Introduction

The F&I office is one of the highest-margin departments in any dealership. According to Haig Partners' Q4 2025 analysis, publicly traded dealer groups reported average F&I profit per vehicle retailed (PVR) of $2,614—a 5.2% year-over-year increase even as front-end gross margins continue to compress. Ancillary products—the protection and coverage items sold beyond the vehicle itself—are now where dealerships build sustainable back-end profitability.

Adding products to your F&I menu sounds straightforward, but results vary dramatically depending on execution. This guide covers the complete process:

- Product selection and portfolio fit

- Provider vetting and contract administration

- Pricing setup and margin structure

- Compliance requirements by product type

- Staff training and presentation techniques

- Menu structure best practices

Key Takeaways

- Ancillary F&I products — VSC, GAP, tire & wheel, appearance protection, and key replacement — drive the majority of dealership back-end profitability

- Adding products successfully means auditing your current mix, vetting providers, setting pricing protocols, and training your F&I staff

- Keep your menu focused — bundling low-margin ancillaries and leading with VSC and GAP improves conversion rates

- Dealers who establish their own reinsurance company retain the underwriting profits that third parties typically keep

- Poor staff training and skipped compliance disclosures are the two most common—and costly—mistakes

What Are Ancillary F&I Products (and Why They Matter to Your Dealership)

Ancillary F&I products are protection and coverage products sold in the finance office alongside the primary vehicle purchase. They are distinct from the vehicle price and core financing. Common examples include vehicle service contracts (VSC), GAP insurance, tire and wheel protection, appearance protection (interior and exterior), key replacement, paintless dent repair (PDR), windshield protection, and 24/7 roadside assistance.

These products have become central to dealership profitability. Front-end margins on vehicle sales have compressed significantly—Haig Partners reports new-vehicle front-end gross PVR declined to $2,948 by Q4 2025, while used-vehicle front-end PVR settled near $1,512. Meanwhile, F&I back-end income has grown steadily, with F&I PVR reaching record levels.

When presented honestly, ancillary products deliver real value to customers — not just revenue to the dealership:

- GAP protects buyers with little equity from owing more than their vehicle is worth after a total loss

- VSC limits out-of-pocket repair costs and keeps buyers on the road

- Appearance protection preserves resale value over the life of the vehicle

Treating the finance office as a customer experience touchpoint — rather than a pure upsell opportunity — builds the trust that drives repeat business and referrals.

How to Add Ancillary F&I Products to Your Dealership Menu

Step 1: Audit Your Current F&I Menu and Performance

Start by reviewing what ancillary products you currently offer, if any. Pull penetration rates and per-vehicle retail (PVR) data to identify what is selling, what is not, and where gaps exist in your product mix.

Identify whether your current menu is too long—causing customer fatigue and low conversion—or too sparse, leaving revenue on the table. Use this audit as the baseline to guide product additions. For example, if your VSC penetration is below 40% but your GAP is at 50%, focus training efforts on VSC presentation rather than adding more products.

Step 2: Identify Which Ancillary Products Fit Your Dealership and Customer Base

Match products to your typical customer profile:

- BHPH and used-car buyers may benefit most from VSC, GAP, and key replacement

- Franchise dealership customers often respond well to appearance protection and tire and wheel coverage

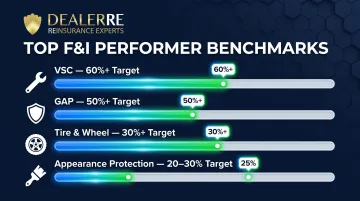

DealerInt's operational benchmarks suggest target penetration rates for top performers:

- VSC: 60%+

- GAP: 50%+

- Tire & Wheel: 30%+

- Appearance protection: 20-30%

Prioritize products that offer genuine value to the buyer and are accepted by the lenders your dealership works with. Some lenders cap loan-to-value (LTV) ratios or exclude specific ancillary products, so verify lender compatibility before adding anything to the menu.

Step 3: Select and Vet Your Product Providers

Evaluate third-party F&I product administrators on several criteria:

- Claim payment speed

- Customer service reputation

- Product terms and exclusions

- Commission structure

- Long-term reliability

A weak provider reflects poorly on your dealership when claims are denied or delayed. CFPB supervisory findings document cases where refund delays averaged 84 days, with some reaching 423 days—creating inflated balances and significant consumer harm.

Those delays point to a structural problem: third-party providers retain underwriting profits on every contract sold, and your dealership absorbs the reputational risk when things go wrong. Dealers who establish a dealer-owned reinsurance company (admin-obligor structure) eliminate that dependency. DealerRE helps dealers set up and manage these programs, replacing third-party F&I products with their own reinsurance company and keeping 100% of the underwriting profit.

Step 4: Establish Pricing, Lender Compliance, and Disclosure Protocols

Price each ancillary product appropriately. Avoid aggressive markups that create consumer complaints or fair lending risk. Consistent pricing across all customers also reduces discrimination exposure — an area regulators are actively scrutinizing.

The compliance stakes are real. The FTC and Maryland AG settlement with Lindsay Auto Group resulted in a $3.1 million civil penalty and up to $75 million in consumer refunds, with requirements including total price advertising and express informed consent for any add-on. The FTC also warned 97 dealer groups about deceptive pricing practices involving add-ons not reflected in advertised prices.

Establish a written disclosure process before you launch any new product. Every ancillary item must be presented to every customer, and any declination must be documented with a customer signature — both a legal safeguard and a defensible paper trail if questions arise later.

Step 5: Train Your F&I Staff on Each Product and the Presentation Process

Equip F&I managers with a clear, product-specific value statement for each ancillary item. Staff who cannot confidently articulate a product's benefit to a specific customer type will undersell or avoid presenting it altogether.

Conduct regular training — both in-person and online — to keep staff current on product terms, pricing changes, and presentation techniques. Also brief sales staff on F&I products so they can set expectations before customers reach the finance office; a warm handoff consistently improves conversion.

DealerRE offers in-person and online F&I training that covers product value statements, presentation techniques, compliance disclosures, and customer interview processes.

How to Structure Your F&I Menu for Maximum Conversions

The number and arrangement of products on your menu directly affects customer experience and acceptance rates. CDK Global's F&I research found that nearly half of customers will add a product if offered only a handful of options, with interest declining as more offers are presented.

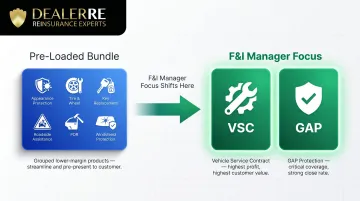

Separate High-Margin Products from Low-Margin Ancillaries

A proven strategy is to preload bundled ancillary products (appearance protection, tire and wheel, key replacement, roadside, PDR, windshield) as a package in the deal structure. This allows F&I managers to dedicate their limited time to presenting and closing VSC and GAP—the two products with the highest commission and customer value.

Menu Format Options

Column-based menus give customers a choice between packages rather than a flat yes/no on each product — that shift in framing is what drives acceptance. Physical menus display 2–4 coverage tiers with monthly payment impact per tier; digital systems use tablet or desk-mounted screens for the same structure interactively. DealerInt reports that a four-column menu outperforms a three-column menu by 5–10% in total product penetration.

Industry research points to a few clear guardrails for effective menu design:

- Keep columns to 4 maximum — more options increase decision fatigue

- Limit bundles to 4–5 to prevent overload

- Target a 3–4 minute initial presentation before fielding questions

Anchor on Total Cost Transparency

Menu format gets customers to the table. What keeps them — and protects your CSI scores — is how you handle transparency once they're there.

Monthly payment framing is a standard sales technique, but when a customer asks for the total cost, give it to them directly. Every menu presentation must show the base payment (no products) as the starting point. That disclosure isn't optional: it's a compliance requirement in most states and the single fastest way to prevent post-sale buyer's remorse from turning into a reputation problem.

Key Factors That Determine How Well Ancillary Products Perform on Your Menu

Three variables consistently separate high-performing ancillary menus from average ones. Getting all three right compounds your results.

Product-to-Customer Fit

The most consistent predictor of ancillary product acceptance is how relevant the product is to the buyer's specific situation. GAP is most valuable for low-down-payment buyers; VSC matters most to buyers of higher-mileage used vehicles. F&I managers should identify these situations during the customer interview before opening the menu.

Provider and Contract Quality

A product is only as strong as the contract behind it. Overly exclusionary terms, slow claims processing, and poor customer service on claims drive cancellations and harm CSI. Auto Finance News reports that chargebacks from early cancellations of aftermarket products are squeezing F&I profits—a direct hit to per-deal income that compounds quickly at volume.

Staff Consistency and Confidence

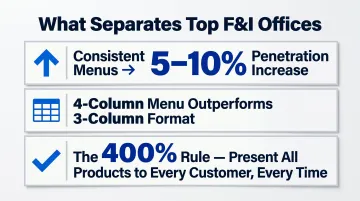

DealerInt links universal presentation discipline directly to penetration gains. Key findings:

- Consistent menus shown to every customer produce 5–10% penetration increases

- A four-column menu outperforms three-column formats in acceptance rates

- The "400% rule" — presenting all products to all customers every time — is the standard practice separating top-performing F&I offices from average ones

Common Mistakes Dealers Make When Adding Ancillary Products to Their Menu

Overloading the Menu with Too Many Individual Products

When customers are presented with 10+ line items, they disengage. This is one of the most documented reasons for low ancillary acceptance rates. The solution is bundling lower-margin items and focusing F&I presentation time on 2–3 core products.

Choosing Providers Based Solely on Highest Commission Rates

High dealer compensation does not always correlate with quality claims handling. A product with a bad claims reputation erodes trust, triggers cancellations, and generates negative reviews that damage the dealership's reputation.

Skipping Staff Training When Adding New Products

Adding a product to the menu system without training F&I managers on its value proposition, terms, and ideal customer profile results in weak presentations — or none at all.

Ignoring Compliance and Disclosure Requirements

Three compliance failures carry the most regulatory risk:

- Failing to document customer declinations in writing

- Applying inconsistent pricing across different customer groups

- Presenting products as required for financing approval

Each exposes the dealership to regulatory action and litigation. The CFPB documented multiple abusive add-on practices in auto finance, including financing void GAP on salvage titles, onerous cancellation hurdles, and failure to process unearned premium refunds.

Frequently Asked Questions

What is an F&I menu?

An F&I menu is a structured presentation tool used by finance and insurance managers in the dealership's finance office to present ancillary product options to customers, typically organized into coverage tiers with associated monthly payment impacts.

What does ancillary mean in F&I?

"Ancillary" in F&I refers to supplemental products offered alongside core vehicle financing—VSCs, GAP, tire and wheel protection, and appearance coverage—that add buyer value while generating back-end profit for the dealership.

What is the main reason to use a menu presentation with F&I customers?

Menu presentations ensure every product is disclosed to every customer in a consistent, compliant format. Structuring the decision as a choice between packages—rather than a yes/no on each product—improves acceptance rates and protects the dealership from compliance risk.

What are the most profitable ancillary F&I products for dealers?

VSCs and GAP insurance generate the highest per-deal profit, followed by tire and wheel protection. How much a dealer actually keeps is directly tied to whether they sell through a third-party provider or retain underwriting profits through a dealer-owned reinsurance structure.

How many products should be on a dealership F&I menu?

Most dealerships should keep the active F&I menu presentation focused on 2–4 items (typically VSC, GAP, and one bundled ancillary package), with additional products available but not front-and-center. Research and industry experience consistently show that fewer options improve customer engagement and close rates.

Is dealer financing ever a good idea for car buyers?

Dealer financing can offer convenience and competitive rates, especially for buyers who qualify for manufacturer or dealer incentives. Buyers should compare the APR with their bank or credit union before committing, and understand that the financing conversation and the F&I product presentation are two separate decisions.