Introduction

Most BHPH dealers know they're running a profitable business model. Fewer realize just how much income they're leaving on the table.

The BHPH structure is unusual in automotive retail: you're operating as both a dealership and a lender simultaneously. That dual role creates at least four distinct profit streams — front-end vehicle margin, interest income from in-house financing, F&I product sales, and reinsurance underwriting profit. Most operators lean heavily on the first two and treat the others as secondary.

That habit is costly. According to NABD/NIADA benchmark data, the average net loss per charge-off reached $6,646 — a number that puts a sharp edge on every profit decision, from how you price inventory to whether you sell a service contract on the deal. Operators who master all four revenue streams consistently outperform those who treat BHPH as a car sales business with payments attached.

This article covers the specific levers that separate high-performing BHPH operations from those that merely survive: inventory and pricing decisions, RFC structure optimization, F&I product integration, and customer retention as a direct financial tool.

TL;DR

- BHPH profit comes from vehicle sales, financing interest, F&I products, and reinsurance — front-end margin is only part of the picture

- Smart inventory sourcing and reconditioning spend protects both gross profit and portfolio performance

- A properly structured RFC defers income, reduces tax burden, and creates a receivables asset you can borrow against

- Dealer-owned reinsurance captures the underwriting profits that currently flow to third-party providers

- Every repossession avoided is a direct profit win — retention is a financial strategy, not just a service philosophy

The BHPH Profit Model: Four Revenue Streams Working Together

BHPH dealerships occupy a unique position: every sale creates two simultaneous profit events: the vehicle margin booked at closing, and the interest income earned over the life of the loan. Most operators track the first. Fewer model the second with any precision.

Front-End Gross and Financing Income

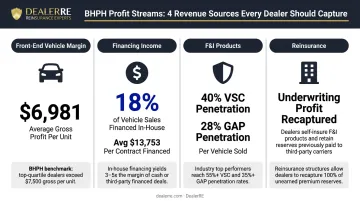

Per NABD/NIADA benchmark data, average gross profit per vehicle sold reached $6,981 in 2021, up from $6,029 in 2019. Industry-wide gross margin climbed from 31% to 38% over the same period, a meaningful recovery. Financing income represented 18% of vehicle sales in the 2019 composite, acting as a fully separate revenue layer on top of that vehicle gross.

The math on a typical note makes this concrete. With an average amount financed of $13,753 (2021 NIADA) and average original loan terms of roughly 43 months, BHPH interest rates (which vary by state usury law but commonly run 18–29.99% APR) generate total collections that can significantly exceed the vehicle's original sale price. The financing side isn't a footnote; for many operators, it's the business.

The RFC Layer

The Related Finance Company (RFC) structure addresses a tax problem created by the Tax Reform Act of 1986. That law eliminated installment reporting for dealers, forcing recognition of full profit at the point of sale — even on receivables not yet collected. The result: dealers owed taxes on cash they hadn't received yet, a problem known as phantom income.

The RFC solves this by having the dealership sell installment contracts to a separately owned finance entity at a discount, creating an offsetting loss at the dealership level. The RFC then collects payments over time and recognizes income as cash arrives. The outcome is deferred tax liability, smoother income recognition, and a receivables portfolio that can be used to raise capital. As SGC Accounting notes, that capital-raising ability should be the primary motivator, beyond tax savings alone.

F&I and Reinsurance: The Underutilized Layers

Industry-wide F&I penetration averages 40% for vehicle service contracts and 28% for GAP. Franchise dealer groups reported average F&I gross profit per vehicle of $2,515 in Q2 2025. BHPH operators have no comparable published benchmark, suggesting most aren't capturing this income at all.

The deeper issue is structural. Even dealers who sell F&I products at reasonable penetration rates typically hand the underwriting profit to a third-party provider. Common products where this margin leaks out include:

- Vehicle service contracts

- GAP coverage

- Collateral protection insurance (CPI)

- Ancillary products (tire and wheel, debt cancellation, theft protection)

A dealer-owned reinsurance program recaptures that margin — keeping underwriting profits inside the dealership rather than funding a third-party provider's bottom line.

Vehicle Acquisition and Pricing Strategy

In BHPH, every inventory decision carries a direct financial consequence that extends well beyond the front-end gross.

Why Vehicle Condition Is a Profit Variable

Industry analysis from Advantage GPS documents a "90-day breakdown cycle": mechanical problems typically begin 30–60 days before the first missed payment, with delinquency following within 30 days of a failure. The causal chain is direct — a subprime borrower who can't drive to work can't make a payment.

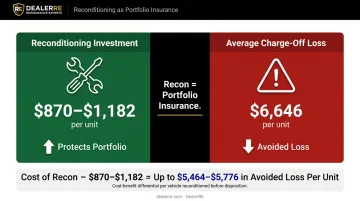

This makes reconditioning spend function as portfolio insurance, not just a cost of goods sold. NABD/NIADA benchmarks put average reconditioning cost at $870–$1,182 per unit. That investment compares favorably against the $6,646 average net loss per charge-off when a loan fails. Operators who minimize recon to protect front-end gross are increasing their charge-off exposure.

Sourcing and Pricing

High-performing BHPH operators tend to:

- Define a narrow set of target makes and models with reliable mechanical histories

- Focus on digital wholesale channels rather than physical auctions, where competition from retail buyers inflates acquisition costs

- Model deal profitability across the full term, not just at the point of sale

On pricing: setting a vehicle price too low to win the deal can destroy the profitability of the financing contract if the customer defaults early. The sale price must account for acquisition cost, reconditioning, expected default rate, and the intended note term. A deal that looks competitive at signing can become a net loss by month six.

Those sourcing disciplines matter more as acquisition costs rise. Average ACV (including recon) reached $7,814 in 2021, up roughly $1,400 from the prior year as wholesale prices climbed sharply. Tighter margins at the point of purchase leave less room to absorb a default — making every sourcing and pricing decision count.

Maximizing Your In-House Financing and RFC Structure

Down Payment, Term Length, and Loss Exposure

Down payment strategy directly affects both deal accessibility and risk protection. Average cash down payments ranged from $703 (2020) to $1,267 (2021) per NIADA/NCM data, reflecting competitive pressure and market volatility. The traditional BHPH approach — sizing the down payment to exceed the dealer's cost in the vehicle — protected against repo losses. As competition has tightened, that cushion has eroded.

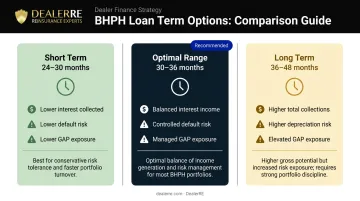

Term length is a related lever:

- Shorter terms (24–30 months) reduce total interest collected but lower default risk and GAP exposure

- Longer terms (36–48 months) increase total collections but raise the probability that the vehicle depreciates faster than the loan is paid down

- Most experienced operators target 30–36 months as a balance point that preserves enough interest income without excessive risk

RFC Mechanics in Practice

The RFC discount reflects the portfolio's expected loss rate. With industry average default rates at 37.5% (2019) and annualized repo rates at 28.1%, the discount applied when the dealership sells notes to the RFC must be commercially reasonable. The IRS has published specific guidance on this in its New Vehicle Dealership Audit Technique Guide.

For scaling operators, the RFC structure smooths income during growth phases and avoids large annual tax bills driven by rapid unit volume increases. The receivables portfolio also becomes a borrowable asset: a capital base that can fund future inventory acquisition.

Cash Flow and Compensation Alignment

One structural challenge unique to BHPH is that dealers use floorplan credit to acquire inventory and must pay off that line when the vehicle sells, but don't receive full proceeds at the point of sale. RFC funding timing and down payment size both interact with those payoff requirements.

Units that sit past 60 days generate curtailment obligations that erode cash flow. Turn discipline matters.

Compensation structure reinforces or undermines all of the above. Paying managers on collected payments rather than units sold aligns incentives with deal quality, down payment collection, and F&I product attachment — and discourages structuring weak deals just to book a unit.

Unlocking F&I and Reinsurance Profits

Why Back-End Profit Matters More in BHPH

At traditional dealerships, F&I products are primarily a revenue opportunity. In BHPH, they're also a risk management tool. Every product sold that protects the vehicle or the loan reduces the dealer's own exposure. A VSC that funds a transmission repair keeps the customer on the road. GAP coverage prevents a total loss from creating a deficiency balance the dealer must absorb.

The Core BHPH F&I Product Stack

- Vehicle Service Contracts (VSCs): Cover mechanical breakdown. In BHPH, they protect the loan — a running vehicle is a paying customer.

- GAP / Debt Cancellation Coverage (DCC): GAP covers the difference between insurance settlement and outstanding loan balance after a total loss. DCC is a reinsured waiver alternative that can be significantly less expensive for the customer than full coverage insurance — which also helps free up cash for car payments.

- Vendor Single Interest (VSI) / Collateral Protection Insurance (CPI): VSI protects the lender when a vehicle is damaged and the borrower lacks insurance. CPI is force-placed when the customer fails to maintain required coverage. Both can be reinsured so the dealer captures the underwriting profit rather than paying a third-party provider.

- Ancillary products: Tire and wheel, key replacement, and similar low-cost add-ons generate incremental revenue per deal with minimal claims exposure.

The Reinsurance Opportunity

Standard third-party F&I arrangements work against the dealer: you sell the contract, earn a markup, and the underwriting profit — the spread between premiums collected and claims paid — flows to the product company. For a BHPH dealer selling VSCs and GAP on every deal, that's a substantial annual profit transfer.

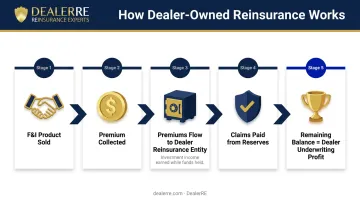

Dealer-owned admin obligor reinsurance recaptures that margin. The dealer establishes their own reinsurance entity (backed by A-rated insurers), premiums flow into that entity, claims are paid from reserves, and the remaining balance is the dealer's underwriting profit. Investment income on reserve funds adds another return layer while those funds are held.

DealerRE has been helping BHPH dealers build exactly this structure since 1994. Their admin obligor programs address a BHPH-specific cash flow concern: rather than requiring dealers to pay the full VSC cost upfront, premiums are financed over the contract term and billed monthly as customer payments come in. The contract remains fully reinsured, so the dealer captures all underwriting profit at term end — without straining their lending pool.

The structure also creates tax planning flexibility. Property and casualty insurers with less than $2.2 million in annual net premiums may elect to be taxed only on investment income under IRC 831(b). Once reserve thresholds are met, accumulated funds can be deployed toward:

- Real estate or dealership reinvestment

- Education funding

- Watercraft or other capital assets

- Any purpose the dealer directs

DealerRE manages the full administrative side of the program — legal forms, filings, tax returns, compliance, renewals, and staff training. Their administrator partner handles claims adjudication directly, giving dealers visibility into the claims process and control over how customer repairs are managed.

Customer Retention as a Profit Strategy

A repossession is not a neutral outcome. It is a direct financial loss.

The Real Cost of a Charge-Off

The average repo fee alone runs $411–$451. Factor in reconditioning at $1,244 per unit, resale losses, and foregone future collections, and total exposure per repossessed unit can reach $6,646 or more.

Every proactive outreach call, repair assist, or modest payment extension should be measured against that number — not against its direct cost.

Two Customers, Very Different Outcomes

Consider the contrast:

Customer A completes a 36-month loan: full interest income collected, VSC covers any mechanical work (possibly from the dealer's own reinsurance reserves), positive payment history, likely repeat buyer.

Customer B defaults at month 6: partial payment stream, repo fee, reconditioning cost, a used unit that must be re-priced and resold, and a lost receivable.

The difference between these two outcomes comes down to what happened around month 2 or 3 — whether someone called when the payment was three days late, or whether a minor mechanical issue got addressed before it became a breakdown.

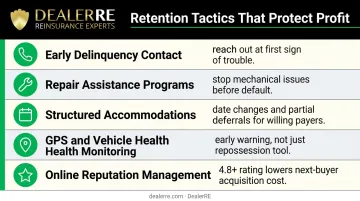

Retention Tactics That Work

High-performing BHPH operators use:

- Contact delinquent accounts at first sign of trouble — before the situation moves past recovery

- Offer repair assistance to stop mechanical breakdowns from triggering the 90-day default cycle

- Extend structured accommodations (date changes, partial deferrals) for customers who show payment intent

- Use GPS and vehicle health monitoring as early warning tools, not just repossession aids

- Actively manage online reputation — BHPH dealers who do this consistently reach 4.8+ Google ratings, which directly lowers acquisition cost for the next buyer

Frequently Asked Questions

What is the $3,000 rule for cars?

The "$3,000 rule" refers to an informal guideline around structuring used vehicle deals so the purchase price results in affordable monthly payments for subprime buyers. In BHPH, this concept influences how dealers price vehicles relative to down payment and term — pricing too high relative to buyer capacity increases early default risk regardless of how attractive the monthly payment looks.

What is the biggest mistake first-time car buyers make?

Most first-time buyers focus on the monthly payment rather than the total loan cost, leaving them exposed to long terms with heavy interest accumulation. BHPH dealers who walk buyers through total repayment — not just the weekly or monthly amount — tend to see stronger payment performance and fewer early defaults.

How profitable is a buy here pay here dealership?

BHPH operations running all four profit streams — vehicle margin, financing income, F&I products, and reinsurance — consistently outperform those relying on vehicle sales alone. NABD/NIADA benchmarks show operating income at 17% of vehicle sales (2021) with average gross profit per unit of $5,035–$6,981 depending on the composite. These figures represent best-performing operators — the spread between top and average performers is substantial.

What is a Related Finance Company (RFC) in BHPH?

An RFC is a separately owned finance entity that purchases installment contracts from the dealership at a discount. This lets the dealer offset gross profit with a discount loss — deferring tax liability — while the RFC recognizes income as payments are collected and can be borrowed against as a capital source.

What is dealer-owned reinsurance and how does it benefit BHPH operators?

Dealer-owned reinsurance allows BHPH operators to capture the underwriting profit from F&I products — VSCs, GAP, DCC, CPI — that would otherwise flow to third-party providers. Premiums are held in the dealer's reinsurance entity, which pays claims from reserves; the remaining balance is the dealer's profit, along with tax planning flexibility and direct control over claims adjudication.

How do BHPH dealers reduce repossession rates?

Deal structure is the foundation — adequate down payments and manageable terms reduce default risk before the loan is signed. Proactive outreach on late payments, repair assistance programs, and vehicle health monitoring technology all work together to prevent the mechanical breakdowns and missed payments that drive repossession cycles.