Car buyers arrive more informed and more skeptical than ever. Margins are compressing. The digital shift has moved the F&I conversation earlier in the buying journey, often before a customer sets foot in your showroom. Dealers who haven't adapted their marketing and presentation approach are leaving real money on the table.

This article covers six actionable strategies to improve F&I product marketing: building staff confidence through training, integrating F&I into the digital buying journey, using presentation techniques that convert, perfecting the sales handoff, tracking the right metrics, and recovering revenue through post-sale follow-up.

TLDR

- Train F&I staff to explain product value with real-world scenarios, not scripted recitations

- Surface F&I product info online before buyers visit — 82% of shoppers already recognize VSCs and GAP

- Use a needs-based interview to lead with 2-3 relevant products per customer, not the full menu

- Align sales and F&I teams so customers arrive prepared, not defensive

- Monitor PVR, PPD, and penetration rates by manager, deal type, and product to find gaps

- Follow up post-sale to recover 35-45% of customers who initially declined

Train Your Team to Sell F&I Products With Confidence

F&I marketing begins with the person delivering it. A manager who can't clearly explain how a vehicle service contract works — or why it matters for a customer keeping their truck for five years — projects uncertainty. Customers notice, and they disengage.

What Product Knowledge Actually Looks Like

Effective product knowledge isn't memorizing a brochure. It means being able to answer three questions for every product:

- Explain coverage, exclusions, and the claims process in plain language — not brochure language

- Quantify the cost of skipping it: a transmission replacement runs $4,000–$6,000, which reframes a $30/month VSC payment entirely

- Share real claim scenarios — even anonymized ones — to make abstract coverage tangible

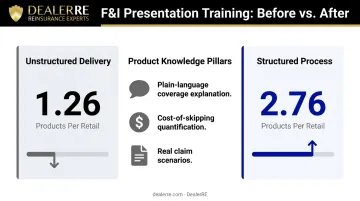

Research from Vision Management Group documented that dealerships using a structured, repeatable presentation process increased products per retail from 1.26 to 2.76. That improvement came from better delivery, not better products.

Training Cadence Matters More Than Volume

One-time onboarding doesn't hold. High-performing F&I operations treat training as an ongoing operational discipline, not an event. Vision Management recommends daily 10-15 minute huddles focused on deal reviews and skill application alongside a 90-day rollout plan for new processes.

F&I managers face objections daily. Rehearsing responses quarterly means defaulting to weak habits under pressure — exactly when it counts most. Regular role-playing, live deal coaching, and objection drills build the muscle memory that holds up in a real conversation with a skeptical buyer.

Using a Framework vs. Starting from Scratch

Dealers who partner with structured F&I support providers get a significant head start. DealerRE offers F&I training classes in both online and in-person formats, along with customized F&I menus through their training academy. That kind of ready-made framework — built around real dealership workflows — means staff aren't figuring out presentation structure on their own.

The NIADA has noted that approximately 80% of F&I customers are persuadable — they'll listen and negotiate when approached well. For dealers looking to move that needle, staff skill and confidence are the most direct levers available, which is exactly what a structured training framework is built to develop.

Integrate F&I Into the Digital Buying Journey Early

By the time a customer walks into your F&I office, they've already formed an opinion about whether they want protection products. That opinion formed online, days or weeks ago — and your dealership either influenced it or missed the window entirely.

The Pre-Visit Reality

A 2024 Protective Asset Protection survey of over 300 recent car shoppers found:

- 82% were already familiar with F&I products before visiting the dealership

- 57% prefer to research F&I products online and buy in-store

- 30% want to research and purchase entirely online

- Among Gen Z buyers, 34.9% said convenience of research was the single biggest factor in their F&I purchase decision

These buyers aren't waiting for your F&I office pitch to start forming opinions. They're forming them on your website — or your competitor's.

That data points directly to where dealerships should act. Here's how to meet buyers where they already are.

How to Surface F&I Information Early

On your website:

- Add product overview pages for VSCs, GAP, and prepaid maintenance alongside vehicle listings

- Frame these as ownership tools, not add-ons — "what protects your investment after you drive home"

- Include FAQs and short explainer videos customers can watch at their own pace

In the showroom:

- Use mobile-friendly or tablet-based interactive menus during the pre-F&I wait period

- Over 70% of automotive shoppers use a mobile device at some point in their buying journey (DemandLocal, 2025) — digital presentation tools aren't optional; they're what buyers already expect

Dealerships that invest in pre-visit digital education reach customers before objections solidify. When a buyer already understands what a VSC covers, the F&I conversation shifts from explanation to decision — and that's where close rates improve.

Use Proven Presentation Strategies to Convert More F&I Sales

A scripted rundown of every available product at full price is the fastest way to lose a customer's attention. Today's buyers expect relevance, not a catalog reading.

Start With a Needs Interview

Before opening a menu, F&I managers should spend 2-3 minutes gathering context:

- How long do they plan to keep the vehicle?

- Do they do their own maintenance or rely on a shop?

- What's their comfort level with unexpected repair costs?

- Are they concerned about negative equity?

These answers determine which 2-3 products to lead with. A customer planning to keep a used vehicle for 7 years with no emergency fund is a strong VSC candidate. Someone financing a new vehicle at 110% LTV needs to hear about GAP first. The menu should follow the discovery, not precede it.

Structured Menu Presentation

Industry trainers across multiple frameworks recommend organizing menu options into 3-4 tiered columns — typically a fully-loaded package, a mid-tier option, a basic option, and a decline column. The goal is giving customers a choice of how much protection, not a yes/no on each individual product.

The "3-3-3" framework — roughly 3 products, 3-4 minutes, 3 payment tiers — reflects principles consistent across most F&I training programs: limit products per presentation, keep the timing tight, and anchor to payment columns rather than lump sums.

Payment Framing vs. Lump Sum

The Protective survey found 18.5% of consumers cited monthly payment as their top F&I purchase factor. Presenting a VSC as "this adds about $22 to your monthly payment" is fundamentally different from presenting it as a $1,800 line item. One fits inside the payment conversation they're already having. The other triggers sticker shock.

Customizing menu presentation by deal type makes this even more effective:

- Used vehicles: Lead with VSC and tire/wheel protection

- New financed deals: Lead with GAP when LTV is high

- Long-term owners: Emphasize service contract term length and coverage depth

- EV buyers: Prioritize battery, charging, and technology coverage — gaps standard VSCs often miss

Perfect the Sales-to-F&I Handoff

A weak handoff is the most overlooked cause of F&I resistance. Customers who weren't told to expect a finance conversation — or who were told "it'll just take a minute" by a salesperson — arrive in the F&I office guarded and annoyed before the manager says a word.

What a Strong Handoff Looks Like

The salesperson's job isn't to sell F&I products — it's to create the conditions where the F&I manager can. That means covering four basics:

- Set expectations early: Tell the customer that a finance specialist will walk them through payment options and ownership protection programs

- Qualify naturally: Ask about financing preference, how long they plan to keep the vehicle, and whether they've dealt with unexpected repair bills

- Avoid negative framing: Phrases like "they'll try to sell you warranties in there" poison the handoff and send the customer in pre-objecting

- Transfer warmth: Introduce the F&I manager by name and pass along context — "She knows you're planning to keep this truck long-term"

Vision Management notes that when salespeople lack finance literacy, they often make payment promises that box deals into structures where there's no room for F&I products. Training the sales floor on basic deal structure — and tying incentives to product penetration, not just unit sales — closes that gap and breaks the siloed mentality where salespeople treat F&I as someone else's problem.

Track the Right F&I Metrics to Sharpen Your Marketing Strategy

Knowing which numbers to watch — and how to read them — is what separates reactive F&I management from a strategy that actually improves results. Three metrics form the core of any F&I performance review:

| Metric | National Benchmark | Notes |

|---|---|---|

| Per Vehicle Retail (PVR) | $1,700–$1,900 average | Top groups average $2,505+ |

| Products Per Deal (PPD) | 1.58 (Q4 2025) | Up from 1.53 in Q4 2024 |

| VSC Penetration | ~46–48% | Highest penetration product |

| GAP Penetration | ~30% | Varies by deal type and LTV |

Source: StoneEagle F&I Benchmark Report Q4 2025 and Brady Ware 2024

Segment to Find the Real Gaps

Aggregate numbers hide specific problems. An F&I manager who averages 1.6 PPD may be hitting 55% VSC penetration and 15% GAP penetration. That's not an overall performance issue — it's a targeted gap in how they're presenting GAP, and it points directly to a specific training conversation.

Segment your metrics by:

- Each F&I manager's product-level penetration rates, not just their overall PPD

- Deal structure — finance, lease, used, and BHPH each carry different product fit profiles

- Vehicle category — new, certified pre-owned, and high-mileage used have different VSC and GAP dynamics

Dealers who structure their F&I programs through a dealer-owned reinsurance company gain an additional layer of insight. Through DealerRE's full-service administration, dealers receive performance reports and claims data showing which products generate underwriting profit and which may need re-evaluation or repricing.

That level of product-specific visibility is only possible when you own the program structure. When a third party controls it, that data stays on their side of the table.

Recover Lost Revenue With Post-Sale Follow-Up

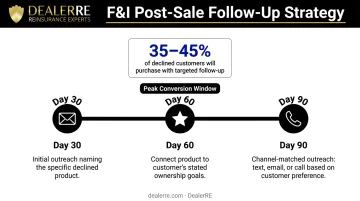

Declined F&I products aren't necessarily lost forever. A customer who said no to a VSC at the desk is in a different headspace 60 days later — after the first bill arrives, the payment routine sets in, and a friend's $3,000 repair bill becomes a dinner table story.

According to StoneEagle's 2025 data, 35-45% of customers who decline F&I products at the desk would purchase at least one product if contacted with targeted follow-up within 90 days. Dealerships using automated post-sale outreach reportedly recover 20% or more in additional back-end revenue.

Building an Effective Follow-Up Cadence

Structure outreach at 30, 60, and 90 days post-sale. The 60-day mark is reportedly the most effective conversion window.

What separates effective follow-up from generic solicitation:

- Name the specific product they passed on — "When you were here, you declined the extended service contract for the F-150"

- Connect it to something they told you — "You mentioned keeping it 5+ years; here's coverage built for that timeline"

- Match the channel to the customer — text for quick responses, email for detail-oriented buyers, a short call for high-ticket products

This turns follow-up from a broadcast into a continuation of the original conversation — and for dealers running their own reinsurance programs, every recovered sale adds directly to the underwriting profit they're already building.

Frequently Asked Questions

What is the most effective way to market F&I products to car buyers?

The most effective approach combines early digital education — putting product information on your website before the visit — with a personalized, needs-based presentation in the F&I office, and a sales handoff that sets positive expectations. All three elements require consistent staff training to execute reliably.

What is the 3-3-3 rule for marketing F&I products?

The 3-3-3 rule is an informal presentation framework used across the industry: present 2-3 relevant products, within a 3-4 minute window, across tiered payment columns. The structure keeps decisions manageable and reduces customer overwhelm at the F&I desk.

What F&I products are easiest to sell?

Vehicle service contracts and GAP insurance consistently post the highest penetration rates — VSCs hover around 46-48% and GAP around 30%. Both are easiest to sell when tied to a specific customer concern: repair cost exposure on a used vehicle, or negative equity risk on a financed deal with a low down payment.

How can the sales team help sell more F&I products?

Salespeople help most by setting expectations before the handoff (mentioning that a finance specialist will cover protection options) and asking qualifying questions about ownership plans and repair concerns. Avoiding negative framing around "add-ons" matters just as much.

What role does technology play in marketing F&I products?

Mobile-friendly menus, digital product overview pages, and tablet-based showroom presentations reduce friction and let customers explore options before formal pricing discussions. With over 70% of car shoppers using mobile devices during the buying process, digital F&I touchpoints are a practical baseline, not an upgrade.

How does owning your F&I program affect your ability to market F&I products?

Dealers who control their own F&I product structure (through a dealer-owned reinsurance company like those DealerRE facilitates) can offer more customized, competitively priced products and retain the underwriting profits that third-party providers would otherwise capture. That ownership also enables data-driven decisions about which products to prioritize, based on actual claims performance.