Introduction

When a borrower finances a vehicle, the lender holds a direct financial stake in that asset. The loan agreement requires the borrower to maintain comprehensive and collision coverage — but borrowers lapse, cancel, or simply never obtain the required insurance. When that happens, the lender's collateral sits exposed.

Collateral Protection Insurance (CPI) is how lenders close that gap. It's a standard tool across auto lending, yet BHPH operators who carry their own paper often run into it without a full understanding of how it works, what it costs, or what compliance looks like at the portfolio level.

This guide covers what CPI is, when it gets triggered, what it covers, and what dealers need to know about protecting their loan portfolios with it.

TL;DR

- CPI is force-placed by a lender when a borrower fails to maintain required insurance on a financed vehicle

- It protects the lender's financial interest — not the borrower's liability, medical expenses, or personal property

- The premium is added to the borrower's loan balance, raising monthly payments or extending the loan term

- Borrowers remove CPI by submitting valid proof of insurance — the lender cancels the policy and refunds any unused premium

- BHPH dealers carrying their own paper face the same collateral exposure as any lender, and structured CPI programs can protect their portfolios while retaining underwriting profit

What Is Collateral Protection Insurance?

The NAIC Creditor-Placed Insurance Model Act (MO-375) defines creditor-placed insurance as coverage "purchased unilaterally by a creditor who is the named insured" to protect against "loss, expense, or damage to collateralized personal property resulting from fire, theft, collision, or other risks that would either impair a creditor's interest or adversely affect the value of collateral."

In plain terms: if a borrower stops insuring the vehicle the lender financed, the lender has a problem. CPI transfers that risk to an insurer when the borrower fails to do so. It's also called force-placed insurance, lender-placed insurance, or creditor-placed insurance — all referring to the same mechanism.

What CPI Is Not

CPI is narrowly scoped to protecting the lender's collateral interest — nothing more. Borrowers who assume it functions like a personal auto policy often find out otherwise at the worst time:

- Not a substitute for full personal auto insurance — it doesn't cover the borrower's liability to third parties

- Not GAP insurance — GAP covers the difference between the vehicle's actual cash value and the remaining loan balance at total loss; CPI covers physical damage when the borrower's own insurance lapses

- Not proof of financial responsibility — CPI does not satisfy any state's minimum liability requirements

In practice, a borrower may need both: CPI if their coverage lapses mid-loan, and GAP if their vehicle is totaled while they owe more than it's worth.

The Regulatory Foundation

CPI programs didn't always operate within consistent standards. During the 1980s and 1990s, class-action litigation exposed widespread abuses — lenders charging premiums that exceeded actual coverage costs, taking undisclosed commissions, and backdating coverage without notice. Cases like Acree v. GMAC and Kenty v. Bank One exposed kickback arrangements and premium overcharges that harmed borrowers while enriching lenders.

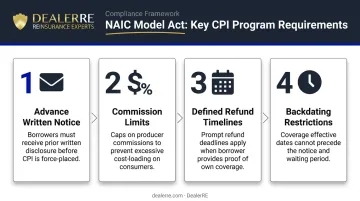

The 1997 NAIC Model Act established the compliance framework that governs CPI today. Key requirements include:

- Advance written notice to borrowers before coverage is placed

- Commission limits on lender-received compensation

- Defined refund timelines when borrowers restore their own coverage

- Restrictions on how far policies can be backdated

Single-Interest vs. Dual-Interest CPI

The type of policy a lender selects has real consequences for borrowers:

| Policy Type | Who It Protects | When It Activates |

|---|---|---|

| Single-interest | Lender only | Requires default, repossession, and impaired lender interest |

| Dual-interest (limited) | Lender + some borrower benefit | Activates while vehicle is still in borrower's possession |

Dual-interest policies can allow claim payments to fund vehicle repairs rather than simply compensating the lender — a meaningful distinction for borrowers trying to maintain a vehicle they still need.

How Does Collateral Protection Insurance Work?

CPI follows a defined sequence: insurance tracking, notice, force-placement, and resolution. Each stage carries regulatory requirements under the NAIC Model Act and applicable state law.

When CPI Gets Triggered

At origination, borrowers agree to maintain comprehensive and collision coverage and list the lender as lienholder. Lenders — or their CPI providers — use automated tracking systems to monitor coverage status throughout the loan term.

Modern CPI programs rely on Electronic Data Interchange (EDI) to receive real-time policy updates from insurance carriers. Platforms like SWBC's AutoPilot and automated verification tools monitor coverage status across entire loan portfolios in real time, flagging lapses as they occur rather than waiting for borrowers to self-report.

When coverage lapses, expires, or cannot be confirmed, the tracking system flags the account and triggers the notice process.

The Force-Placement Process

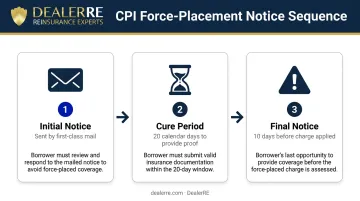

The NAIC Model Act requires lenders to give borrowers a genuine opportunity to respond before force-placing coverage:

- Initial notice — sent by first-class mail, informing the borrower of the insurance requirement

- Cure period — borrower has at least 20 calendar days to provide proof of acceptable coverage

- Final notice — sent at least 10 calendar days before any charge is applied; must state explicitly that insurance will be purchased and charged to the account if the borrower does not respond

If the borrower doesn't respond, the lender force-places a CPI policy. The premium is added to the borrower's loan principal — increasing monthly payments or extending the loan term. The borrower cannot shop for a better rate or select coverage terms. The policy is entirely the lender's choice, protecting the lender's interest.

Backdating applies here as well: CPI premiums can be backdated to the date the borrower's prior coverage lapsed, closing the gap retroactively. Under the NAIC Model Act, backdating cannot exceed one year before the charge is applied to the account.

How CPI Resolves

CPI ends when the borrower provides valid proof of comprehensive and collision coverage — typically the declarations page of an active policy naming the lender as lienholder. Once confirmed, the lender must:

- Cancel the force-placed CPI policy

- Refund any unused premium within 60 calendar days

- Issue a refund statement disclosing the effective date, termination date, and amount refunded

Refunds are prorated from when proof is confirmed — not retroactively from when the coverage gap began. Any period during which the vehicle was genuinely uninsured may still carry a CPI charge the borrower cannot recover — which is precisely why lenders depend on CPI to close the collateral exposure gap that voluntary coverage alone cannot guarantee.

What CPI Covers — and What It Doesn't

CPI provides physical damage coverage on the financed vehicle. That means:

Typically covered:

- Collision damage (impacts with other vehicles or fixed objects)

- Comprehensive damage (theft, vandalism, fire, weather events, falling objects)

Not covered:

- Borrower liability to third parties (property damage or bodily injury caused to others)

- Medical payments or Personal Injury Protection (PIP) for the borrower

- Personal property inside the vehicle

- Loan balance exceeding the vehicle's actual cash value

As the AVP CPI program disclosure states directly: "Collateral Protection Insurance does not provide bodily injury, no fault or liability insurance and does not comply with any state financial responsibility law."

A borrower driving under CPI alone is still legally uninsured from a liability standpoint — and legally exposed in every state.

Post-Repossession Coverage and Compliance Risk

The coverage gaps above affect borrowers — but CPI programs also carry lender-side risks that are easy to overlook. Some CPI policies include lender-specific coverages that apply after repossession, protecting the lender against damage that happens during or after the repossession process. This is a legitimate use of single-interest CPI.

Where programs run into trouble is when lenders charge borrowers for coverage on vehicles already in the lender's possession. The CFPB's July 2024 consent order against Fifth Third Bank resulted in approximately $20 million in civil penalties and $3.6 million in consumer restitution — partly for charging CPI premiums on already-repossessed vehicles. Getting the timing and billing right isn't a technicality — it's the difference between a compliant program and a regulatory enforcement action.

CPI and the Auto Dealer: What Dealers Need to Know

The BHPH Collateral Exposure Problem

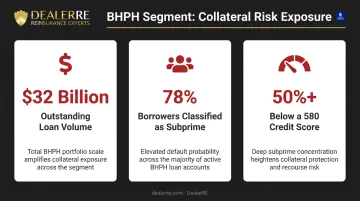

BHPH dealers who carry their own retail installment contracts are, functionally, lenders. They hold the financial interest in every vehicle on their lot that's been sold on credit — and that exposure is significant.

Federal Reserve data shows the BHPH segment carries approximately $32 billion in outstanding loan volume, with 78% of borrowers classified as subprime and more than half below a 580 credit score. These borrowers face real financial pressure — the same pressure that leads insurance policies to lapse. An uninsured vehicle that gets totaled, stolen, or seriously damaged doesn't just hurt the borrower; it directly hits the dealer's receivables.

The practical problem is direct: dealers require full coverage insurance, but spend significant staff time chasing proof of insurance — essentially acting as collections agents for third-party insurers just to verify their collateral is protected.

How Dealer-Owned CPI Reinsurance Changes the Math

CPI programs can be structured differently from simply purchasing force-placed coverage from a third-party provider. Through an admin obligor reinsurance structure — the type DealerRE has offered since 1994 — BHPH dealers can reinsure CPI through their own dealer-owned reinsurance company.

The mechanics: instead of sending CPI premiums to a third-party insurer, the dealer routes them into their own reinsurance company. Claims are adjudicated through an administrator (DealerRE works with Assured Vehicle Protection), but the underwriting profit — premiums collected minus claims paid — stays with the dealer instead of flowing to an outside provider.

This converts what was previously a cost of doing business into a revenue-generating program funded by the customer base. The collateral protection is the same; what changes is who captures the profit from providing it.

DealerRE also offers complementary products for BHPH dealers managing total-loss exposure:

- Debt Cancellation Coverage (DCC) — sold proactively as an alternative to requiring full coverage insurance; covers the total debt owed at total loss and typically costs less for customers than standard comprehensive and collision coverage

- GAP reinsurance — covers the shortfall between insurance payout and remaining loan balance at total loss

- Vendor Single Interest (VSI) — protects lenders when a vehicle is damaged and the borrower lacks required coverage, and can include repossession-related costs

State, Federal, and NAIC Compliance Obligations

Any dealer operating a CPI-adjacent program must stay current on applicable state laws, NAIC Model Act requirements, and federal consumer protection regulations. The required notice sequence, refund timelines, commission restrictions, and backdating limits aren't optional — and the CFPB has demonstrated willingness to pursue enforcement in this space.

DealerRE manages legal forms, filings, tax returns, and renewals for dealer-owned reinsurance companies, and partners with outside CPAs and legal counsel to keep programs compliant. Dealers interested in whether a program applies in their state can confirm availability directly — program eligibility varies by state law.

Frequently Asked Questions

Is collateral protection insurance the same as GAP insurance?

No — they're distinct products. CPI covers physical damage to the vehicle when the borrower's insurance lapses, protecting the lender's collateral interest. GAP covers the shortfall between the vehicle's actual cash value and the remaining loan balance at total loss. A borrower could need both if they let coverage lapse and their vehicle is totaled while they still owe more than it's worth.

How do I get rid of collateral protection insurance?

Provide your lender with valid proof of comprehensive and collision coverage — typically the declarations page of an active policy that names the lender as lienholder. Once the lender confirms coverage, they're required to cancel the CPI policy and refund any unused premium within 60 calendar days.

Is collateral protection insurance proof of insurance?

No. CPI is the lender's unilateral policy protecting their own financial interest. It does not meet state minimum liability requirements, does not satisfy any legal proof-of-insurance obligation, and provides no liability, medical, or personal coverage for the borrower. Drivers relying solely on CPI are legally uninsured.

Who pays for collateral protection insurance?

The lender initially pays the premium, then passes the cost to the borrower by adding it to the loan principal, resulting in higher monthly payments or a longer loan term.

What does collateral protection insurance cover?

CPI covers physical damage to the financed vehicle — collision and comprehensive — protecting against accidents, theft, vandalism, fire, and weather damage. It does not cover the borrower's liability to others, personal injuries, personal property inside the vehicle, or any loan balance exceeding the vehicle's actual cash value.

Why is collateral protection insurance so expensive?

CPI premiums run higher than standard auto insurance because the borrower has no ability to shop rates — the lender selects the policy entirely. Insurers price in the adverse selection risk of covering borrowers who already let coverage lapse, and administrative costs for tracking, notices, and refund processing add to the overall expense.