Introduction

Every BHPH dealer knows the pattern: a customer drives off the lot with an in-house financed vehicle, makes their first few payments, then quietly drops their auto insurance to free up cash. Weeks later, that vehicle gets totaled. No insurance. No payout. Just a charge-off sitting on your books.

This is exactly the problem Collateral Protection Insurance (CPI) exists to solve. As a force-placed insurance product, CPI activates when a borrower fails to maintain the required coverage — protecting the dealer's financial interest in the vehicle without relying on the customer to do the right thing.

For BHPH dealers, where the dealership is the lender, an uninsured total loss hits directly on the balance sheet. Knowing what CPI covers, how it triggers, what it excludes, and how it fits a broader reinsurance strategy determines whether your portfolio stays profitable — or bleeds losses you could have prevented.

This article breaks down CPI from the basics through compliance requirements most dealers overlook — and explains how pairing CPI with a dealer-owned reinsurance structure can turn a risk management tool into a genuine profit center.

TL;DR

- CPI is force-placed on a customer's account when their required auto insurance lapses, protecting the dealer's interest in the vehicle collateral.

- It's enforced through the retail installment contract — not optional, not customer-selected.

- Coverage applies to physical damage and total loss of the collateral vehicle only — not liability, not GAP.

- An uninsured total loss without CPI means losing both the vehicle value and the remaining loan balance.

- Paired with a dealer-owned reinsurance company, CPI premiums flow back to the dealer as retained underwriting profit rather than a third-party cost.

What Is CPI and Why It Matters for BHPH Dealers

Collateral Protection Insurance is a force-placed insurance policy a dealer adds to a customer's loan account when that customer fails to maintain required full-coverage auto insurance — with the dealer listed as lienholder. The CFPB confirms it plainly: "This insurance protects only the lender, not you, but the lender will charge you for the insurance."

That single-interest structure is the point. CPI isn't a benefit the customer gets — it's the contractual remedy the dealer has when the borrower breaks their insurance obligation.

The BHPH Context Makes This Critical

In a traditional franchise deal, a bank or captive lender holds the lien. If the customer lets their insurance lapse, the bank absorbs the loss exposure. In a BHPH deal, the dealer holds the lien. There is no bank cushion. An uninsured total loss is a direct hit to your balance sheet.

CPI is not something customers select or opt into. The retail installment contract requires them to maintain qualifying coverage. CPI is what happens when they don't — it's enforcement, not an add-on product.

CPI is also not:

- GAP insurance, which covers the loan deficiency after a primary payout — CPI pays nothing toward that gap

- A service contract covering mechanical breakdown — CPI has no mechanical component

- The customer's liability policy — CPI protects your lien interest, not the customer's exposure to third-party claims

Why BHPH Portfolios Carry Higher Lapse Risk

BHPH borrowers are more likely to let insurance lapse than buyers in traditional finance channels. Industry data consistently shows that the majority of BHPH lending volume goes to subprime borrowers — compared to roughly a quarter for traditional lenders. Deep subprime borrowers (scores below 580) account for a disproportionate share of all BHPH loans.

These borrowers are managing tight budgets against 25%+ APRs. When something has to give, insurance is often the first expense cut.

The national uninsured motorist rate reached 15.4% in 2023 — up from 12.4% in 2017 — according to the Insurance Research Council. In Mississippi, the rate exceeds 28%. No authoritative source publishes a BHPH-specific lapse rate, but the demographic profile of BHPH borrowers makes it reasonable to assume lapse rates run meaningfully higher than the national baseline.

What CPI Covers — and What It Doesn't

CPI is a single-interest policy. It protects the dealer's financial interest in the collateral vehicle — nothing more.

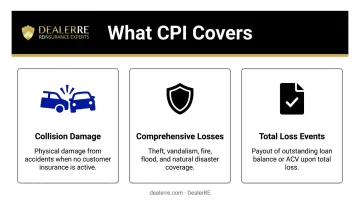

Coverage Inclusions

When CPI is active, it covers:

- Collision damage — physical damage from an accident while the vehicle has no qualifying customer insurance

- Comprehensive losses — theft, vandalism, fire, flood, and natural disaster

- Total loss events — when the vehicle is written off, CPI pays the outstanding loan balance or the vehicle's actual cash value (whichever applies per policy terms), preventing a complete charge-off

When damage is repairable, CPI can cover repair costs to restore the vehicle, keeping the loan account intact and the borrower in the car.

Coverage Exclusions and Boundaries

CPI also has firm boundaries — and they matter for how you structure each deal:

- No liability protection for the customer — if they cause an accident and injure someone, that's entirely on them

- No GAP coverage — if the loan balance exceeds the vehicle's ACV at total loss, the remaining deficiency is still owed by the borrower (and often uncollectable)

- No mechanical breakdown — service contract territory, not CPI

- No personal property inside the vehicle

The GAP deficiency issue is worth calling out specifically for BHPH dealers. On high loan-to-value deals — which BHPH often produces — a CPI payout at ACV may still leave a significant deficiency on the books.

Dealers running high-LTV portfolios should evaluate whether supplemental GAP coverage closes that remaining exposure. CPI and GAP serve different functions; in some deals, you need both.

How CPI Works in a BHPH Operation

CPI isn't just a policy — it's an ongoing operational process. Its effectiveness depends on consistent enrollment, accurate tracking, regulatory compliance, and integration with your collections workflow.

The Trigger and Enrollment Process

The standard workflow looks like this:

- At the point of sale, the customer provides proof of full-coverage insurance with the dealer listed as lienholder.

- Ongoing monitoring tracks that coverage — either through an automated tracking system, carrier notification, or staff follow-up.

- When coverage lapses or isn't provided, CPI is force-placed onto the account.

- The customer is notified per applicable state and contractual requirements.

State-specific rules govern how quickly CPI can be applied after a lapse is detected. Waiting periods vary across jurisdictions — some states permit near-immediate placement, others require a defined waiting window — and dealers must work with compliance guidance specific to their state to stay compliant.

Adding CPI Premiums to the Loan Account

Once force-placed, the dealer adds the CPI premium to the customer's loan balance and collects it at the next scheduled installment. It stays on the account until the customer reinstates qualifying coverage and provides acceptable proof.

Many customers never reinstate coverage. The CPI premium becomes a recurring line item. This makes tracking accuracy and collections integration critical — a poorly managed CPI process creates billing gaps, disputes, and unrecovered premiums.

Compliance and Customer Notification Requirements

Federal force-placed insurance rules under CFPB Regulation X apply to mortgage servicers, not auto dealers. Auto CPI compliance is governed by a patchwork of state insurance regulations, the NAIC Creditor-Placed Insurance Model Act, and the terms of the retail installment contract itself.

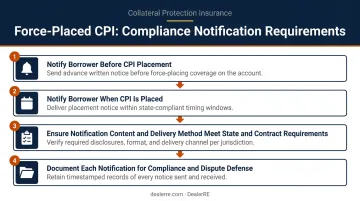

Regardless of state, dealers share common notification obligations:

- Notify the borrower before CPI is placed, per contractual requirements

- Notify the borrower when CPI is placed, with timing that meets state standards

- Ensure notification content and delivery method satisfy both state rules and the retail installment contract

- Document each notification for compliance and dispute defense

The CFPB's enforcement action against Fifth Third Bank for improper force-placed auto insurance practices is a useful reminder that regulators are paying attention in this space, even without a prescriptive federal auto CPI framework.

Work with a CPI provider that handles customer notifications on your behalf. Self-managing notifications — getting content, timing, and delivery right across every account — creates real legal exposure if anything slips.

The Risks of Operating Without CPI

Without CPI, every uninsured vehicle in your portfolio is an uncovered liability. If that vehicle gets totaled or stolen while the customer has no insurance, the full loss lands on you.

The charge-off math is brutal. An uninsured total loss typically means losing both the vehicle's value and the remaining loan balance — the customer who let their insurance lapse almost never has the financial capacity to pay off the deficiency. NIADA data puts the average BHPH default rate at 36%, with average loss severity per repossession exceeding $10,000 — up from roughly $7,500 pre-pandemic.

The dollar stakes have risen sharply:

- Average BHPH inventory cost: $13,117 (NIADA, 2023)

- Average reconditioning costs: $1,679 (NIADA, 2024)

- Wholesale used vehicle values remain elevated — the Manheim Used Vehicle Value Index hit 209.2 in April 2026

A single uninsured total loss on a higher-value unit can represent a $15,000–$20,000 write-off when you account for the vehicle cost, reconditioning, and lost loan receivable. For a small or mid-sized BHPH operation, that kind of hit lands directly on cash flow — not as an accounting abstraction, but as real money out the door.

BHPH delinquency rates reached 10% in Q3 2025, nearly three times the traditional lender average. Repossession rates are 16 times higher than the industry norm. Each of those repos carries uninsured-loss exposure. At that volume, going without CPI isn't lean — it's reckless.

CPI and Reinsurance: Turning Protection Into Profit

CPI protects your portfolio. Pair it with a dealer-owned reinsurance structure, and it also builds equity — premiums that once flowed to a third-party carrier start staying in your business instead.

How the Structure Works

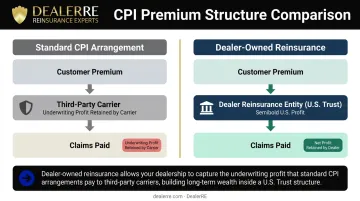

In a standard CPI arrangement, premiums flow to a third-party insurance carrier. The carrier pays claims, retains the underwriting profit, and the dealer gets protection. That's the baseline.

In a dealer-owned reinsurance structure, the dealer establishes their own reinsurance company — typically domiciled offshore in a jurisdiction like the Turks and Caicos Islands, while all assets remain in a U.S. trust account. CPI premiums flow into the dealer's reinsurance entity rather than to a third-party carrier. Claims are paid from that pooled fund. Net underwriting profits stay with the dealer.

DealerRE helps BHPH dealers set up admin obligor reinsurance programs that include CPI. The structure uses a Trust Agreement between the direct underwriting insurance company, the dealer's reinsurance entity, and a U.S.-based Trust Company — meaning no funds go offshore. Withdrawals from the trust cover claim payments, limited professional fees, income taxes, and any funds above required reserves, all requiring approval from the underwriting insurance company.

The Tax Angle

Property and casualty insurance companies with less than $2.2 million in annual net premiums can elect to be taxed only on investment income under IRS Section 831(b) — a real tax advantage for mid-sized dealers accumulating CPI premium volume. The reinsurance company elects to be treated as a domestic insurance company for U.S. federal tax purposes despite its offshore domicile.

Dealers should work with qualified tax counsel on this structure. IRS Notice 2016-66 flagged certain micro-captive transactions for enhanced scrutiny, so proper setup and documentation matter.

When Does Reinsurance Make Sense?

The tax efficiency above assumes meaningful premium volume — which is exactly why reinsurance isn't the right starting point for every dealer. Smaller or earlier-stage BHPH dealers can implement CPI effectively through a third-party provider and still capture the core protection benefit.

As premium volume grows, the economics shift. The underwriting profit leaving your business each month starts to represent real money — and at that scale, establishing a reinsurance company makes sense.

With DealerRE's guidance on structure, administration, and compliance, retained CPI premiums can be invested, used to fund capital needs, or withdrawn to support dealer and personal financial goals.

Common Misconceptions About CPI Among BHPH Dealers

Myth: "CPI Is Only for Large Dealerships"

This is the most common objection — and it's wrong. Smaller BHPH dealers arguably need CPI more than large operations because they have less financial cushion to absorb an uninsured total loss. CPI programs are scalable; the capital required to implement is minimal relative to the exposure it covers. DealerRE has seen this firsthand across its dealer base — volume isn't the barrier most dealers assume it to be.

Myth: "We Track Insurance Manually, So We're Covered"

Staff follow-up alone creates serious gaps. Customers can provide expired or fraudulent proof of insurance, let policies lapse between check-ins, or simply stop responding. An automated tracking system or carrier notification service catches lapses as they happen. Manual processes don't — and a lapse that goes undetected for several weeks is a wide window for an uninsured loss.

Myth: "CPI and GAP Are Basically the Same Thing"

They're not interchangeable — they address different pieces of the same problem:

- CPI protects the vehicle collateral against physical damage and total loss

- GAP covers the loan deficiency remaining after a payout when the vehicle's ACV falls short of the outstanding balance

On a high-LTV BHPH deal, a CPI payout settles the vehicle loss but may leave a significant deficiency uncovered. That remaining balance is exactly what GAP is designed to address. For many BHPH deals, having both in place is the only way to fully protect against a total loss scenario.

Frequently Asked Questions

What does CPI insurance cover?

CPI covers physical damage and total loss of the collateral vehicle, paying the dealer's outstanding loan balance or the vehicle's actual cash value per policy terms. As a single-interest policy, it protects only the dealer's financial interest — not the customer's liability exposure or mechanical issues.

How does CPI differ from regular auto insurance?

Regular auto insurance is purchased by and primarily benefits the vehicle owner. CPI is force-placed by the dealer/lender when the customer fails to maintain their own required coverage — it protects the lender's interest in the collateral, not the customer's personal liability or equity.

Who pays for CPI — the dealer or the customer?

The dealer arranges and initially pays the CPI premium, then passes the cost to the customer by adding it to their loan balance, collected per the retail installment contract schedule.

Is CPI required for BHPH customers?

CPI is not required by law, but it is enforced by the dealer under the retail installment contract. Customers agree at signing to maintain qualifying insurance. CPI is the contractual remedy when they fail to meet that obligation.

When is CPI added to a BHPH loan account?

CPI is triggered when a customer's insurance lapses or proof of coverage isn't provided. State laws dictate the allowable waiting period before placement, and dealers must follow their jurisdiction's specific compliance requirements to avoid legal exposure.

Can a BHPH dealer use CPI without setting up a reinsurance company?

Yes. Dealers can partner with a CPI provider, force-place coverage when needed, and receive basic protection without any reinsurance structure. Reinsurance becomes relevant when premium volume grows to the point where retaining underwriting profit, rather than sending it to a third-party carrier, represents a meaningful financial opportunity.