BHPH loan balances have grown 214% since 2018, reaching roughly $32 billion in outstanding balances as of late 2025 — hardly a fringe operation. Yet persistent myths continue to distort how dealers, customers, and regulators view the space.

This article breaks down what BHPH dealerships actually are, debunks the six most common myths dealers and customers encounter, and explains how ancillary products like service contracts and GAP fit into a well-run BHPH operation.

TL;DR

- BHPH dealerships act as both seller and lender, serving buyers who can't qualify through conventional financing channels

- Higher interest rates reflect the real default risk dealers absorb — not predatory intent

- Federal and state regulations govern BHPH operations more than most people realize

- Many reputable dealers now report payments to credit bureaus, offering customers a real credit-building path

- Service contracts and GAP protect customers — and stabilize the dealer's loan portfolio at the same time

What Is a Buy Here Pay Here Dealership?

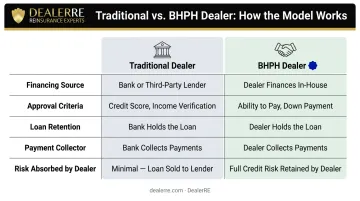

The BHPH model works like this: the dealership sells the vehicle and finances it in-house, keeping the loan on its own books rather than routing it through a bank or credit union. The buyer makes payments directly to the dealership.

Approximately 78% of BHPH lending volume goes to subprime borrowers, compared to only 27% for traditional auto lenders. Deep subprime borrowers — those with credit scores below 580 — accounted for more than half of all BHPH loans in 2025. These are buyers who have been declined by conventional lenders and have no other realistic path to financing.

How BHPH Differs from Traditional Dealers

| Feature | Traditional Dealer | BHPH Dealer |

|---|---|---|

| Financing source | Banks, credit unions | In-house |

| Approval criteria | Credit score-driven | Income and ability to pay |

| Loan stays with dealer | No | Yes |

| Who collects payments | Lender | Dealership |

| Risk absorbed by dealer | Minimal | 100% |

Two industry sources put it plainly. The CFPB defines BHPH dealers as those who "typically serve consumers with limited or damaged credit histories." NIADA goes further, describing BHPH customers as those "who would otherwise lack access to vehicle financing." That population runs into the millions — and the BHPH dealer is often the only option standing between them and transportation.

6 Common Myths About BHPH Dealerships — Debunked

Many of the myths circulating online stem from outdated practices, isolated bad actors, or generalizations applied unfairly to the entire industry. The reality is more nuanced — and for dealers and borrowers alike, the details matter.

Myth 1: BHPH Dealers Only Sell Low-Quality, Unreliable Cars

Fact: Selling unreliable vehicles is self-defeating for a BHPH dealer.

Unlike a franchise dealer who transfers the loan to a bank and moves on, the BHPH dealer carries every loan. If a customer's car breaks down, they stop paying. That direct financial consequence creates a strong incentive to sell vehicles that actually run.

NABD put it plainly: "If they cannot drive it, they aren't paying for it." Reputable dealers conduct multi-point inspections and recondition inventory carefully — not out of altruism, but because vehicle reliability directly determines portfolio performance.

Myth 2: Interest Rates at BHPH Lots Are Always Predatory

Fact: Higher rates reflect risk absorption, not margin extraction.

According to the Federal Reserve, BHPH dealers charge a weighted average of 25.39% APR for subprime borrowers, compared to 14.60% from traditional subprime lenders. The gap sounds alarming until you consider the context:

- BHPH dealers hold 100% of default risk — no secondary market, no bank backstop

- 5% of BHPH balances were in active repossession in late 2025

- Experian reports deep subprime used car APRs from all lenders at 21.81% — narrowing the gap considerably

The rate premium exists because BHPH dealers are absorbing losses that would otherwise fall on a bank. The relevant comparison isn't prime auto financing — it's what deep subprime borrowers pay everywhere else.

Myth 3: Customers Never Get Warranties or Vehicle Protection

Fact: The industry has shifted significantly on this.

The FTC's Used Car Rule requires every dealer to disclose whether a vehicle is sold with a warranty or "as is" via a Buyers Guide on the vehicle. Beyond that legal baseline, many reputable BHPH dealers today offer 30–90 day warranties or optional service contracts.

The logic is straightforward: when the car stops running, the customer stops paying — so protecting the vehicle protects the receivable. DealerRE works with BHPH dealers to build customer-funded service contract pools through dealer-owned reinsurance, so repairs don't come out of the dealer's pocket and the customer stays on the road.

Myth 4: BHPH Dealers Repossess Cars to Resell Them Repeatedly

Fact: Churning is expensive and reputation-destroying — not a viable model.

Repossession involves agent fees, storage costs, reconditioning, legal compliance with public vs. private sale requirements, and real administrative burden. Vehicles returned from customers frequently arrive with deferred maintenance and neglect. None of that is profitable.

In January 2025, the CFPB secured a $42 million judgment against a Georgia-based BHPH operator for illegal repossessions, misuse of vehicle disabling devices, and GAP refund failures. That enforcement action targeted a specific bad actor — not a systemic indictment of the broader model.

Most BHPH dealers prefer working with a struggling customer toward resolution rather than accelerating repossession. Keeping a customer in their vehicle and making payments is almost always more valuable than recovering a depreciated asset.

Myth 5: BHPH Dealerships Are Completely Unregulated

Fact: BHPH dealers operate under a substantial compliance burden.

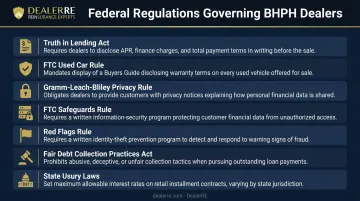

Federal regulations that apply directly to BHPH operations include:

- Truth in Lending Act (Regulation Z) — requires full disclosure of APR, finance charges, and payment schedules

- FTC Used Car Rule — mandates Buyers Guide disclosure on every vehicle

- Gramm-Leach-Bliley Privacy Rule — applies to all dealers who extend credit

- FTC Safeguards Rule — requires a written information security program

- Red Flags Rule — mandates identity theft prevention programs

- Fair Debt Collection Practices Act — governs collection activity

- State usury laws — set maximum interest rates and late fee limits by state

The CFPB has exercised active enforcement authority over BHPH dealers as creditors. NIADA, which represents over 13,000 members nationally, actively supports compliance standards and education across the industry.

Myth 6: BHPH Dealers Never Report Payments to Credit Bureaus

Fact: Credit reporting among BHPH dealers is growing — and becoming more standard.

In 2015, Equifax expanded its partnership with NIADA specifically to allow BHPH dealers to report consumer auto loan payment data without meeting traditional account-volume thresholds — a barrier that had previously locked smaller operators out of the reporting system entirely.

An increasing number of BHPH dealers now report on-time payments to credit bureaus. For a subprime borrower with limited options, consistent payment history on a BHPH loan can produce measurable credit score improvement. Buyers should ask about reporting practices before committing to any dealer.

How Reputable BHPH Dealers Actually Operate

Because the dealer carries every loan, the underwriting decision isn't handed off to an algorithm. Income verification, employment history, and residence stability become the primary approval factors — making the process more relational and less score-driven than conventional bank underwriting.

The Dealer-as-Lender Advantage

Having skin in the game on every deal creates natural incentives that work in the customer's favor:

- Responsible approvals — dealers who approve buyers who can't actually pay hurt themselves directly

- Fair vehicle pricing — overpriced inventory on an unaffordable loan ends in repossession, which costs the dealer money

- Proactive communication — reputable dealers reach out when a customer is struggling rather than waiting for default

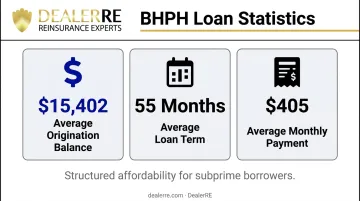

Average BHPH loan terms reflect this conservatism: $15,402 average origination balance, 55-month average term, $405 average monthly payment. For buyers working within a tight budget, those figures represent real, structured affordability — not a debt trap.

Industry Standards and Association Membership

NIADA acquired NABD's assets and operations in December 2017, creating a combined organization that represents over 13,000 members nationwide. NABD had published annual industry benchmarks for 20 consecutive years, giving dealers data-driven guidance on underwriting, collections, and loss management. That benchmark infrastructure transferred to NIADA with the acquisition.

Membership in NIADA signals a baseline commitment to compliance and professional standards. For BHPH dealers, it means access to:

- Underwriting and collections benchmarks built from real industry data

- Loss management guidance developed across hundreds of dealer operations

- Peer recognition programs that distinguish compliance-focused operators

DealerRE has been a member and sponsor of NIADA since its founding. Several DealerRE clients have been recognized as National Quality Dealer of the Year and have served as NIADA Board Members — a direct indicator of how seriously compliance-focused operators take their standing in the industry.

What Ancillary Products Mean for a BHPH Dealership

Ancillary products are financial protection products sold at the point of purchase: vehicle service contracts (VSCs), GAP coverage, collateral protection insurance (CPI), debt cancellation coverage (DCC), and vendor single interest (VSI) coverage. In a BHPH context, they serve a dual purpose — protecting the customer from financial exposure while protecting the dealer's loan portfolio.

Why These Products Matter More in BHPH Than Anywhere Else

A franchise dealer who sells the loan to a bank doesn't care what happens to the vehicle in month 18. A BHPH dealer absolutely does — because that monthly payment is still theirs to collect.

- Service contracts keep customers driving when mechanical breakdowns would otherwise trigger missed payments and repossession

- GAP coverage protects the dealer's receivable when an insurance settlement falls short of the remaining loan balance after a total loss

- CPI/DCC addresses the common BHPH reality that subprime customers often let their insurance lapse

- VSI coverage fills the gap when a customer's lapsed policy leaves the collateral — and the dealer's asset — exposed with no claim path

Many BHPH dealers already absorb these costs informally — forgiving balances after total losses, paying out-of-pocket to fix customers' cars. As DealerRE puts it: dealers are "providing GAP for the customer, you are just doing it for free."

The question isn't whether these costs exist. It's whether the dealer captures the income to offset them.

Retaining Underwriting Profits Through Dealer-Owned Reinsurance

When a dealer sells a service contract through a third-party provider, they earn a commission. The provider keeps everything left after claims — the underwriting profit. Over the life of a dealership, that retained profit can exceed the value of the dealership's annual F&I income.

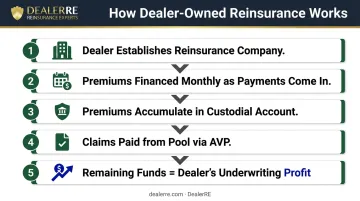

DealerRE's admin obligor reinsurance structure allows BHPH dealers to own that profit instead. Here's how it works in practice:

- Dealer establishes their own reinsurance company, backed by A-rated insurers through DealerRE's admin obligor structure

- Premiums are financed over the contract term — for BHPH operations specifically, dealers are billed monthly as customers make payments, preserving cash flow and lending capacity

- Premiums accumulate in a custodial account at a U.S. Trust Company, invested conservatively in government bonds

- Claims are paid from that pool, adjudicated through Assured Vehicle Protection (AVP)

- Remaining funds at contract end are the dealer's underwriting profit — money that previously went to a third-party provider

DealerRE has helped over 400 auto dealers establish these programs since Tim Byrd founded the company in 1994. The cash flow structure is particularly relevant for BHPH operators: unlike third-party arrangements that may require full premium payment upfront, the monthly billing model aligns with how BHPH dealers actually receive income.

The result is a dealership that protects its receivables, serves customers better, and builds a secondary income stream from products it was likely already offering — just without the profit staying in house.

Frequently Asked Questions

What is an ancillary product on a Buy Here Pay Here car loan?

Ancillary products are add-on protection items sold alongside a BHPH vehicle purchase — typically including service contracts, GAP coverage, CPI, and DCC. They protect the customer from unexpected financial exposure while also protecting the dealer's loan portfolio against breakdown-related missed payments and total-loss shortfalls.

Are BHPH dealerships regulated by law?

Yes. BHPH dealers are subject to the Truth in Lending Act, FTC Used Car Rule, Gramm-Leach-Bliley Privacy and Safeguards Rules, Red Flags Rule, state usury laws, and CFPB enforcement authority. The "completely unregulated" claim doesn't hold up to scrutiny.

Do Buy Here Pay Here dealers report payments to credit bureaus?

A growing number do. Equifax expanded its NIADA partnership in 2015 specifically to make reporting accessible to smaller BHPH operators. Dealers who participate gain a tangible differentiator — offering customers a path to credit rebuilding that competitors may not provide.

What credit score do you need to buy from a BHPH dealership?

BHPH dealerships typically don't set minimum credit score thresholds. Approvals are based primarily on verifiable income, employment stability, and demonstrated ability to make regular payments — not a three-digit number.

Is Buy Here Pay Here bad for customers?

BHPH is a viable — and often necessary — option for credit-challenged buyers. Outcomes depend heavily on the specific dealership. Reputable operators offer transparent terms, inspected vehicles, protection products, and responsive service throughout the loan term.

How do Buy Here Pay Here dealers make money?

BHPH dealers earn through vehicle sale markup, interest collected on in-house loans, and ancillary product income. Dealers who establish their own reinsurance structure — like those DealerRE works with — also retain the underwriting profits from protection products rather than sending that income to third-party providers.