Introduction

Most auto dealers never think about reinsurance until something forces the issue — a third-party provider exits their market, a warranty program reprices, or a colleague mentions capturing underwriting profits directly. That's exactly when understanding how the broader reinsurance market operates starts to matter.

When a reinsurer the size of AXA XL restructures its global operations, the effects reach across the entire insurance market: from Lloyd's syndicates to the F&I offices of dealerships nationwide. Reinsurance is the financial infrastructure behind virtually every insurance product sold anywhere.

This article covers who AXA XL is, what their recent structural changes mean, and why auto dealers should pay attention to the broader reinsurance market — even when their own programs look nothing like catastrophe coverage.

TLDR

- AXA XL is AXA's global commercial P&C and reinsurance division, formed via a $15.3 billion acquisition of XL Group in 2018

- "XL" traces to EXEL Limited (1986), founded to provide excess liability coverage — and "XL" as a product type means excess of loss reinsurance

- AXA XL reported €1.4 billion in reinsurance premiums in Q1 2025, up 12% year-over-year

- In 2025, AXA unified its ceded reinsurance teams into a single global structure to streamline oversight and eliminate redundant functions

- For auto dealers, admin obligor reinsurance is a profit-retention tool — it captures underwriting income from F&I products rather than transferring catastrophe risk to a carrier

What Is AXA XL? A Brief History

AXA XL is the global commercial property and casualty arm of AXA, the French insurance giant. Headquartered in Stamford, Connecticut and domiciled in Bermuda, the company operates from more than 100 offices across six continents, serving clients in over 200 countries. With roughly 7,400 employees and a Q1 2025 premium base of nearly €7 billion, it ranks among the largest commercial lines insurers and reinsurers in the world.

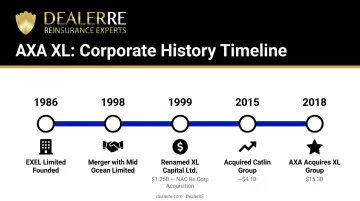

From EXEL Limited to XL Group

The company's origins go back to 1986, when 68 Fortune 500 companies created EXEL Limited in the Cayman Islands. The early 1980s had produced a severe commercial liability insurance shortage, and large corporations needed a way to access excess liability capacity the standard market couldn't provide. EXEL was that vehicle. Both EXEL and Mid Ocean Limited re-domiciled to Bermuda in 1990.

Several major transactions shaped the company's growth over the following three decades:

| Year | Event | Value |

|---|---|---|

| 1998 | EXEL Limited merges with Mid Ocean Limited | Not publicly specified |

| 1999 | Company renamed XL Capital Ltd. | — |

| 1999 | Acquired NAC Re Corp | $1.25 billion |

| 2015 | Acquired Catlin Group | ~$4.1 billion |

| 2018 | AXA acquired XL Group | $15.3 billion |

The 2018 AXA acquisition reshaped the business entirely. AXA combined XL Group with its existing operations to create the AXA XL brand, folding one of the world's largest reinsurers into an even larger global insurance group.

Current Business Mix

Per AXA's Q1 2025 activity indicators, AXA XL's premiums break down as follows:

- Insurance: €5.5 billion (~79% of total)

- Reinsurance: €1.4 billion (~21% of total)

- Life & Health: €32 million

Reinsurance is the smaller segment by premium volume, but it carries outsized strategic importance. It's also the part of the business that's been most actively restructured.

What Does "XL" Mean in Reinsurance?

This question comes up often, and there are two correct answers depending on what you're asking.

The Brand Origin

"XL" in AXA XL traces directly to EXEL Limited — the 1986 entity whose name stood for excess liability. When EXEL merged with Mid Ocean and became XL Capital Ltd. in 1999, the abbreviation carried forward. It was never a generic descriptor. It reflected a specific founding purpose: providing excess liability capacity that the standard insurance market had stopped offering.

The Product Category

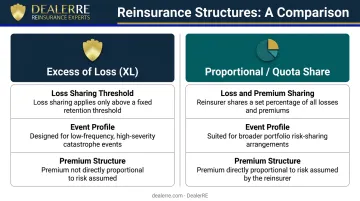

Separately, "XL" in reinsurance parlance refers to excess of loss coverage — a distinct structure where the reinsurer's obligation only begins once losses exceed a defined retention threshold. The International Risk Management Institute defines excess of loss reinsurance as "a generic term for all forms of reinsurance under which the reinsurer pays the excess over a fixed amount (retention) of the primary company's loss."

Here's how excess of loss compares to proportional reinsurance:

| Feature | Excess of Loss (XL) | Proportional / Quota Share |

|---|---|---|

| Loss sharing | Reinsurer pays only above a fixed retention | Reinsurer shares a set % of all losses and premiums |

| Typical use | Low-frequency, high-severity events | Broader portfolio risk-sharing |

| Premium basis | Not directly proportional | Proportional to risk assumed |

Excess of loss structures are most common in catastrophe coverage — hurricanes, earthquakes, large casualty events. They protect primary insurers from low-frequency, high-severity losses that would otherwise blow through their balance sheets.

That catastrophe-protection context matters when auto dealers evaluate their own reinsurance options. Dealer-owned reinsurance serves a fundamentally different purpose: retaining the underwriting profit generated by F&I product sales rather than shielding a balance sheet from low-frequency disasters. The structure, the motivation, and the financial outcome are distinct.

AXA XL's Recent Restructuring: Key Developments in 2024 and 2025

Three significant organizational moves have reshaped AXA XL's reinsurance operations over the past year.

China Rebrand (October 2024)

Effective October 16, 2024, XL Reinsurance (China) Company Limited was officially renamed AXA International Reinsurance (Shanghai) Company Limited following approval from China's National Financial Regulatory Administration. The move was designed to align the China entity with the AXA brand globally and signal a long-term commitment to mainland Chinese reinsurance markets.

Unified Ceded Reinsurance Team (July 2025)

On June 24, 2025, AXA announced the combination of the AXA Group and AXA XL Ceded Reinsurance teams into a single unified structure, effective July 1, 2025. Guy Van Hecke leads the combined team in a dual capacity — reporting to Group CUO Nancy Bewlay, with a matrix line to AXA XL CEO Scott Gunter.

The four stated objectives for the combined team:

- Establish a consistent ceded reinsurance strategy across AXA Group

- Capture One AXA synergies by reducing duplication

- Streamline communication with reinsurance market partners

- Optimize governance across global operations

As Van Hecke put it: "By bringing these teams together, we are creating a more integrated and agile Ceded Re structure that will strengthen our partnerships globally... reduce duplication, enhance market presence, and ensure seamless communication across our global operations."

North America Leadership (Late 2024 – Early 2025)

AXA XL made two key appointments to accelerate its North America growth strategy:

- Greg Schiffer named CEO of AXA XL Reinsurance for North America (effective November 11, 2024), joining from Swiss Re

- Simon Rees appointed CUO for North America Programs (effective April 1, 2025), focused on specialty program capabilities

The Rees appointment is directly relevant for program administrators and dealers — it targets growth in specialty and program business, which overlaps with the F&I product reinsurance space.

AXA XL's Scale and Ratings

AXA XL Re holds some of the strongest financial ratings in the reinsurance market:

| Agency | Rating |

|---|---|

| AM Best | A+ (Superior) |

| S&P Global | AA- |

| Moody's | A2 |

These ratings reflect both balance sheet strength and AXA XL Re's strategic position within the AXA Group, which reported net income of €8.1 billion in 2024. For buyers evaluating counterparty risk, the ratings signal a reinsurer with the financial depth to pay claims through extended loss periods.

Reinsurance premiums reached €1,439 million in Q1 2025 (12% growth year-over-year), driven by ILS business and favorable casualty pricing. Through H1 2025, AXA XL reinsurance growth held at 11%.

What This Signals for the Market

According to Guy Carpenter's January 2025 renewal analysis, total dedicated reinsurance capital reached $607 billion — up 6.9% — with property catastrophe renewals oversubscribed. Reinsurer ROE for 2024 projected at 17.3%.

Three signals define where the market currently stands:

- AM Best shifted its global reinsurance outlook from positive to stable in early 2026, driven by accelerating property pricing softening

- Casualty excess of loss placements continue facing treaty-term pressure at renewals

- Capital remains abundant, but disciplined pricing is now the dominant force in placement decisions

For businesses that rely on reinsurance-backed programs, capacity isn't the concern right now — pricing discipline is.

What Auto Dealers Should Know About Reinsurance

Global reinsurers like AXA XL operate in a world of catastrophe risk, casualty clash, and cross-border treaty structures — none of which has much bearing on what a dealership's F&I office actually needs.

Dealers aren't buying hurricane protection. They're selling vehicle service contracts, GAP, collateral protection, and ancillary products — and most of them are watching the underwriting profit from those sales flow out the door to third-party providers.

The Admin Obligor Structure

Through a dealer-owned admin obligor reinsurance program, a dealer establishes their own reinsurance company to capture 100% of the underwriting profit that would otherwise go to external providers. A-rated carriers back the structure, so there's financial protection — and the profit stays with the dealer.

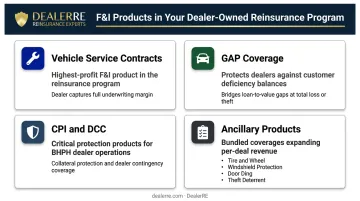

Products typically covered through this structure include:

- Vehicle Service Contracts (VSCs) — typically the highest-profit F&I product in a dealer-owned program

- GAP coverage, which protects customers from deficiency balances on total losses

- Collateral Protection Insurance (CPI) and Debt Cancellation Coverage (DCC) — both critical for BHPH dealers

- Ancillary products: tire and wheel, windshield repair, door ding, theft protection

Unlike pooled third-party arrangements, the dealer reinsures only their own book — meaning claims performance reflects your F&I operation directly, not another dealer's.

Tax Planning Advantage

Dealer-owned reinsurance companies structured under IRS Code Section 831(b) may elect to be taxed only on investment income — not underwriting profits — when annual net premiums stay below $2.2 million. Third-party arrangements offer no equivalent tax treatment.

DealerRE

DealerRE has helped over 400 dealers nationwide establish and manage their own admin obligor reinsurance programs since 1994. Services include compliance management, claims adjudication, financial reporting, tax filings, and F&I training — both online and in person. Dealers selling 30+ vehicles per month are typically strong candidates for a dealer-owned program.

Frequently Asked Questions

What is XL in reinsurance?

"XL" in AXA XL traces to EXEL Limited, a 1986 company whose name stood for excess liability. As a product category, "XL" refers to excess of loss reinsurance — coverage that kicks in only after losses exceed a defined retention threshold, typically used for catastrophic or low-frequency, high-severity events.

What is AXA XL's financial strength rating?

AXA XL holds an A+ (Superior) Financial Strength Rating from AM Best, an AA- from S&P Global, and an A2 from Moody's. These ratings reflect strong balance sheet strength and AXA XL's core strategic importance within the AXA Group, which reported €8.1 billion in net income in 2024.

How did AXA come to own XL Group?

AXA completed its acquisition of XL Group in September 2018 for $15.3 billion, combining it with AXA's existing commercial lines capabilities to create AXA XL as its global commercial P&C and reinsurance division.

What does AXA XL's 2025 restructuring mean for policyholders and cedents?

The consolidation of AXA Group and AXA XL Ceded Re teams is an internal operational move to reduce duplication and unify ceded reinsurance strategy. For cedents, it means a single point of contact and more consistent communication going forward.

Can auto dealers set up their own reinsurance company instead of relying on third-party providers?

Yes. Through a dealer-owned admin obligor reinsurance structure, dealers can establish their own reinsurance entity to retain 100% of the underwriting profit from F&I product sales. DealerRE helps dealers structure, launch, and manage these programs — covering compliance, claims adjudication, and financial administration from day one.