F&I gross profit per vehicle is approaching all-time highs in 2025, according to Haig Partners data — while the front end shrinks. That shift makes the F&I office the most reliable profit center in the dealership, and the dealers who understand what's driving PVR growth right now are pulling ahead.

This article breaks down the five trends shaping F&I profitability in 2025, the macro forces behind them, and what high-performing dealers are doing differently.

TL;DR

- F&I gross profit per vehicle is near historic highs in 2025, averaging $2,534 at public dealer groups as of Q3

- Higher product penetration is the primary driver of PVR growth

- AI and digital tools are cutting friction and lifting customer satisfaction across the F&I process

- Dealer-owned reinsurance structures let dealers capture underwriting profits that previously left the dealership entirely

- Focused training, cross-departmental alignment, and lean product menus define top-performing F&I offices

The State of F&I Profit Per Vehicle in 2025

F&I PVR has climbed steadily throughout 2025. Haig Partners data shows public dealer groups averaged:

| Quarter | Avg F&I PVR | YoY Change |

|---|---|---|

| Q1 2025 | $2,505 | +2.8% |

| Q2 2025 | $2,515 | +3.2% |

| Q3 2025 | $2,534 | +5.2% |

That Q3 figure puts F&I PVR close to all-time records. StoneEagle's broader dealer sample tells a similar story — average F&I income hit $1,924 per vehicle in Q2 2025, up 7.6% year-over-year, with March 2025 setting the highest average total F&I income per dealer since the post-COVID boom.

The Contrast With Front-End Margins

The front end is moving in the opposite direction. New vehicle front-end gross profit declined for nine consecutive quarters through Q2 2024, dropping 26.9% year-over-year. StoneEagle reported front-end gross at just $695 per vehicle in June 2025 — down 40% from 2024 highs.

Used vehicle margins have followed a similar path, falling 36.6% from pandemic-era peaks to roughly pre-pandemic norms.

That compression isn't easing. Tariffs on vehicles imported from Canada and Mexico are pushing transaction prices higher while suppressing volume. Affordability challenges are keeping buyers on the sidelines. And rising vehicle repair costs are making F&I products easier for managers to present and close than at any point since the post-COVID normalization period.

Why Product Penetration Is the Metric to Watch

PVR tells you what the F&I office earned per deal. Product penetration — the share of deals that include at least one F&I product, and how many — tells you why. With front-end margins compressed on both new and used vehicles, the F&I office has become the primary profit center for most dealers. Penetration is the engine driving PVR growth in 2025, and each trend covered below circles back to it.

Trend 1: Higher Product Penetration Is Driving PVR to Record Levels

The PVR gains aren't coming from price increases alone. Dealers are selling more products per transaction.

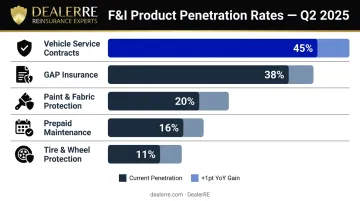

StoneEagle Q2 2025 data shows products per deal at 1.57, up from 1.52 a year earlier. Current penetration rates by product:

| Product | Q2 2025 Penetration | YoY Change |

|---|---|---|

| Vehicle Service Contracts | 45% | +1 pt |

| GAP Insurance | 38% | +1 pt |

| Paint & Fabric Protection | 20% | +1 pt |

| Prepaid Maintenance | 16% | Flat |

| Tire & Wheel Protection | 11% | +1 pt |

Those gains look modest in isolation. But across thousands of transactions, each incremental percentage point in penetration adds real dollars to annual F&I income — and rising repair costs explain why buyers are increasingly receptive.

Why Consumers Are More Receptive

Rising repair costs have made protection products an easy sell. The BLS CPI for motor vehicle maintenance and repair rose 7.7% year-over-year as of September 2025 — more than double the 3.0% all-items CPI rate. Motor vehicle repair alone climbed 11.5% over the same period.

Buyers who just spent $35,000 on a vehicle and understand that a transmission repair now costs $4,000+ are much easier to have a service contract conversation with.

The Sweet Spot: One to Two Products Per Deal

CDK Global research shows that 49% of car shoppers purchase one to two F&I products per deal. Take rates drop sharply beyond that: only 10% opted for three to four items, and just 4% bought five or more.

Presenting a full catalog actually hurts penetration. High-performing F&I offices narrow it down to the two or three products most relevant to each deal — based on vehicle type, customer profile, and loan structure. Focused presentations close more consistently than broad ones.

Trend 2: Digital F&I Tools and AI Are Reshaping the Finance Office

Digital tools have moved from a convenience into a core driver of F&I performance. Offices that have adopted structured digital workflows are seeing higher penetration rates, faster deal times, and stronger compliance posture — all at once.

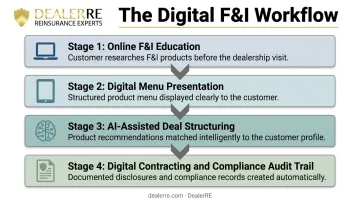

What "Digital F&I" Actually Means in Practice

The shift encompasses several distinct capabilities:

- Digital menu systems that guide customers through product presentations in a structured, documented format

- Online F&I education that introduces product value before the customer reaches the finance office

- AI-assisted deal structuring that matches product recommendations to customer and vehicle profiles

- Digital contracting that reduces time in the finance office and creates compliance audit trails

When customers encounter F&I product information during online research or through a digital menu before sitting down with the finance manager, they arrive better informed and less resistant. That reduced resistance translates directly into higher product acceptance rates once the finance conversation begins.

The Satisfaction Data

The Cox Automotive 2025 Car Buyer Journey Study found that overall buyer satisfaction reached record highs in 2025. 84% of shoppers who used AI-powered online tools reported high satisfaction. Buyers who completed more than half their purchase steps digitally saved time at the dealership and reported higher overall satisfaction across the board.

Those same tools that improve customer experience also serve the dealership's compliance needs — a connection worth understanding before the next audit.

The Compliance Dimension

Digital menu systems create consistent, documented product presentations — every customer sees the same menu, in the same compliant format, with the same disclosures. That consistency has real regulatory value.

The FTC's March 2026 warning to 97 dealership groups about deceptive pricing practices — with pending enforcement actions against specific groups — makes clear that documentation and transparency aren't just good customer service. They're risk management.

Trend 3: Dealer-Owned Reinsurance — Keeping the Profits That Used to Walk Out the Door

Dealer-owned reinsurance is the structural shift that most directly changes a dealer's long-term financial picture — redirecting underwriting profits and investment income that currently flow to third-party providers back to the dealership itself. Most smaller dealers assume it requires high volume. It doesn't.

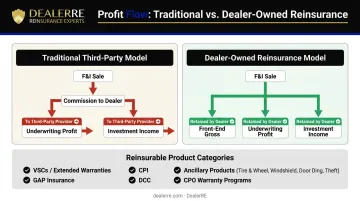

How the Traditional Model Leaks Profit

In a standard third-party arrangement, a dealer sells a service contract or GAP policy, earns a commission or markup, and that's the end of their participation. The underwriting profit — what's left after claims are paid — flows to the third-party provider. So does the investment income earned on the reserves while contracts are outstanding.

If your warranty company weren't making a profit from your F&I sales, why would they continue to do business with you?

What Dealer-Owned Reinsurance Captures Instead

When a dealer establishes an admin obligor reinsurance company, they retain:

- The same front-end F&I gross they were already earning

- The underwriting profit (the premium reserves not consumed by claims)

- Investment income on reserves, held in trust and invested conservatively in government bonds

Mercer Capital describes this structure as allowing dealers to retain underwriting profits and investment income otherwise ceded to third-party providers. The dealer's reinsurance company is backed by A-rated insurance carriers, so customer claims remain protected even if the dealer's reserves face stress.

Products That Can Be Reinsured

Dealers aren't limited to VSCs — the reinsurable product set covers most of what a well-run F&I office already sells:

- Vehicle Service Contracts and Extended Warranties

- GAP Insurance

- Collateral Protection Insurance (CPI) — especially relevant for BHPH

- Debt Cancellation Coverage (DCC)

- Ancillary products: Tire & Wheel, Windshield Repair, Door Ding, Theft Protection

- Certified Pre-Owned warranty programs

Tax Planning and Wealth Building

The broader the product mix in a dealer's reinsurance company, the more premium volume accumulates — and that volume creates real tax planning leverage. Reinsurance companies are taxed as property and casualty insurers under IRS rules, and entities with less than $2.2 million in annual net premiums may elect to be taxed only on investment income under IRC 831(b).

Earned income from the structure can be deployed in several directions:

- Reinvested into the dealership

- Applied to real estate acquisition

- Used for college funding, watercraft, or personal financial goals

DealerRE, founded in 1994 by Tim Byrd in Southeast Virginia, specializes in helping franchise dealers, independent dealers, and BHPH operators establish and manage admin obligor reinsurance companies. Their full-service model covers claims adjudication, compliance, financial reporting, tax filings, and performance analysis, so dealers capture the profit without taking on the administrative burden themselves. DealerRE has worked with over 400 dealers nationwide, with several clients earning National Quality Dealer of the Year recognition.

The most common misconception, according to DealerRE's team: that dealers need high volume to participate. Most larger dealers already own reinsurance companies. The opportunity has simply been undermarketed to smaller dealers who qualify.

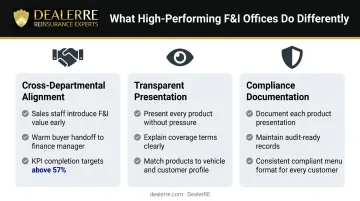

Trend 4: F&I Training and Cross-Departmental Collaboration Are Closing the Performance Gap

AutoNation averaged $2,775 F&I PVR in Q3 2025. Penske averaged $1,966. The gap between top and average performers isn't explained by luck — it's explained by process.

What High-Performing F&I Offices Do Differently

The finance office doesn't operate in isolation. When sales staff understand F&I products and introduce their value during the front-end conversation, the F&I manager inherits a warmer, more prepared buyer. That handoff is worth real money.

J.D. Power's 2024 Sales Satisfaction Index found that when nine or ten key performance indicators are met during the sales experience, satisfaction scores average 917 out of 1,000. When only seven or eight are met, scores drop 90 points. Currently, only 57% of buyers report that nine or ten KPIs were completed.

The gap between 57% and 100% KPI completion is largely a training and process problem, one that cross-departmental collaboration directly addresses.

Compliance as a Profitability Tool

FTC scrutiny on dealership F&I practices is intensifying. Compliance-focused training isn't just about avoiding fines — it builds the customer trust that makes product acceptance more likely.

Finance offices that consistently earn better take rates tend to share a few habits:

- Present every product transparently, without pressure tactics

- Document each presentation for both compliance and follow-up purposes

- Explain coverage terms clearly so buyers can make informed decisions

DealerRE provides F&I training as part of its full-service program, with both online and in-person options alongside F&I menu development. Dealers get tools to improve penetration rates while maintaining regulatory compliance.

Trend 5: Consumer Trust in the F&I Manager — and How Smart Dealers Use It

Here's a finding worth putting on the wall of every F&I office: 65% of car buyers say they trust the F&I manager more than any other dealership employee. Over 80% describe the F&I manager as honest, patient, and a good communicator, per CDK Global research.

That trust is an asset. Most dealers don't fully deploy it.

Positioning F&I as Financial Guidance, Not an Upsell

Dealers who understand this dynamic shift their framing. Rather than presenting products as add-ons at the end of a deal, they position the F&I office as an advocate for the customer's financial protection — addressing coverage that connects directly to costs the customer just experienced:

- Rising repair bills they saw on the service drive

- Total loss exposure on a vehicle they just financed

- Maintenance price increases they've already absorbed

That context makes coverage feel relevant rather than optional. When the conversation is framed that way, one or two well-chosen products — delivered by someone the customer already trusts — consistently outperforms a five-product catalog presentation.

The discipline matters: presenting too many options signals upsell, not guidance. That distinction erodes the exact trust that makes the F&I office effective in the first place. Dealers who protect that trust — and pair it with products they actually control through a reinsurance structure — capture both the acceptance rate and the underlying profit margin.

What's Driving These Trends — and What to Watch Next

Driving Forces Behind 2025 F&I Momentum

Three structural forces are converging:

- Front-end margin compression is pushing dealer focus toward back-end profit, making F&I investment a strategic priority rather than an afterthought

- Rising repair costs and parts inflation — with motor vehicle repair CPI up 11.5% year-over-year — are making protection products genuinely valuable to buyers, not just profitable for dealers

- Technology investment is reducing friction throughout the F&I process, enabling higher penetration by getting product information in front of customers earlier and more consistently

Tariffs add another layer. Edmunds found that 44% of shoppers say tariffs will definitely influence their next vehicle purchase, with S&P Global expecting 25% tariffs on Canadian and Mexican imports to persist through 2025. Higher transaction prices shrink the buyer pool — but the buyers who remain tend to be better qualified and more receptive to financial protection products.

Future Signals to Watch

Two developments deserve close attention as market conditions evolve:

EV-specific F&I products are gaining traction. JM&A Group's EV+ Protect suite covers vehicle, battery, and battery systems in a single warranty — unlike traditional products that split these coverages. Dealers reportedly earn 10% more on F&I product sales for EVs compared to ICE vehicles.

Dealers building EV F&I expertise now will be ahead of that curve when adoption accelerates.

Normalization risk is the other side of the equation. Continued affordability pressure and potential rate increases could reduce buyer willingness to add products. The dealers best insulated from that risk have diversified product portfolios, strong training programs, and reinsurance structures that generate profit independent of any single product cycle.

Frequently Asked Questions

What does F&I mean at a car dealership?

F&I stands for Finance and Insurance — the department that arranges vehicle financing and presents protection products like service contracts, GAP coverage, and prepaid maintenance. F&I is typically one of the highest-margin departments in a dealership.

What is a good F&I profit per vehicle in 2025?

Haig Partners' Q3 2025 data shows public dealer groups averaging $2,534 per vehicle retailed, which is near historic highs. That's a useful benchmark for franchise and independent dealers measuring their own performance.

What F&I products generate the most profit for dealerships?

Vehicle Service Contracts and GAP insurance rank as the highest-volume and highest-revenue products. Prepaid maintenance, tire and wheel protection, and appearance packages also add solid margin to per-vehicle totals.

How many F&I products should a dealer offer per deal?

Industry data points to one to two products as the sweet spot. Take rates drop sharply beyond that. The key is presenting the most relevant products for each specific vehicle and customer rather than offering the full catalog.

How does dealer-owned reinsurance increase F&I profitability?

Dealer-owned reinsurance captures both the front-end F&I gross and the underwriting profit (the reserve funds not consumed by claims), plus investment income on those reserves. In a standard third-party arrangement, only the initial markup stays with the dealer.

What is the biggest driver of F&I PVR growth in 2025?

Stronger product penetration (more products sold per transaction) is the primary driver cited by public dealer groups. Consumer demand for protection products has grown alongside rising repair costs and higher vehicle prices, making that penetration growth sustainable rather than artificially inflated.