Introduction

For many car buyers, the surprise hits weeks or months after driving off the lot: an unfamiliar line item on the monthly loan statement labeled "CPI," sometimes adding $150–200 to the payment. This stands for Collateral Protection Insurance—a force-placed insurance product that lenders purchase when borrowers fail to maintain required coverage on financed vehicles. Unlike the insurance policies buyers choose, CPI protects the lender's interest first, not the driver's, and borrowers pay the premium without enjoying the full benefits.

For buyers, knowing when and why CPI appears—and how to remove it—can save hundreds of dollars per month. Catching it early matters because most lenders don't remove back-charged premiums automatically.

For dealers, proper disclosure and compliant use of CPI protects against regulatory exposure while maintaining portfolio stability. This article covers what CPI is, when it's placed, what it costs and covers, how to remove it, and what dealers need to understand about using it compliantly within their F&I operations.

TLDR

- CPI is force-placed by lenders when borrowers lack required comprehensive and collision coverage on financed vehicles

- Borrowers pay the premiums, but the policy protects the lender's collateral—not the driver

- CPI excludes liability insurance, leaving borrowers legally uninsured under state financial responsibility laws

- To remove CPI, borrowers must secure qualifying personal auto insurance and submit proof to the lender

- Dealers offering CPI must meet TILA/Regulation Z disclosure standards or face significant legal exposure

What Is CPI? Understanding Collateral Protection Insurance

Collateral Protection Insurance is a type of force-placed insurance that auto lenders purchase on financed vehicles when borrowers fail to carry required comprehensive and collision coverage. Unlike insurance policies consumers select and purchase directly, CPI is placed without the borrower's input by the lender—the borrower doesn't choose it, doesn't shop for it, and often doesn't know about it until charges appear.

Why Lenders Use CPI

When a buyer finances a vehicle, that vehicle serves as collateral securing the loan. If the borrower damages or totals the car without maintaining insurance, the lender cannot recover the loan balance from the damaged collateral. CPI covers that exposure by protecting the lender's financial interest in the vehicle against physical damage risks including fire, theft, collision, and other hazards.

When CPI Gets Placed

Understanding when CPI is placed helps lenders and dealers stay ahead of the process. Two scenarios typically trigger it:

- At origination — The buyer cannot or does not provide proof of insurance before leaving the lot

- Post-origination — The lender discovers the borrower's policy has lapsed or been canceled

The most common point of friction: borrowers pay the CPI premium, but the policy protects the lender's interest, not the driver's.

According to the CFPB, force-placed insurance is something "a lender obtains to cover a vehicle when a borrower fails to obtain or maintain required insurance—it protects only the lender, not the borrower, and the lender charges the borrower for the cost." That distinction must be disclosed clearly to avoid claims of unfair or deceptive practices.

Other names for CPI in loan documents:

- Force-placed auto insurance

- Lien protection insurance

- Auto loan protection insurance

- Creditor-placed insurance

How CPI Works at the Dealership

The Legal Foundation

The loan agreement contains specific language granting the lender the right to place CPI if insurance requirements aren't met. This contractual clause forms the legal foundation for adding CPI charges to the account.

Finance contracts generally require borrowers to maintain comprehensive and collision insurance throughout the loan term. They explicitly state that failure to do so allows the servicer to purchase coverage at the consumer's expense.

Post-Origination Monitoring

After loan origination, lenders monitor insurance coverage through electronic databases or manual tracking systems. When these systems indicate a lapse or inadequate coverage, the servicer sends a notice requesting proof of insurance. If the borrower doesn't respond within the required timeframe (typically 20-30 days depending on state law), the servicer purchases and activates CPI.

What Happens When CPI Is Placed

Once triggered, the lender purchases the CPI policy and adds the premium directly to the borrower's monthly payment. The mechanics work as follows:

- The lender obtains coverage from an insurance provider

- Premiums are charged to the borrower's loan account

- Monthly payments increase to cover the CPI cost

- The cost may be backdated to cover the period when the vehicle was uninsured, creating a sudden, significant balance owed

State regulations permit lenders to backdate premiums to the exact date coverage lapsed. This retroactive billing can accumulate for several months before a borrower discovers the charge, resulting in payment shock when hundreds or thousands of dollars appear on the account balance .

The Off-Ramp for Borrowers

CPI isn't permanent. Once a borrower obtains a qualifying personal insurance policy and provides proof to the lender, the CPI is canceled.

Refund rights depend on the circumstances:

- Overlap period: State insurance regulations require lenders to provide prorated refunds for any period when both CPI and personal coverage existed simultaneously.

- CPI placed in error: If coverage was continuous and CPI was added incorrectly, borrowers are entitled to a full refund of all premiums paid.

What CPI Covers, What It Costs, and What It Doesn't Include

Coverage Overview

CPI typically mirrors comprehensive and collision insurance, covering physical damage to the vehicle from accidents, theft, vandalism, and natural disasters. The policy protects the lender's financial interest by ensuring the collateral maintains value throughout the loan term.

The Critical Liability Gap

CPI does not include liability insurance. This exclusion creates a dangerous misunderstanding. A borrower driving under CPI-only coverage remains uninsured under state financial responsibility laws, meaning:

- They can receive tickets for driving without insurance

- They remain personally liable for damage or injury caused to others

- License suspension is possible for failure to maintain required coverage

Pennsylvania's DMV explicitly warns: "Insurance maintained by the lien holder is not liability insurance: it only protects the lender. Collateral protection insurance is not an acceptable form of insurance." California's DMV confirms: "Comprehensive or collision insurance does not meet vehicle financial responsibility requirements."

Cost Structure and Comparison

CPI premiums are calculated based on the total loan amount rather than the borrower's driving history or credit score. The CFPB found that under one major bank's program, CPI cost roughly 14% of the outstanding loan balance, resulting in average annual premiums between $1,703 and $1,847. That translates to nearly $200 added to monthly payments.

Comparison Example:

| Coverage Type | Typical Monthly Cost | Annual Cost |

|---|---|---|

| Standard Full Coverage (comp + collision + liability) | $100–150 | $1,200–1,800 |

| CPI (comp + collision only, no liability) | $140–200+ | $1,700–2,400+ |

Most states cap CPI rates and require insurers to file rate schedules with state insurance departments. The NAIC Model Act presumes rates are reasonable if they produce a loss ratio of 60% or greater, but even compliant rates remain significantly higher than what borrowers could obtain independently.

Backdating Risk Example

Compliant rates are only part of the problem. Backdating practices can push costs even higher—often without warning.

In a Department of Justice complaint against National General, investigators documented how backdated force-placed policies created sharp payment increases. Because annual premiums (approximately $1,100) were amortized over the remaining policy term of about seven months after backdating, monthly payments increased by an average of 25%.

Consider the practical impact: a borrower whose coverage lapsed in January but wasn't notified until April could suddenly face a $1,100 charge split over eight months. That adds $137 per month on top of the regular CPI premium going forward.

How to Remove CPI from Your Loan

Steps to Remove CPI

Removing CPI follows a simple sequence:

- Review your loan contract to confirm the coverage type and minimum limits required (usually comprehensive and collision with specific deductible caps)

- Shop for a qualifying personal auto insurance policy from a provider of your choice

- Obtain proof of insurance documentation including declarations page with VIN, policy number, coverage details, effective dates, and lienholder information

- Submit documentation to your lender via the method specified in your loan agreement (mail, fax, online portal)

State laws grant borrowers the explicit right to cancel CPI by providing proper evidence of required insurance. Once the lender confirms continuous coverage, CPI must be canceled, generally within 15 days of receiving documentation.

Getting a Refund for Overlapping CPI Charges

If your lender placed CPI while you actually maintained qualifying coverage, you're entitled to a full refund for premiums paid during the overlap period. To pursue this:

Gather documentation:

- Your insurance declarations pages showing continuous coverage dates

- CPI placement notices from the lender (with dates)

- Loan statements showing CPI charges

Submit a dispute:

- Contact your lender's customer service department

- Reference the specific dates of continuous coverage

- Request immediate cancellation and full refund

The CFPB has identified this scenario as an unfair practice, noting that servicers caused substantial injury by maintaining CPI charges when consumers had adequate insurance in place.

Disputing Improper CPI Charges

CPI placed after a genuine coverage lapse is legal — but not every placement is legitimate. Dispute charges in these situations:

- CPI added despite continuous qualifying coverage on your end

- CPI placed without required advance warning (20-30 days depending on your state)

- Charges exceeding state-approved rate caps

- Lender refusing to cancel or issue a refund after you've submitted proof of insurance

If the lender doesn't respond appropriately, file complaints with the Consumer Financial Protection Bureau and your state insurance department.

What Dealers Need to Know: CPI Compliance and Risk Management

The Disclosure Requirement

Under TILA/Regulation Z (12 CFR 1026.4(d)(2)), CPI premiums may be excluded from the finance charge only if two conditions are met:

- The insurance coverage may be obtained from a person of the consumer's choice, and this fact is disclosed

- If coverage is obtained from or through the creditor, the premium for the initial term must be disclosed in writing

Failure to meet these disclosure standards means the CPI premium must be reclassified as part of the finance charge—a costly compliance error that can trigger APR disclosure violations and potential TILA penalties.

Required disclosures at loan origination must clearly state:

- CPI may be placed if insurance lapses

- The customer has the right to obtain insurance from a provider of their choice

- The CPI premium amount if placed

- CPI does not include liability coverage or satisfy state financial responsibility laws

Warning Against Indiscriminate Force-Placement

CFPB enforcement actions demonstrate the serious legal exposure dealers face when force-placing CPI improperly. In 2024, Fifth Third Bank faced a $5 million penalty for placing duplicative CPI on borrowers who already maintained insurance. Wells Fargo's 2018 settlement exceeded $1 billion for unlawfully force-placing unnecessary CPI on hundreds of thousands of borrowers, leading to wrongful repossessions.

Under UDAAP, charging consumers for unnecessary CPI constitutes an Unfair act or practice—it causes substantial injury (fees, delinquency, repossession) that consumers cannot reasonably avoid and provides no countervailing benefit.

Per consumer credit law including UCCC unconscionability provisions, requiring CPI on buyers who already have insurance or can obtain it exposes dealers to significant legal risk. The practice provides zero benefit to consumers while exceeding the creditor's legitimate need for collateral protection.

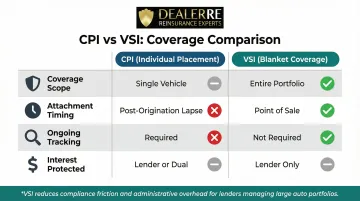

The VSI Alternative

Vendor's Single Interest (VSI) coverage can reduce compliance friction for lenders managing large portfolios:

| Feature | CPI (Individual Placement) | VSI (Blanket Coverage) |

|---|---|---|

| Coverage scope | Individual vehicle when borrower coverage lapses | Blanket coverage across lender's entire eligible portfolio |

| Attachment timing | Post-origination upon lapse | Point of sale / loan origination |

| Ongoing tracking required | Yes—continuous monitoring of borrower policies | No ongoing tracking required |

| Interest protected | Single (lender) or dual (lender & borrower) | Single interest (lender only) |

VSI is insurance purchased by financial institutions that protects against financial loss from physical damage to collateral. It covers only the outstanding loan balance—borrowers receive no protection for their equity.

California regulations explicitly permit credit unions to obtain blanket VSI policies, provided the premium is paid by the credit union and not charged to borrowers individually.

Critical distinction: When properly structured, VSI eliminates the need for post-origination tracking and complex refund processing. However, proper disclosure remains mandatory, and state law must permit the structure.

F&I Strategy and Reinsurance Programs

Both CPI and VSI rely on third-party providers who retain underwriting profits. Dealers with well-structured F&I programs—including dealer-owned reinsurance arrangements—can manage collateral protection directly and keep those profits in-house.

Companies like DealerRE specialize in helping independent and Buy Here Pay Here dealers set up admin obligor reinsurance programs. Instead of sending CPI premiums to external insurance companies, dealers route them to their own reinsurance entity. Key advantages of this structure include:

- Captures underwriting profits that would otherwise go to third-party providers

- Maintains claims administration and regulatory compliance in-house

- Transforms collateral protection from a cost center into a revenue stream

- Gives dealers direct control over claims outcomes and customer relationships

For dealers selling 30+ vehicles monthly, this approach provides greater control over claims outcomes, customer relationships, and financial performance compared to sourcing coverage from outside providers.

Frequently Asked Questions

Why was CPI added to my car loan?

CPI is added when the lender determines you don't have the required comprehensive and collision coverage on the financed vehicle, either at origination or after a coverage lapse. You pay the premium, not the lender, and the charge continues until you secure qualifying personal insurance.

Can I get CPI removed?

Yes. Purchase a qualifying personal auto insurance policy meeting your loan contract's coverage requirements and submit proof to the lender. Once confirmed, CPI is canceled and any overlap period is typically refunded within 14–30 days.

When should I dispute a CPI charge?

CPI placed after a genuine coverage lapse is legitimate. Dispute it if it was added while you maintained qualifying coverage, applied without the required advance notice, or billed at rates exceeding state-approved caps.

Does CPI cover me as a driver?

No. CPI only covers the vehicle (the lender's collateral) and does not include liability insurance. Relying solely on CPI means you remain technically uninsured under state law and face fines, license suspension, or personal liability for damages caused to others.

Is CPI insurance legal?

CPI is legal and enforceable when placed with proper disclosure and in compliance with state insurance regulations. Force-placing it on borrowers who already maintain coverage — or skipping required notice — exposes lenders and dealers to CFPB enforcement actions and UDAAP liability.

For buyers, knowing your rights prevents unnecessary charges and keeps your coverage compliant. For dealers, CPI done right — with proper disclosure and a well-structured reinsurance program — protects your portfolio without creating regulatory exposure. If you're a dealer looking to build a compliant CPI program and keep more of the underwriting profit, contact DealerRE at (804) 824-9533 to learn about admin obligor reinsurance solutions.