Introduction

Florida accounts for roughly 20% of global property catastrophe reinsurance demand — more than any other single state. Hurricane Ian generated $54 billion in insured losses in 2022 alone. Combine that exposure with Florida's booming economy, high vehicle density, and litigation environment, and you get a market that demands the most sophisticated reinsurance operations in the world.

Major global reinsurers have built entire catastrophe modeling divisions around Florida, not just served it from a distance. For Florida-based insurance companies, the right reinsurance partner is often the difference between surviving a bad hurricane season and insolvency.

This guide covers the top reinsurance companies operating in Florida, what makes each notable, and how to evaluate them. If you're an auto dealer, it also explains why the reinsurance opportunity most relevant to your business looks very different from the names on this list.

TL;DR

- Florida represents ~20% of global property catastrophe reinsurance demand, making it the world's most concentrated hurricane reinsurance market

- Munich Re, Swiss Re, RenaissanceRe, Everest Re, and TransRe each actively write Florida risk with distinct strengths and ratings profiles

- Prioritize AM Best A- or better ratings when selecting a reinsurer — financial strength matters more than brand name

- Auto dealers in Florida aren't typically clients of these global reinsurers — they have access to a separate, highly profitable dealer-owned reinsurance structure

- DealerRE has helped 400+ dealers nationwide establish their own reinsurance companies to capture F&I profits currently going to third parties

Overview of Reinsurance in Florida

Reinsurance is insurance for insurance companies. As the NAIC defines it, it's a contract where a primary insurer (the cedent) transfers all or part of the risk from policies it has written to a reinsurance company, which assumes that risk in exchange for a premium. This allows primary insurers to expand capacity, stabilize earnings, and survive catastrophic loss events without depleting their capital.

Florida makes this arrangement unusually critical. The state holds only 9% of total U.S. homeowners' insurance premiums but generates 79% of the nation's homeowners' insurance lawsuits, per NAIC data. Meanwhile, U.S. insured natural catastrophe losses hit $115.6 billion in 2024 — and Florida-impacting storms drive a disproportionate share of that total year after year.

Florida's Insurance Market by the Numbers:

- $305 billion total insurance industry regulated by Florida OIR

- 4,876 insurance-related entities in Florida

- 209,711 insurance industry jobs statewide

- 6.52% of Florida GDP generated by the insurance sector

That scale means every major global reinsurer carries active Florida risk exposure, either directly or through intermediary placements.

Florida's reinsurance market extends well beyond property catastrophe, though that's where most attention lands. Auto dealers, specialty lenders, and BHPH operators also rely on reinsurance structures — they're just built around F&I product risk rather than hurricane exposure.

Top Reinsurance Company Offices in Florida

The companies below were selected based on market presence in Florida, financial strength ratings, specialization in lines relevant to Florida's risk profile, and overall industry reputation among cedents and brokers.

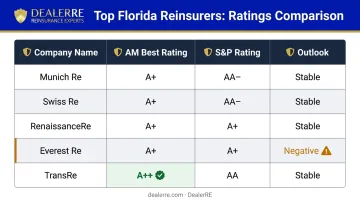

Munich Reinsurance America (Munich Re)

Munich Re is one of the world's largest reinsurers, with U.S. operations headquartered in Delaware and active participation in Florida's property catastrophe and specialty markets. Its S&P rating was upgraded to AA in July 2024 — reflecting sustained strong performance across its global platform.

Munich Re's catastrophe modeling capabilities and broad treaty capacity make it a primary market for Florida-focused cedents placing property cat, proportional, and specialty programs across multiple lines.

| Category | Details |

|---|---|

| Focus Areas | Property catastrophe, casualty (auto liability, general liability, workers' comp), specialty lines |

| AM Best Rating | A+ (Superior), Stable |

| S&P Rating | AA (Very Strong), Stable — upgraded July 2024 |

| Florida Relevance | Significant Florida property cat exposure; automated hurricane damage detection technology; broad treaty and proportional program capacity for Florida-based cedents |

Swiss Re

Swiss Re is a leading global reinsurer with deep U.S. operations and one of the broadest risk transfer platforms in the Florida market. Alongside traditional treaty reinsurance, Swiss Re is a major participant in the insurance-linked securities (ILS) and catastrophe bond markets — a structurally distinct channel that gives Florida-exposed cedents access to capital market capacity beyond rated carrier balance sheets.

Florida's Citizens Property Insurance Corp. has used cat bond vehicles like "Everglades Re" to transfer hurricane risk to capital markets, a structure where Swiss Re's ILS expertise is directly applicable.

| Category | Details |

|---|---|

| Focus Areas | Property and casualty treaty/facultative reinsurance, life and health reinsurance, ILS and catastrophe bonds |

| AM Best Rating | A+ (Superior), Stable |

| S&P Rating | AA- (Very Strong), Stable — affirmed November 2025 |

| Florida Relevance | Active in ILS/cat bond structures for Florida hurricane risk; Hurricane Ian cat bond analysis published February 2024; provides alternative risk transfer alongside traditional treaty capacity |

RenaissanceRe (RenRe)

RenaissanceRe has a founding story that's inseparable from Florida's catastrophe history. The company was established in June 1993 directly in response to Hurricane Andrew — the event that forced the industry to confront a systematic underpricing of catastrophe risk. RenRe pioneered sophisticated computer modeling for cat risk pricing and has remained one of the most important reinsurers of Florida hurricane exposure ever since.

In September 2024, the Florida Office of Insurance Regulation approved Renaissance Reinsurance Ltd. as the 10th reinsurer under Florida's modified collateral requirements — a milestone that expands its capacity to participate in Florida's catastrophe market with reduced collateral posting requirements.

| Category | Details |

|---|---|

| Focus Areas | Property catastrophe reinsurance (founding core business), casualty and specialty reinsurance, professional liability |

| AM Best Rating | A+ (Superior), Stable — affirmed October 2025 |

| S&P Rating | A+ — Positive outlook (potential upgrade indicated) |

| Florida Relevance | Founded specifically in response to Hurricane Andrew; FL OIR modified collateral approval September 2024; quantitative cat modeling expertise built around Florida exposure |

Everest Re Group

Everest Re is a diversified global reinsurer and insurer with significant U.S. property and casualty operations, including active participation in Florida's catastrophe reinsurance market. The company reported pretax catastrophe losses of $1.2 billion (net of reinsurance) in Q3 2017 — driven largely by Hurricanes Harvey, Irma, and Maria — illustrating its meaningful Florida exposure.

Important caveat: Both AM Best and S&P revised Everest Re's outlook to negative in 2025 following $1.7 billion in net reserve strengthening on U.S. casualty lines. The A+ rating remains affirmed, but cedents placing new programs should monitor reserve adequacy developments — particularly for casualty lines.

| Category | Details |

|---|---|

| Focus Areas | Property catastrophe reinsurance, casualty treaty and facultative, unified global specialties (established 2024) |

| AM Best Rating | A+ (Superior), Negative Outlook |

| S&P Rating | A+, Negative Outlook — revised January 2025 |

| Florida Relevance | Active Florida property cat writer; consistent market presence through hard and soft cycles; casualty reserve concerns are in U.S. lines, not property cat |

TransRe (Transatlantic Holdings)

TransRe — the operating brand for Transatlantic Holdings, Inc. — is a wholly owned subsidiary of Alleghany Corporation, which became part of Berkshire Hathaway in October 2022. That ownership structure is directly reflected in its ratings: TransRe carries AM Best A++ (Superior) and S&P AA+ — the highest financial strength ratings of any reinsurer on this list.

Founded in 1977 and headquartered in New York, TransRe offers treaty and facultative reinsurance across property, casualty, and specialty lines. Its facultative capabilities are particularly relevant for individual large or complex Florida property risks that fall outside standard treaty terms.

| Category | Details |

|---|---|

| Focus Areas | Property catastrophe treaty and facultative, casualty, specialty reinsurance |

| AM Best Rating | A++ (Superior), Stable — highest available rating |

| S&P Rating | AA+ (Very Strong), Stable |

| Florida Relevance | Broker-intermediated placements for Florida-based cedents; facultative capabilities for individual complex Florida risks; Berkshire Hathaway financial backing provides unmatched counterparty credit quality |

What Florida Auto Dealers Should Know About Reinsurance

The reinsurers above serve primary insurance carriers — not auto dealerships. Munich Re and Swiss Re aren't writing dealer service contracts or GAP coverage for Florida car buyers. Their clients are insurance companies.

Florida auto dealers have access to an entirely different reinsurance structure, and it's one of the most profitable opportunities many dealers aren't yet using.

How Dealer-Owned Reinsurance Works

When a dealership sells F&I products — service contracts, GAP, collateral protection insurance — through a third-party provider, the dealer earns the front-end gross profit. The third-party company keeps the rest: the underwriting profit on premiums that exceed claims costs.

Consider the math. F&I gross profit per vehicle retailed reached $2,505 in Q1 2025 at publicly owned U.S. dealerships — up for four consecutive quarters — and F&I now represents approximately 73% of total dealership profit. That's a massive premium volume flowing through every F&I office, and a significant share of it currently leaves the dealership.

An administrator obligor reinsurance company puts that profit back in the dealer's hands. Instead of sending premiums to a third-party provider, the dealer establishes their own reinsurance company that receives those premiums and captures 100% of the underwriting profit as policies expire.

Key benefits for Florida dealers:

- Retain underwriting profits on service contracts, GAP, CPI, and ancillary products

- Tax planning advantages under IRC Section 831(b) — qualifying companies are taxed only on investment income, not underwriting profits

- Control over the claims experience — driving service work back to your facility

- Ability to invest accumulated premiums for additional ROI

- Use earned income to fund real estate, college savings, watercraft, or direct dealership reinvestment

Why Florida's Market Makes This Especially Valuable

Those mechanics apply anywhere — but Florida's scale amplifies the opportunity. The state is one of the country's largest auto markets, with high vehicle sales volumes and a significant BHPH segment. More volume means more F&I contracts sold, more premiums flowing into the dealer's own reinsurance company, and more underwriting profit to capture.

BHPH dealers in Florida benefit from an additional structural advantage: DealerRE's program allows premiums to be billed monthly as customer payments are received, rather than requiring large upfront payments that strain cash flow and lending pools.

DealerRE's Role for Florida Dealers

Since 1994, DealerRE has helped over 400 auto dealers nationwide — including dealers across Florida — establish and manage their own admin obligor reinsurance companies. The company handles everything dealers don't want to manage themselves:

- Full legal setup and entity filing

- Compliance management and state contract approvals

- Claims adjudication through experienced administrators

- Tax preparation and annual filings (Form 1120PC)

- F&I training — online and in-person — to improve product penetration

- Monthly financial statements and performance reporting

As DealerRE founder Tim Byrd frames it: if your third-party warranty provider weren't profiting from your dealership, they'd have no reason to keep doing business with you. The program exists to put that profit where it belongs — with the dealer.

How We Chose the Best Reinsurance Companies in Florida

The reinsurers on this list were evaluated on four criteria:

- Financial strength ratings — AM Best and S&P ratings indicate whether a reinsurer can actually pay claims. The industry minimum is AM Best A- or better. Every company above meets or exceeds that threshold.

- Active Florida market presence — national operations aren't enough. Each company listed has meaningful Florida exposure, either through direct Florida regulatory approvals or substantial property cat books that necessarily include Florida risk.

- Specialization in Florida-relevant lines — property catastrophe, casualty, and specialty lines are the primary reinsurance needs of Florida-based cedents.

- Market reputation — broker and cedent experience matters, particularly during difficult claims periods.

Common mistakes to avoid when selecting a reinsurance partner:

- Choosing brand recognition over ratings — a well-known name with a negative outlook isn't the same as a financially stable one

- Ignoring the distinction between treaty and facultative capabilities — Florida's complex property risks often require facultative placement

- Conflating traditional property-casualty reinsurance with dealer-owned F&I reinsurance programs — they serve different purposes and client types, and evaluating them on the same criteria leads to poor decisions

With those criteria in mind, here's a closer look at the top reinsurance company offices operating in Florida today.

Conclusion

Florida's reinsurance market ranks among the most sophisticated in the world. The companies on this list — Munich Re, Swiss Re, RenaissanceRe, Everest Re, and TransRe — represent the highest tier of global reinsurance capacity, each with specific strengths relevant to Florida's hurricane-exposed, litigation-heavy risk environment. Selecting the right partner comes down to ratings first, then a clear understanding of your cedent's specific exposure.

That calculus looks different for auto dealers. The most profitable reinsurance opportunity isn't a treaty with a Bermuda-based catastrophe reinsurer — it's a dealer-owned program that keeps F&I underwriting profits inside your business instead of sending them to third parties.

If you're a Florida auto dealer and want to understand what that could look like for your operation, contact DealerRE. Full-service administration, no hidden fees, and a team that has helped over 400 dealers build and manage their own programs since 1994.

Frequently Asked Questions

What exactly does a reinsurance company do?

A reinsurance company assumes a portion of the risk a primary insurer has underwritten, in exchange for a share of the premium. This allows the primary insurer to expand capacity, stabilize earnings, and protect against catastrophic losses that would otherwise exceed its capital reserves.

Are there reinsurance companies specifically for auto dealers in Florida?

Traditional reinsurers like Munich Re and Swiss Re serve primary insurance carriers, not dealerships. Florida auto dealers access reinsurance through dealer-owned programs — where the dealer's own reinsurance company receives premiums from F&I product sales rather than sending those profits to a third-party provider. Administrators like DealerRE specialize in setting up and managing exactly these types of programs for dealerships nationwide.

What is the difference between treaty and facultative reinsurance?

Treaty reinsurance covers a defined class of business automatically — for example, all of an insurer's property policies. Facultative reinsurance is negotiated individually for specific large or unusual risks. Most Florida property catastrophe reinsurance is placed on a treaty basis.

How do reinsurance companies handle Florida hurricane risk?

Major reinsurers use sophisticated catastrophe models to price and manage Florida hurricane exposure. Coverage is typically placed in layers through broker intermediaries, with each layer protecting Florida-based insurers from losses above a defined retention threshold.

What financial ratings should I look for when evaluating a reinsurance company?

Check AM Best and S&P Global ratings. An AM Best rating of A- (Excellent) or better is the widely accepted minimum for a reinsurance counterparty — it confirms the reinsurer has sufficient financial capacity to pay claims. Also check whether the outlook is stable, positive, or negative.

Can an auto dealer in Florida set up their own reinsurance company?

Yes — and it's more common than many dealers realize. Working with a reinsurance administrator, Florida dealers can establish their own company to capture the underwriting profits from F&I product sales instead of paying a third-party provider. Setup, compliance, and administration are typically handled by the administrator.