Introduction

Front-end gross profits are compressing. New vehicle gross profit per vehicle retailed dropped to $3,135 in Q1 2025 — a 14.4% year-over-year decline, continuing a trend that's been grinding downward for years. For dealers who haven't fully optimized their F&I departments, that compression is starting to hurt.

The good news: F&I is one profit center that responds directly to process discipline, not inventory cycles or manufacturer incentives. Dealers who treat it that way consistently outperform those who don't.

This guide covers the levers that matter most: standardizing your process, optimizing your product mix, aligning your whole dealership, tracking the right KPIs weekly, and — the layer most dealers overlook — recapturing the underwriting profits that currently flow straight to your third-party F&I product providers.

TLDR

- Standardize menu presentation — 100% of customers, no exceptions, every time

- Track three weekly KPIs: F&I PVR, VSC/GAP penetration, and chargeback trends

- Align your sales team around a scripted, non-negotiable F&I handoff

- Focus your product mix on high-penetration, high-margin products — VSCs and GAP lead, ancillaries add depth

- Dealer-owned reinsurance captures the underwriting profits your third-party providers keep — the biggest untapped revenue layer for most dealers

Why F&I Is the Dealership's Most Reliable Profit Center

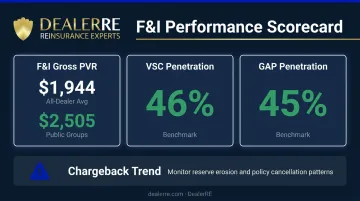

F&I gross profit for public dealer groups hit $2,505 PVR in Q1 2025 — within 4% of the all-time high of $2,603 set in Q3 2022. Meanwhile, the all-dealer average reached a record $1,944 PVR in November 2024. That $560 gap between the all-dealer average and what public groups are earning tells you something: there's significant upside still on the table for independent and mid-size franchise dealers who get their process right.

What makes F&I structurally different from front-end gross is its resilience. New vehicle margins fluctuate with inventory constraints, manufacturer incentives, and consumer demand cycles — none of which you control. F&I performance is driven by process discipline, product execution, and staff training — factors that sit entirely within your control.

F&I's share of total dealership gross profit grew from 18.8% in 2007 to 25.5% by 2019, and that trend has only intensified as vehicle margins have normalized post-pandemic. For most dealerships today, F&I is no longer supplemental income — it's the margin that separates a profitable year from a break-even one.

Standardize Your F&I Process for Consistent Results

The most common F&I profit killer isn't a bad market or a tough customer — it's inconsistency. When each manager "does it their own way," results swing based on individual personality rather than a repeatable system. One top performer goes on vacation and PVR drops 30%. The culprit isn't the person — it's the absence of a system that works without them.

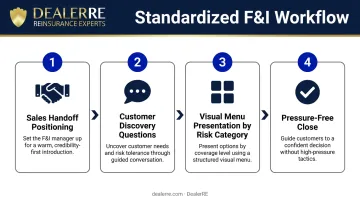

What a Standardized F&I Workflow Looks Like

A well-built process covers four stages:

- Position the F&I manager during the sales handoff as someone who protects the customer's investment — not a paperwork clerk. The handoff language matters (more on this below).

- Ask two or three questions about how the customer uses the vehicle. This feeds directly into the product presentation and makes the conversation feel personalized rather than scripted.

- Present products grouped by risk category, displayed visually, with each option connected back to something the customer actually said.

- Close without pressure — clear product explanations, no manipulation, and a pace that respects the customer's time.

The 100% Menu Presentation Rule

Dealerships running 100% menu presentation report 2.3x product penetration and $687 more PVR per retail unit compared to those that don't. That gap is almost entirely explained by one habit: pre-judging which customers will buy.

Cash buyers, subprime customers, first-time buyers, repeat loyalists — all of them get the menu. The moment your F&I managers start deciding who's worth pitching, a significant chunk of potential PVR walks out the door.

Continuous Coaching, Not One-Time Training

One-time training events produce a short spike and then reversion. The dealerships that sustain high F&I performance build ongoing coaching habits instead:

- 10–15 minutes of roleplay, a few times a week

- Weekly deal reviews tied directly to KPI data

- Targeted practice focused on the specific gap — if GAP penetration dropped this week, drill that conversation, not a generic refresher

Tying practice to live performance data produces faster, more durable improvement than any offsite event.

Identify the Key F&I KPIs to Track Weekly

A one-page scoreboard reviewed in a 15-minute weekly huddle outperforms a complex monthly report. Keep it to three metrics:

| KPI | Industry Benchmark | What It Tells You |

|---|---|---|

| F&I Gross PVR | $1,944 (all-dealer avg) / $2,505 (public groups) | Overall department health |

| VSC Penetration | 46% | Product execution on core offering |

| GAP Penetration | 45% | Second core product performance |

Round out your dashboard with a chargeback/cancellation trend as a fourth data point. One F&I manager averaging $1,600 PVR discovered that 18% of their deals were being canceled — dramatically eroding their effective profitability. They initially blamed their customer base. The root cause was process and product selection.

How to run the weekly huddle:

- Review each metric vs. the prior week

- Identify the one metric that moved in the wrong direction

- Set one specific improvement focus for the coming week

- Practice that piece of the conversation before the huddle ends

The goal is a short, consistent rhythm — same metrics, same questions, every week — so small problems get caught before they compound.

Optimize Your F&I Product Mix and Presentation

Know Your Product Priorities

Based on data from 6,000+ dealerships, here's where penetration benchmarks currently stand:

- VSCs: 46% average penetration — the single largest F&I revenue driver at 54% of total F&I product revenue

- GAP: 45% average penetration — accounts for 12% of revenue but high margin per deal

- Prepaid maintenance: 17% average penetration — lower penetration but easy to present

- Ancillary products (tire/wheel, appearance, windshield): gaining traction as bundled offerings across dealer groups

Focus your menu on fewer products presented well, not every option available. A customer presented with six products and no context buys nothing. A customer presented with three products tied directly to their situation buys two.

Features-Based vs. Needs-Based Presentation

A features-based pitch describes what the product covers. A needs-based presentation connects the product to what the customer already told you.

- ❌ "This VSC covers 2,000+ components and includes roadside assistance..."

- ✅ "You mentioned you commute 45 minutes each way — here's how a VSC protects you when something comes up between service visits..."

The second version doesn't feel like a sales pitch. It feels like advice. That shift in framing consistently improves both acceptance rates and customer satisfaction scores.

Expand Your Lender Base

Even the best presentation fails if the customer can't get financed. Financing access is one of the most underused levers in F&I — a buyer who can't get approved through your dealership is a buyer who never sees your product menu.

Expanding your lender relationships directly increases the pool eligible for F&I product sales. Focus on:

- Adding subprime and secondary lenders to cover more credit profiles

- Reviewing your lender mix at least twice a year

- Tracking which lender gaps are costing you deal opportunities

Align Your Whole Dealership Around F&I Success

The Sales-to-F&I Handoff

What your salespeople say in the 60 seconds before the customer walks into the finance office either opens the door or closes it. Two examples:

- ❌ "You don't have to buy anything back there — it's just paperwork."

- ✅ "They'll show you options to protect your investment. You decide what makes sense for you."

The first kills the conversation before it starts. The second positions the F&I manager as a resource, not an obstacle. Build a scripted, non-negotiable handoff line and train every salesperson on it. No improvisation.

Service Department Reinforcement

When a service advisor says "good thing your service contract covers this" to a customer whose repair comes in at $1,800, that moment does more for future F&I sales than any training seminar. The service lane is one of your most underused F&I reinforcement tools.

The reverse is also true: customers who declined coverage and now face a large repair bill represent a follow-up opportunity. A well-timed outreach — not to say "told you so," but to offer coverage going forward — keeps the F&I department relevant beyond the original sale.

Protect F&I Profit After the Deal

All of that cross-department coordination only pays off if the gross you've booked actually reaches the bank. Three areas to watch:

- Chargeback trends: Monitor by product and by manager. A spike in cancellations on a specific product usually points to how it's being presented, not the product itself.

- Product explanations: Overpromising causes chargebacks. Plain-language, honest presentations prevent them.

- Paperwork and funding discipline: Errors in documentation create delays and occasionally kill deals. Tight review processes protect the gross you've already earned.

The F&I Profit Layer Most Dealers Never Capture

The Profit Leak That Exists Even in Well-Run Departments

Here's a simple question worth sitting with: if your third-party F&I product provider weren't making a profit from your business, why would they continue offering it?

Every time you sell a vehicle service contract or GAP product through a third-party provider, that provider collects the premium, pays the claims, and keeps what's left. That spread (the gap between premiums collected and claims paid) is underwriting profit. And in most dealerships, it flows entirely to the provider.

For a high-volume dealership, that's a substantial portion of the total economics of every F&I product sale that simply gets handed away.

How Dealer-Owned Reinsurance Fixes This

The admin obligor reinsurance model works like this: the dealer establishes their own reinsurance company (a separate legal entity) that assumes the underwriting risk on the VSCs and other F&I products they sell. Instead of underwriting profit flowing to the third-party provider, it flows into the dealer's own company.

The dealer still makes the same gross profit at the point of sale. The structure is backed by A-rated carriers for professional risk management. The difference is what happens to the money after the deal closes.

The Full Scope of Financial Benefits

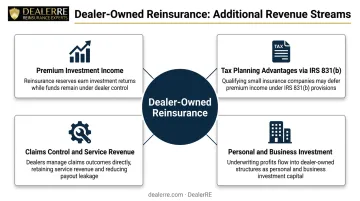

Dealer-owned reinsurance does more than capture underwriting profits. Four additional revenue streams come with the structure:

- Premium investment income: Reserve funds can be invested in conservative instruments, with all investment income belonging to the dealer's reinsurance company

- Tax planning advantages: Under IRS Section 831(b), qualifying small insurance companies are taxed only on investment income — not on premium income

- Claims control: Dealers control the claims process and can direct service work back to their own facility, keeping revenue in the dealership ecosystem

- Personal and business investment: Earned income can be deployed into real estate, reinvestment in the dealership, education funding, or other investments — a long-term wealth-building vehicle alongside day-to-day F&I income

Note: IRS regulations finalized in January 2025 updated micro-captive rules. Most dealer reinsurance programs qualify for the Consumer Coverage Exception if more than 95% of ceded risk involves unrelated customers. Verify your program's compliance with current IRS guidance.

Who This Works For

Dealer-owned reinsurance is available to franchise dealers, independent dealers, and BHPH dealers. The most common misconception is that reinsurance requires high volume. Smaller dealers have historically been under-marketed to, not disqualified.

For BHPH dealers specifically, the structure addresses a core business problem: customers stop paying when vehicles break down. Admin obligor reinsurance allows BHPH dealers to build a customer-funded pool to cover mechanical repairs, so the dealer draws from the reinsurance fund instead of paying out of pocket to preserve a payment stream.

The premium is financed over the contract term, so there's no cash flow hit upfront.

DealerRE: Specialist Partner for Dealer-Owned Reinsurance

DealerRE has helped over 400 auto dealers establish reinsurance companies since 1994. Their full-service model handles every layer of complexity that would otherwise stop dealers from pursuing this structure:

- Company setup and formation

- F&I training (online and in-person)

- Claims adjudication

- Compliance management

- Performance reporting and financial administration

- All legal forms, filings, tax returns, and renewals

For dealers ready to stop giving away underwriting profits, the next step is understanding what a program looks like for their specific volume and dealer type.

Frequently Asked Questions

What is a good F&I gross profit per vehicle retailed (PVR) for a dealership?

Public franchise groups averaged $2,505 PVR in Q1 2025, while the all-dealer average hit a record $1,944 in November 2024. Performance varies by vehicle type, deal mix, and process consistency. Use these as starting benchmarks, not ceilings.

What F&I products generate the highest profit for dealerships?

Vehicle service contracts drive the most revenue at roughly 54% of total F&I product income, with GAP second. Prepaid maintenance and ancillary products (tire/wheel, appearance, windshield) add incremental margin — the best mix depends on your vehicle inventory and customer profile.

How can I improve F&I penetration rates at my dealership?

Three levers move the needle most: 100% menu presentation with no customer exceptions, a needs-based discovery conversation before the menu, and weekly coaching tied to live performance data rather than periodic training events.

What is dealer-owned reinsurance and how does it differ from using a third-party F&I provider?

With a third-party provider, the underwriting profit — the spread between premiums collected and claims paid — stays with the provider. Dealer-owned reinsurance lets you establish your own company that captures those profits directly, while an A-rated carrier backs the contracts.

How do chargebacks affect F&I profitability and how can I reduce them?

Chargebacks erode your booked PVR — one example showed 18% deal cancellation rates gutting effective profitability. Most trace back to overpromising or poor product fit. Monitor trends weekly by product and manager, and keep your presentations honest and plain-language.

Is dealer-owned reinsurance available for independent and BHPH dealers?

Yes. Reinsurance programs are available to franchise, independent, and BHPH dealers. For BHPH operations, programs can be structured around mechanical breakdown and insurance protection funded through the customer payment base, with premiums financed over the contract term.