Introduction

When a borrower finances a vehicle, the lender requires them to maintain comprehensive and collision coverage — full stop. But what happens when that coverage lapses, gets cancelled, or was never properly set up in the first place?

That's where collateral protection insurance (CPI) steps in. CPI is the lender's safety net: a force-placed policy that kicks in when a borrower's required insurance disappears. The lender places it, but the borrower pays for it — and it's almost always more expensive than the coverage it replaces.

This article covers both sides of the equation. For borrowers, it's about understanding the financial consequences of letting coverage lapse. For BHPH dealers and auto lenders who carry their own paper, CPI is a risk management tool that protects their collateral portfolio — and, structured correctly, a source of retained underwriting profit.

TLDR

- CPI is lender-placed insurance that activates when a borrower's required coverage lapses — it protects the lender, not the borrower

- It covers physical damage (comprehensive and collision) only — no liability, no medical, no UM/UIM

- Costs range from $2,000–$6,000 per year, often more than standard full-coverage insurance

- CPI is legal and enforceable under the 1996 NAIC Creditor-Placed Insurance Model Act

- BHPH dealers can reinsure CPI through their own company to retain underwriting profits

What Is Collateral Protection Insurance (CPI)?

CPI is a lender-placed policy activated when a borrower fails to maintain the comprehensive and collision coverage required by their loan agreement. Its sole purpose is to protect the lender's financial interest in the vehicle — not the borrower's liability exposure, not their medical costs.

The lender or dealer purchases the policy and advances the premium. That cost gets added to the borrower's loan balance, collected through higher monthly payments or an extended loan term. The borrower pays for coverage that only the lender can use.

How CPI Differs from Standard Auto Insurance

| Feature | Standard Auto Insurance | Collateral Protection Insurance |

|---|---|---|

| Who purchases it | Borrower | Lender/dealer |

| Who it protects | Borrower (liability, damages, medical) | Lender's collateral interest only |

| When it activates | At policy purchase | When borrower's coverage lapses |

| Liability coverage | Yes | No |

| Competitively priced | Yes | No — lender selects terms |

| Satisfies state minimums | Yes | No |

The CFPB's Supervisory Highlights explicitly notes that CPI and force-placed insurance (FPI) are interchangeable terms for the same product. Other common names include creditor-placed insurance and lender-placed insurance — all describe the same mechanism, applicable to auto loans and other financed assets.

Even with CPI active on their account, borrowers remain legally uninsured for driving purposes. CPI covers the lender's interest in the physical vehicle — it does not satisfy any state financial responsibility law. A borrower driving with only CPI in place is still subject to fines, license suspension, or worse.

For dealers, that gap matters. If a borrower defaults after an at-fault accident and carries no personal liability coverage, the collateral recovery picture changes significantly.

How Does CPI Work?

The Trigger

CPI activates when an insurance tracking system flags that a borrower's policy has lapsed, been cancelled, or never listed the financed vehicle with the required coverages. Most lenders monitor this continuously through third-party tracking platforms that alert them to coverage gaps as they occur.

The Notification Process

Before placing CPI, lenders are required to notify the borrower — typically by mail — giving them a chance to provide proof of their own coverage. Per Bankrate's analysis of CPI programs, a declarations page is required, not just an insurance ID card. The distinction matters: an ID card doesn't confirm coverage levels or that the financed vehicle is listed.

How It Gets Added to the Loan

Once placed, the CPI premium gets tacked onto the loan balance. Per NCUA guidance, the premium should be amortized over the life of the CPI policy — not the full remaining loan term — so the borrower fully reimburses the lender by the time the policy expires. This results in higher monthly payments — sometimes significantly.

What Happens If CPI Is Placed in Error

If a borrower had continuous qualifying coverage during the period in question, they can request a refund. The lender cancels the CPI and reverses charges once valid proof is confirmed. Any genuine gap period — where coverage was actually absent — may still carry a charge.

Regulatory requirements back this up: the NAIC Model Act Section 9 mandates a refund of unearned premiums whenever placement was in error.

Consequences of Non-Payment

The premium is folded into the loan payment, so refusing to pay it puts the borrower at risk of:

- Loan default

- Vehicle repossession

- Credit score damage

- Compounding fees and interest on the added balance

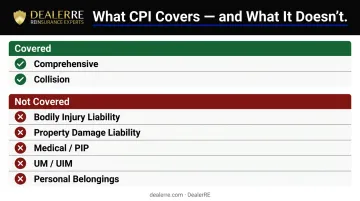

What CPI Covers — and What It Doesn't

What CPI Covers

According to AutoInsurance.com, CPI provides physical damage coverage through two components:

- Comprehensive — Non-collision events including theft, fire, weather damage (hail, flooding), vandalism, and animal strikes. Personal belongings inside the vehicle are not covered; CPI protects the lender's interest in the vehicle itself, nothing more.

- Collision — Damage from the vehicle striking another vehicle or a fixed object, regardless of fault. Damage to the other party's vehicle or property is not included — that falls under liability, which CPI explicitly excludes.

Coverage is also capped at the outstanding loan balance, not the vehicle's full market value, per NAIC Model Act Section 5.

CPI Coverage at a Glance

| Coverage Type | Included in CPI? |

|---|---|

| Comprehensive (theft, fire, weather) | ✅ Yes |

| Collision damage | ✅ Yes |

| Bodily injury liability | ❌ No |

| Property damage liability | ❌ No |

| Medical payments / PIP | ❌ No |

| Uninsured/underinsured motorist | ❌ No |

| Personal belongings | ❌ No |

The liability exclusions matter beyond the borrower. A dealer or lender administering CPI needs to understand exactly where coverage stops — because when a borrower causes an accident without separate liability coverage, no part of that claim flows back through CPI. The lender's collateral is protected; everything else is the borrower's problem alone.

How Much Does CPI Cost?

CPI is expensive — and the borrower has no ability to shop around or negotiate. The lender selects the vendor, the coverage level, and the terms.

Cost Ranges

Two industry sources provide the clearest benchmarks:

- Unitas360 (2025): Average of $2,000–$3,000 per year per vehicle

- AutoInsurance.com (2025): Broader range of $200–$500 per month ($2,400–$6,000 annually)

Compare that to the average full-coverage personal auto insurance policy, which ran $1,984 per year according to ValuePenguin's 2024 analysis. Even at the low end of CPI pricing, the borrower is paying as much as or more than a standard policy — and getting significantly less protection.

What Drives CPI Pricing

- Outstanding loan balance — coverage is capped at net debt

- Lender's chosen vendor — the borrower has no say

- Coverage level — comprehensive only vs. comprehensive plus collision

- State regulatory requirements — premium structures vary by jurisdiction

- Borrower's risk profile — higher-risk portfolios typically mean higher rates

For dealers and BHPH lenders administering CPI programs, these benchmarks carry real weight. At $2,000–$6,000 per vehicle annually, CPI generates meaningful premium volume — which is precisely why how that premium is structured and who captures the underwriting profit matters as much as the rate itself.

Is CPI Legal?

Yes — with a significant history behind that answer.

The Litigation Wave

During the 1980s and 1990s, CPI became what one legal analysis described as a "cottage industry" for plaintiffs' class action lawyers. Most major lenders faced litigation alleging violations of TILA, RICO statutes, and the Bank Holding Company Act.

Claims centered on undisclosed lender commissions from CPI providers, hidden fees, and improper premium refund calculations. The vast majority of these cases settled without a merits determination, and some lenders abandoned CPI programs entirely rather than face continued litigation.

The 1996 NAIC Model Act

The National Association of Insurance Commissioners responded with the Creditor-Placed Insurance Model Act (MO-375-1), adopted in October 1996. The Act established a compliance framework with specific requirements:

- Section 5: Coverage capped at outstanding loan balance (net debt)

- Section 6: Prohibited coverages (repossession, skip, conversion)

- Section 9: Mandatory refund of unearned premiums

- Section 13: Required disclosures to the borrower before placement

This framework gave lenders a clear compliance framework — and courts have upheld properly administered CPI programs. In Kenty v. Bank One, the Sixth Circuit sided with the lender when the loan contract clearly authorized the insurance placement.

Compliance failures, however, carry real consequences. In July 2024, the CFPB ordered Fifth Third Bank to pay approximately $20 million in penalties for placing duplicative and unnecessary force-placed insurance on over 800,000 auto loan accounts. A well-designed program that follows the Model Act is enforceable — sloppy administration turns that same program into a significant liability.

What CPI Means for BHPH Dealers

The Exposure Problem

Buy here pay here dealers are uniquely positioned: they're simultaneously the seller and the lender. When a customer lets their insurance lapse — and in the BHPH segment, this happens regularly — the dealer's asset is sitting unprotected on the road.

The numbers show how widespread the problem is. According to the Insurance Information Institute's 2025 data, 15.4% of all motorists were uninsured in 2023, and one in three drivers (33.4%) was either uninsured or underinsured.

In a BHPH portfolio concentrated in subprime borrowers — where Federal Reserve research shows 78% of lending volume goes to subprime borrowers and delinquency rates run at 10% versus 3.8% for traditional lenders — lapse risk runs structurally higher than those national averages.

CPI as a Risk Management Layer

CPI gives BHPH dealers a mechanism to force-place coverage when a customer's policy lapses and recoup the cost from the borrower. The lender advances the premium, adds it to the loan balance, and the customer funds the protection on the dealer's collateral.

CPI is one layer, not a complete solution. It addresses physical damage exposure — but not mechanical breakdown risk, which is a separate exposure in any BHPH portfolio.

The Reinsurance Angle: Retaining the Profit

Under a traditional third-party CPI arrangement, the dealer places coverage through an external vendor — and that vendor keeps the underwriting profit. If the vendor weren't making money on the program, they wouldn't offer it.

DealerRE's dealer-owned reinsurance model flips that structure. BHPH dealers who reinsure CPI through their own company capture the underwriting profits instead of sending them to a third party.

Customers still pay the CPI premium each month — the difference is where that money accumulates. Instead of funding an external provider's margin, it builds inside the dealer's own reinsurance company.

The same structure can be extended across multiple product lines, turning a siloed CPI program into a comprehensive portfolio:

- Vehicle service contracts — mechanical breakdown protection funded by the customer base

- GAP coverage — protects the loan balance gap in a total loss

- Debt cancellation coverage (DCC) — an alternative to GAP with different regulatory treatment

For dealers who have been treating CPI as a pure expense, the reinsurance model reframes it as a profit center.

Frequently Asked Questions

What is the difference between CPI and a standard auto insurance policy?

Standard auto insurance is purchased by the borrower, covers liability, medical expenses, and physical damage, and can be competitively shopped. CPI is placed by the lender, protects only the lender's financial interest in the vehicle, excludes all liability coverage, and typically costs more — with no ability for the borrower to negotiate terms.

Is collateral protection insurance legal?

Yes. CPI is legal and enforceable when authorized by the underlying loan agreement. The 1996 NAIC Creditor-Placed Insurance Model Act established the compliance framework lenders must follow, and courts have upheld properly administered programs — though compliance failures carry significant regulatory and financial risk.

How much does CPI typically cost?

Industry sources cite a range of $2,000–$3,000 per year on average, with broader ranges up to $6,000 annually depending on the lender's vendor and program. This frequently equals or exceeds the cost of a standard full-coverage policy — making borrower-maintained coverage with proof of insurance the less expensive path by a significant margin.

What does collateral protection insurance not cover?

CPI does not cover bodily injury liability, property damage liability, medical payments, or uninsured/underinsured motorist exposure. It covers physical damage to the vehicle only. Borrowers with CPI as their sole coverage remain uninsured for driving purposes and in violation of state financial responsibility laws.

Can a BHPH dealer require CPI on financed vehicles?

Yes. BHPH dealers who carry their own paper function as the lender and can require borrowers to maintain insurance and force-place CPI when coverage lapses — provided the loan agreement authorizes placement and the program complies with applicable state regulations.

How does a dealer track borrower insurance to know when to place CPI?

Lenders typically use third-party insurance tracking platforms that monitor policy status continuously. When a borrower's coverage lapses or fails to meet required levels, the system alerts the lender and triggers the notification and placement process outlined under the NAIC Model Act.