Dealers hear this question constantly, and buyers wrestle with it at nearly every new-car purchase. The honest answer is: it depends — but not just on price. The coverage terms, who's backing the product, and how the dealer structured the program in the first place matter just as much as the sticker.

This post breaks down both sides of the equation. For buyers, it's a practical guide to when dealer GAP is genuinely worth the premium. For dealers, it's a look at why the structure behind the product determines whether you can price it competitively and still offer superior coverage.

DealerRE has been working in dealer F&I reinsurance since 1994, so this comparison goes deeper than surface-level pricing.

TL;DR

- Dealer GAP typically runs $500–$700 as a lump sum rolled into your loan; insurer GAP endorsements average $20–$150 per year — though coverage terms differ significantly between the two

- Key dealer GAP advantages: deductible coverage up to $1,000, negative equity from trade-ins covered, higher LTV payout limits, and no coverage loss when switching auto insurers

- Dealer GAP makes the most financial sense with low down payments, loan terms of 60+ months, rolled-in negative equity, or fast-depreciating vehicles

- For dealers, whether GAP is structured through a reinsurance company or a straight third-party markup determines who keeps the underwriting profit

What Is GAP Insurance from a Dealer?

GAP (Guaranteed Asset Protection) covers the difference between what you owe on your auto loan and what your standard insurer pays out after a total loss or theft. That payout is based on the vehicle's actual cash value (ACV) — and new vehicles can lose an average of 23.5% of their value in the first year, according to Edmunds. That gap between ACV and your loan balance is exactly what this coverage is designed to close.

How It's Offered at the Dealership

Dealer GAP is presented in the F&I office at the time of sale, either as a standalone flat fee or rolled into your loan financing. Adding a GAP endorsement through your existing auto insurer is a completely separate option — one most buyers never hear about at the dealership.

What dealer GAP does NOT cover:

- Vehicle repairs or mechanical issues

- Personal injuries from an accident

- The cost of purchasing a replacement vehicle

- Any loss outside of total loss or theft scenarios

GAP is optional in most cases. A lender may require it as part of a financing agreement, but a dealer cannot make it a condition of the sale itself — that distinction matters when you're evaluating whether the price you're being quoted is fair.

Dealer GAP vs. Insurer GAP: A Side-by-Side Breakdown

Cost Structure

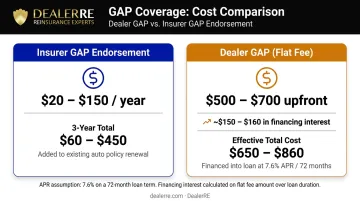

According to NerdWallet, dealer GAP runs $500–$700 as a one-time flat fee. Insurer GAP endorsements typically cost $50–$150 per year, or as little as $20 annually per Bankrate.

That gap widens when you factor in financing. At the current average APR of 7.6% on a 72-month new-car loan, rolling a $600 GAP fee into your loan adds roughly $150–$160 in interest — bringing the effective cost closer to $760.

| Source | Channel | Cost | 3-Year Effective Cost |

|---|---|---|---|

| NerdWallet (2026) | Insurer endorsement | $50–$150/yr | $150–$450 |

| Bankrate (2025) | Insurer endorsement | ~$20/yr | ~$60 |

| NerdWallet (2026) | Dealer (flat fee) | $500–$700 | $650–$860 with interest |

Cost is only one variable. The deductible treatment, negative equity coverage, and portability terms can matter just as much at claim time.

The Deductible Difference

Insurer-sourced GAP pays out after your deductible is applied. Progressive states explicitly that GAP coverage pays the difference between your loan balance and ACV, "minus your deductible." State Farm and Liberty Mutual confirm the same.

In a typical scenario: you owe $18,000, ACV is $15,000, the gap is $3,000, and your deductible is $500.

| Product | Primary Insurance Pays | GAP Pays | You Pay |

|---|---|---|---|

| Insurer GAP | $14,500 | $3,000 | $500 |

| Dealer GAP (deductible coverage) | $14,500 | $3,500 | $0 |

Well-structured dealer GAP programs — including DealerRE's — cover the underlying insurance deductible up to $1,000. That's a real, measurable difference at claim time.

Negative Equity Coverage

This matters for anyone who rolled a balance from a trade-in into their new loan.

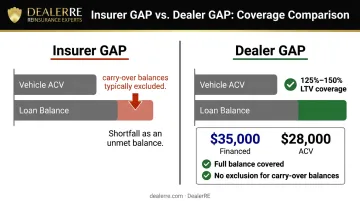

Insurer GAP products typically exclude carry-over balances from previous loans. NerdWallet confirms that GAP insurance "typically does not cover carry-over balances from previous loans or leases." State Farm's documentation says the same.

Dealer GAP programs — when properly written — can cover the full financed amount, including rolled-in negative equity. DealerRE's GAP program offers 125% or 150% LTV coverage, meaning it can protect loan balances up to 150% of the vehicle's ACV at total loss. For a buyer who financed $35,000 on a car worth $28,000 at purchase, that distinction could mean thousands of dollars.

Coverage Limits

Progressive caps its loan/lease payoff product at 25% of the vehicle's ACV. On a $20,000 ACV vehicle, that's a $5,000 maximum payout — and if you owe $28,000, you're still $3,000 short.

Allstate uses a dollar-amount cap (up to $50,000) rather than a percentage, per Bankrate. Dealer GAP products generally don't carry ACV percentage caps, though individual administrator contracts may set maximum dollar limits.

Portability

Those coverage constraints connect to a broader flexibility question: what happens when you switch insurers? Insurer GAP is an endorsement tied to your policy — switch carriers, and coverage terminates. You'd have to re-add GAP with the new insurer, if they offer it.

Dealer GAP is a standalone contract. It stays in force regardless of which auto insurer you use, giving you full freedom to rate-shop your primary policy without affecting GAP coverage.

When Dealer GAP Insurance Is Actually Worth the Price

On day one of your loan, if your financed amount exceeds the vehicle's actual cash value, you're already underwater. The real question is how far underwater — and whether the cost of dealer GAP coverage is proportionate to that risk.

Dealer GAP makes the most sense when:

- Your down payment was less than 10–15% of the purchase price

- Your loan term is 60 months or longer (nearly 30% of new loans now run 73–84 months, per Experian Q4 2025)

- You rolled negative equity from a trade-in into the new loan

- You're financing a vehicle with steep depreciation — EVs and luxury sedans are the highest-risk category, with some models losing more than 50% of value in three to four years

- Your average daily mileage is high, accelerating depreciation

When dealer GAP is harder to justify:

- You put 20%+ down

- Your loan term is 36–48 months and you're close to ACV from the start

- You're financing a vehicle known for retaining value well

If you've already purchased dealer GAP and your situation has improved — your balance is now close to or below ACV — cancellation is an option worth exercising. GAP can be canceled once your loan balance falls below the vehicle's value. Many contracts include a full-refund window within the first 30 days and prorated refunds after that. The CFPB is explicit that buyers have the right to cancel optional add-on products at any time.

Why Dealer GAP Has a Reputation Problem — and Whether It's Deserved

The criticism is legitimate — but it's aimed at a specific business model, not dealer GAP as a category.

The Traditional Markup Problem

In the standard F&I setup, the dealer buys GAP wholesale from a third-party provider and resells it at retail. The spread is dealership revenue. The underwriting profit — what's left after claims — goes entirely to the third-party provider.

This creates a problematic incentive structure: the dealer has every reason to maximize the retail price and no financial stake in whether the product actually performs well for the customer. The result is $700 price tags for products available elsewhere for less, and no particular reason for the dealer to offer better terms.

What Makes Dealer GAP Worth the Premium

Dealer GAP earns its price when the coverage terms genuinely differ. Specifically:

- Deductible coverage — up to $1,000 reimbursed at claim time

- Negative equity coverage — full financed balance, not just the current vehicle's value

- Higher LTV limits — 125% or 150% of ACV rather than a 25% cap

- Carrier portability — stays in force when the customer switches auto insurers

- No risk of cancellation for claims filed

These advantages only materialize if the dealer's GAP product is actually written with these terms. Not all dealer GAP is equal — and customers should ask specifically about each of these points before signing.

That verification matters for compliance reasons, too. The FTC's CARS Rule (finalized January 2024) requires dealers to disclose that add-ons are not required for the vehicle purchase and prohibits charging for them without express informed consent. Dealers who communicate GAP's coverage advantages clearly — rather than burying the terms in fine print — satisfy the regulation and build the kind of trust that holds up when a customer actually files a claim.

How a Dealer-Owned Reinsurance Program Changes the GAP Equation

This is where the conversation shifts for dealers.

The Fundamental Economic Shift

In the traditional model, a dealer earns a commission on the GAP sale. The third-party provider keeps the underwriting profit — the difference between all premiums collected and all claims paid. As DealerRE puts it: if your third-party GAP provider weren't making a profit off you, why would they continue doing business with you?

When a dealer operates their own reinsurance program, that underwriting profit stays with the dealer. The customer pays the same retail price. The dealer still captures the front-end gross margin. But now the long-term premium economics (what's left after claims are paid) flow into the dealer's own reinsurance entity rather than into a third-party company's bottom line.

What It Enables on the Coverage Side

Owning the reinsurance structure gives dealers direct control over product terms. DealerRE's GAP program, for example, supports:

- LTV coverage at 150% or 125%, protecting loan balances well above typical insurer caps

- Underlying insurance deductible coverage up to $1,000

- Backing by an A-rated carrier through the admin obligor structure — meaning if the reinsurance entity can't meet obligations, the A-rated carrier covers the claim

That combination of broad coverage terms and profit retention is what makes dealer-owned GAP competitive at the F&I desk. The dealer can price competitively, offer terms that outperform insurer-sourced alternatives on the points that matter at claim time, and still generate more long-term profit than the traditional markup model provides.

The Customer Experience Impact

A dealer who offers genuinely competitive GAP removes the adversarial dynamic at the finance desk. The customer isn't being upsold a commoditized product at an inflated margin. They're getting coverage that stands up to comparison — and that changes how customers remember the dealership after a claim.

DealerRE has helped more than 400 dealers build admin obligor reinsurance programs since 1994, replacing third-party F&I products (including GAP) with dealer-owned programs that retain what third-party providers have historically kept for themselves.

For dealers evaluating this model, the practical question is whether your GAP program is structured to be genuinely competitive at the point of sale — and whether you're capturing the underwriting profit that structure is designed to generate.

Frequently Asked Questions

Should you buy gap insurance from a dealer?

Dealer GAP can be worth it when the product terms are favorable: no deductible out-of-pocket, full negative equity coverage, and high LTV limits. Compare the dealer's specific terms and total financed cost directly against your auto insurer's GAP endorsement before deciding — price alone doesn't capture the full picture.

Is dealer gap insurance more expensive than insurer gap insurance?

Dealer GAP typically costs more upfront — $500–$700 as a flat fee, often financed — while insurer GAP endorsements run $20–$150 per year. Coverage differences matter too: insurer GAP rarely covers your deductible, may exclude rolled-in negative equity, and Progressive caps payouts at 25% of ACV.

Can you cancel gap insurance purchased from a dealer?

Yes. The CFPB confirms buyers can cancel optional add-on products at any time, with most contracts offering a 30-day full refund and prorated refunds after that. If your loan is active, the refund applies to your balance — check your contract for specifics.

Does dealer gap insurance cover your deductible?

Well-structured dealer GAP policies typically cover the underlying insurance deductible — DealerRE's program covers it up to $1,000. Insurer-sourced GAP does not cover the deductible; your payout is reduced by the deductible amount, leaving you responsible for $500–$1,000 out of pocket at claim time.

When does gap insurance make financial sense?

GAP coverage makes the most sense with low or no down payment, loan terms of 60+ months, negative equity rolled in from a trade-in, or rapidly depreciating vehicles like EVs and luxury models. If your loan balance already sits below ACV, coverage is harder to justify.

Can a dealer require you to purchase gap insurance to get financing?

No. GAP is optional unless the lender specifically requires it — in which case the cost must be disclosed in the finance charge and reflected in the APR. The CFPB is clear that dealers cannot make optional add-on products a condition of purchase; buyers always have the right to decline.