Compliance

Third-party warranty and insurance providers often leave dealers with limited visibility into how products are structured, priced, and represented — creating compliance gaps. Dealers who own their F&I product programs through dealer-owned reinsurance (such as the admin obligor reinsurance programs DealerRE helps dealers establish) gain direct control over:

- Product terms: Customize VSCs, GAP, and ancillary products to match inventory and customer needs

- Pricing consistency: Capture 100% of underwriting profits while maintaining uniform pricing across all customers

- Claims handling: Manage customer claims directly through the dealer's own reinsurance company, ensuring prompt, fair resolution that strengthens retention

This reduces compliance exposure while capturing profits previously lost to third-party providers.

Looking Ahead

As state and federal enforcement grows stricter, dealers who build compliance infrastructure now will outpace competitors still scrambling to catch up. That infrastructure includes:

- Written compliance programs and internal review processes

- Trained F&I staff who present products consistently across every deal

- Documented deal files that demonstrate fair treatment to regulators

Dealers who check those boxes protect their revenue — and build the kind of customer trust that drives repeat business and referrals.

Frequently Asked Questions

What is finance and compliance in a dealership context?

Finance and compliance refers to the legal and ethical obligations dealerships must meet when advertising, selling, and financing vehicles. This covers federal laws like TILA and ECOA, FTC rules, and state consumer protection requirements designed to protect buyers from deceptive or unfair practices.

What is insurance compliance in auto F&I?

Insurance compliance in F&I means ensuring voluntary protection products — VSCs, GAP insurance, and credit life — are presented accurately and priced consistently. Insurance compliance in F&I means ensuring voluntary protection products — VSCs, GAP insurance, and credit life — are presented accurately, priced consistently, and fully disclosed as optional. Each must also be administered in line with state insurance regulations and federal consumer protection laws.

What is an example of financial compliance at a dealership?

A concrete example: issuing an Adverse Action Notice when a customer's credit application is denied, or providing a Risk-Based Pricing Disclosure to every credit applicant. Both are federal requirements dealers must meet on every deal.

What are the most common F&I compliance violations at dealerships?

The most frequently cited violations include:

- Undisclosed fees in advertised prices

- Adding F&I products without customer consent (payment packing)

- Failure to issue Adverse Action Notices

- Incomplete deal files

- Inconsistent pricing that creates fair lending exposure

What happens if a dealership fails an F&I compliance audit?

Failures can trigger FTC or state AG enforcement, civil fines, class action lawsuits, and mandatory customer refunds. A documented compliance program with corrective action history significantly reduces liability even when a violation surfaces.

How often should dealers conduct F&I compliance training?

Best practices call for training at least annually, with ongoing reinforcement when new staff join, regulations change, or internal audits reveal compliance gaps. Continuous training is the single most effective defense against F&I violations.