Introduction

Many BHPH dealers implement collateral protection insurance (CPI) programs to protect their financed inventory when customers let their coverage lapse — but most launch these programs without fully understanding what they actually cost or what they can earn back. This lack of clarity creates two common problems: dealers who underestimate total program costs and price coverage incorrectly to customers, and dealers who don't realize they can recapture substantial underwriting profits through a dealer-owned reinsurance arrangement.

CPI program costs for BHPH dealers are not one-size-fits-all. Pricing depends on variables including the ceding fee percentage, program structure, active portfolio size, state-specific premium taxes, and whether the dealer participates in underwriting profits through a reinsurance company.

Understanding how these components interact is what separates dealers who run a profitable CPI program from those who leave money on the table.

This article breaks down the real cost components of a CPI program — from ceding fees and per-vehicle charges to setup expenses and ongoing administration. It also covers the difference between standard third-party programs and dealer-owned reinsurance structures, so you can evaluate your options and determine which approach fits your portfolio size and business goals.

Key Takeaways

- CPI programs cost dealers through a ceding fee of 8%–20% of collected premiums plus state insurance premium tax

- Monthly customer premiums typically range $80–$120 per vehicle based on value and coverage terms

- Standard programs are pure cost centers — dealer-owned reinsurance structures return a substantial share of premiums back as underwriting profit

- The cheapest ceding fee isn't always the most cost-effective when compliance, claims quality, and monitoring are factored in

- Uninsured driver rates reached 15.4% nationally in 2023, leaving roughly 1 in 7 financed vehicles uninsured at any given time

What Does a CPI Program Cost for BHPH Dealers?

CPI program costs don't come as a flat purchase price — they're structured as a percentage of premiums collected from enrolled customers. This means costs scale directly with your portfolio size and penetration rate (the percentage of your active accounts enrolled in CPI coverage at any given time).

Two cost scenarios create the most problems for BHPH dealers: those who underestimate total program cost and price it poorly to customers, absorbing losses they shouldn't, and those who don't realize they can recapture underwriting profits through a reinsurance structure and leave substantial money with their third-party provider unnecessarily.

Ceding Fee: The Primary Cost Driver

The ceding fee is the percentage of collected premiums the dealer pays to the CPI program provider or fronting insurance carrier. Cost comparisons between providers hinge on this number — and it's where the range is widest.

Auto Remarketing's 2022 coverage of the CPI market shows traditional providers typically charge ceding fees between 12% and 20%. Auto Finance News confirmed this in 2024, reporting a standard range of 15%-20% among established carriers.

However, competitive pressure has driven some providers to introduce lower rates. National Lenders disrupted the market in 2022 by launching a program with an 8% ceding fee — described as "industry-leading" — establishing a new competitive floor. Dealers should evaluate proposals against a range of 8%-20%: 8% represents the low end from specific market entrants, while 15%-20% is the more typical range from established providers.

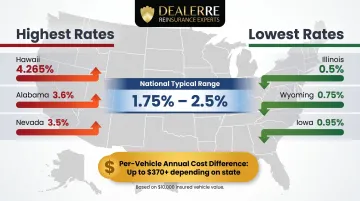

State insurance premium tax is added on top of the ceding fee and represents a real but frequently overlooked cost component. Premium tax rates vary by state and are non-negotiable pass-through costs. According to NAIC premium tax data, most states charge 1.75%-2.5%, though outliers exist:

- Highest rates: Hawaii (4.265%), Alabama (3.6%), Nevada (3.5%)

- Lowest rates: Illinois (0.5%), Wyoming (0.75%), Iowa (0.95%)

For a dealer collecting $100/month CPI premium per vehicle, the premium tax alone adds $4.27 in Hawaii versus $0.50 in Illinois — a difference that compounds across a 200-vehicle portfolio.

Per-Vehicle Monthly Cost to Customers

The monthly CPI premium is the cost passed to customers when they fail to maintain their own insurance. This amount reimburses the dealer for the cost of force-placed coverage and is typically added to the principal balance or monthly payment schedule.

Auto Finance News reports that BHPH customers pay $80-$120 per month for CPI coverage, compared to approximately $191/month (the 2024 national average) for traditional full-coverage auto insurance. That puts CPI at a 42%-63% discount relative to standard coverage, with one key caveat: CPI covers only the dealer's collateral interest (single-interest physical damage), while full-coverage insurance also includes liability and other protections.

Penetration rate — the percentage of your active portfolio enrolled in CPI at any given time — directly affects total program revenue and cost recovery. According to RL Dealer Services, new programs typically reach 25%-30% penetration within the first 90-120 days, with 40%-50% achievable at program maturity.

For a dealer with 200 active accounts, that difference is significant:

| Penetration Stage | Enrolled Vehicles | Monthly Premium Range |

|---|---|---|

| Early (30%) | 60 vehicles | $4,800–$7,200 |

| Mature (50%) | 100 vehicles | $8,000–$12,000 |

Program Setup and Administration Costs

Some CPI providers charge upfront or ongoing administrative fees for compliance forms, customer notifications, insurance verification monitoring, and claims handling. Others bundle these services into the ceding fee. This creates a hidden cost differential that doesn't show up in simple ceding fee comparisons.

Dealers should confirm exactly what is included versus billed separately:

- Legal formation and compliance documents (state-specific notices, consumer disclosures)

- Insurance verification and lapse monitoring (automated tracking systems or manual staff processes)

- Claims adjudication services (processing, payment turnaround, dispute resolution)

- Ongoing regulatory filings (annual renewals, state reporting)

The cost of getting compliance wrong is steep: regulatory fines, consumer complaints, and CFPB enforcement actions can quickly dwarf the cost of doing it right upfront. CFPB enforcement actions against lenders for improper force-placed insurance demonstrate real financial consequences, including restitution orders exceeding $1 million in documented cases.

Key Factors That Affect CPI Program Costs

Several variables determine how much a BHPH dealer pays for — or earns back from — a CPI program. Knowing these factors lets dealers evaluate providers on equal footing, not just by the advertised ceding fee.

Portfolio Size and Penetration Rate

A dealer with a large active loan portfolio generates more CPI premium volume, which affects both total program cost and the economics of a reinsurance arrangement. A small dealer with 50 active accounts operates with very different economics than one with 500.

Example: Consider two dealers at 30% penetration collecting $100/month per enrolled vehicle:

- Dealer A (50 active accounts): 15 vehicles enrolled = $1,500/month premium = $18,000/year

- Dealer B (500 active accounts): 150 vehicles enrolled = $15,000/month premium = $180,000/year

At a 15% ceding fee, Dealer A pays $2,700/year while Dealer B pays $27,000. This difference explains why reinsurance structures — which require setup costs and ongoing management — become more cost-effective at larger portfolio sizes. Auto Finance News notes that 50-100 active accounts or approximately $500,000+ in managed assets typically represents the minimum portfolio size where a formal dealer-owned reinsurance structure becomes cost-justified.

State Regulatory Environment

CPI regulation varies widely by state, and that variance directly affects compliance costs and program pricing. According to RL Dealer Services, the regulatory landscape breaks down roughly as follows:

- ~3 states regulate CPI through insurance codes

- ~8 states regulate it through finance codes

- Remaining states have no CPI-specific regulation

Dealers operating across multiple states must design their program around the most restrictive jurisdiction's requirements. Even in unregulated states, the NAIC Creditor-Placed Insurance Model Act #375 sets baseline standards — including a 20-day initial notice plus 10-day final notice before force-placement, and justification required for commissions exceeding 20% of net written premium.

Coverage Scope and Vehicle Values

CPI covers the dealer's interest in the collateral (physical damage/total loss), not the customer's liability. Premium tracks the value of vehicles being covered — higher-value inventory commands higher premiums.

CPI typically covers:

- Physical damage (comprehensive and collision)

- Total loss (limited to actual cash value or net payoff, whichever is less)

- Dealer's financial interest only

It's equally important to understand what CPI does NOT cover:

- Customer liability (third-party bodily injury or property damage)

- Medical payments or personal injury protection

- Customer's personal property inside the vehicle

- State minimum liability requirements

Customers enrolled in CPI must continue carrying their own liability insurance as required by state law. CPI is not a substitute for that legal obligation.

Profit Participation Structure

How a dealer participates economically in the program changes the cost picture entirely. There are three main structures:

- No profit participation — Dealer pays ceding fee; insurance company keeps all underwriting profit

- Standard retrospective commission — Dealer receives a retro commission tied to favorable loss experience

- Dealer-owned reinsurance company (PORC/admin obligor) — Dealer's reinsurance entity receives underwriting profit directly

Structure #3 shifts the dealer from a fee-payer to a profit-center owner. According to RL Dealer Services, approximately $67 per month per enrolled vehicle flows into the dealer's reinsurance company in a PORC structure. Auto Finance News reports dealers capture $25-$45 per month net per vehicle in underwriting profit and reserves under this model, with programs modeled on a 40%-60% loss ratio.

The gap between the $67 gross and $25-$45 net represents claims payments and the reduced ceding fee to the fronting carrier.

CPI Cost Breakdown: What You're Actually Paying For

The total cost of a CPI program extends well beyond the ceding fee. BHPH dealers should evaluate all cost components — one-time and recurring — before selecting a program.

Here's what you're actually paying for across five cost components:

Ceding Fee (Recurring)

The ceding fee is paid as a percentage of collected premiums and is the largest recurring cost in any CPI program. Typical rates run 8%–20%, depending on the provider and program structure.

In a reinsurance arrangement, dealers retain the majority of premium and cede only a smaller portion to the fronting carrier — which significantly changes the cost structure compared to a standard third-party program. That distinction alone is worth understanding before you compare quotes.

State Insurance Premium Tax (Recurring)

Every licensed state applies a premium tax as a pass-through cost separate from the ceding fee. In most states, this runs 1.75%–2.5%, with outliers ranging from 0.5% to 4.265%.

This rate is non-negotiable. At typical premium levels, it adds roughly $18–$30 per vehicle per year and should be factored into any cost estimate from day one.

Compliance, Forms, and Legal Setup (One-Time / Periodic)

This covers consumer-compliant disclosure forms, state-specific notices, and — when a reinsurance entity is involved — legal formation documents and regulatory filings. Some providers bundle this end-to-end into the ceding fee; others charge separately or leave it to the dealer.

The cost of getting this wrong is steep. CFPB enforcement actions against Fifth Third Bank and Lobel Financial show that improper notice sequencing, duplicative placements, and refund handling errors can produce restitution orders exceeding $1 million. Front-end compliance spend is far cheaper.

Insurance Verification and Monitoring (Recurring)

Dealers must confirm that customers claiming coverage actually have it — and catch lapses as they happen. Some CPI providers include automated verification and monitoring tools; others charge separately or expect dealership staff to handle it manually.

The difference in outcomes is significant. Auto Finance News reports that lenders using automated tracking systems achieve 80%–90% successful CPI placement on identified lapses. Manual processes introduce labor cost and reduce that placement rate.

Claims Adjudication (Recurring / Per-Claim)

When a covered vehicle is damaged or totaled, the claim must be processed and paid. Providers vary widely here — some offer fast, dealer-friendly adjudication; others create delays that translate to real money in downtime and lost customer goodwill.

Claims quality rarely appears in an initial ceding fee comparison, but it shows up on your bottom line. A provider with a 10% lower ceding fee but 30-day slower claims processing may actually cost more in lost opportunity and customer satisfaction.

Standard CPI vs. CPI With a Dealer-Owned Reinsurance Company

The fundamental difference between these two structures determines whether CPI functions as a cost center or a profit center for your dealership.

Standard Third-Party CPI Program:

- Dealer pays ceding fee to insurance company

- Insurance company keeps all underwriting profit

- Dealer has no participation in favorable loss experience

- Lower setup complexity and infrastructure requirements

- Better suited for smaller portfolios (under 50-100 active accounts)

Dealer-Owned Reinsurance Structure (PORC/Admin Obligor):

- Portion of premium flows into dealer's own reinsurance entity

- Dealer participates in underwriting profit when claims are low

- Approximately $67/month per enrolled vehicle flows into the dealer's reinsurance company (gross)

- Net profit of $25-$45/month per vehicle after claims and fronting carrier fees

- Requires setup, ongoing management, compliance, and minimum portfolio size

- Better economics for established dealers with 50-100+ active accounts

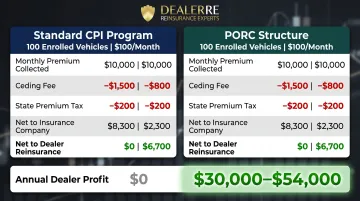

Example Premium Flow Comparison (100 enrolled vehicles at $100/month premium):

| Component | Standard Program | PORC Structure |

|---|---|---|

| Monthly premium collected | $10,000 | $10,000 |

| Ceding fee (15% vs 8%) | -$1,500 | -$800 |

| State premium tax (2%) | -$200 | -$200 |

| Net to insurance company | $8,300 | $2,300 |

| Net to dealer's reinsurance | $0 | $6,700 |

| Dealer profit participation | $0/year | $30,000-$54,000/year (at 40%-60% loss ratio) |

The table above makes the choice straightforward — the question is whether your portfolio is large enough to justify the setup.

Which structure fits your dealership?

- Under 50 active accounts: start with a standard program to keep setup simple and costs low

- 50-100+ active accounts (or $500,000+ in managed assets): a reinsurance structure generates enough premium volume to cover setup costs and produce meaningful profit participation

- Already at scale: DealerRE helps BHPH dealers set up and manage admin obligor programs that replace third-party CPI providers and keep underwriting profits in-house

What BHPH Dealers Most Often Get Wrong About CPI Costs

Focusing Only on the Ceding Fee

A lower ceding fee from a provider that doesn't handle compliance, monitoring, or claims properly can cost more in staff time, legal exposure, and claim disputes than a slightly higher fee from a full-service provider.

What to evaluate instead:

- What's included in the ceding fee (compliance forms, monitoring tools, claims handling)?

- What's the provider's claims turnaround time and dispute rate?

- Does the provider offer automated insurance verification or does your staff handle it manually?

- What compliance support is provided for state-specific regulations?

A provider charging 12% with full-service compliance and 5-day claims turnaround may deliver better net economics than one charging 8% but requiring your staff to manage notices, tracking, and claims disputes.

Ignoring the Cost of Not Having CPI

An uninsured total loss on a financed vehicle with no CPI coverage means the dealer absorbs the entire loss — typically the full remaining principal balance minus any salvage value.

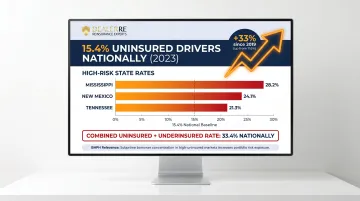

According to Insurance Research Council data from 2023, 15.4% of U.S. drivers were uninsured — up from 11.6% in 2019, a 33% increase in just four years. The combined uninsured and underinsured rate reached 33.4% nationally, meaning one in three drivers lacks adequate coverage.

The BHPH demographic — subprime borrowers with lower incomes and past financial challenges — consistently shows higher uninsured rates than the national average. Dealers operating in high-uninsured states face an even sharper concentration of that risk:

- Mississippi: 28.2% uninsured rate

- New Mexico: 24.1% uninsured rate

- Tennessee: 21.3% uninsured rate

Without CPI, that exposure lands directly on the portfolio.

Treating CPI Purely as a Cost

Absorbing uninsured losses is the floor-level risk CPI addresses — but dealers who understand penetration rates, premium volume, and reinsurance structures can model CPI as a profit center, not just portfolio protection.

Many dealers implement CPI without considering profit participation options and leave significant money with their third-party provider on the table. At 40% penetration on a 200-vehicle portfolio collecting $100/month per enrolled vehicle, a PORC structure puts $24,000–$43,200 in annual profit back in the dealer's pocket instead of the insurance company's.

Frequently Asked Questions

How much does collateral protection insurance cost?

For BHPH dealers, CPI cost is primarily measured as a ceding fee — typically 8%-20% of collected premiums depending on the provider — plus state premium tax (usually 1.75%-2.5%). The monthly cost passed to customers ranges $80-$120 based on vehicle value and coverage terms, which is generally less than what customers would pay for standard full-coverage auto insurance.

What is collateral protection insurance?

CPI is a lender-placed insurance product that protects the BHPH dealer's financial interest in a financed vehicle when the customer fails to maintain adequate auto insurance. It is a single-interest policy: the dealer (lienholder) is the insured, not the customer. The cost is typically recouped by adding a monthly charge to the customer's account when their insurance lapses.

Can you drive with CPI insurance?

CPI does not cover the customer's liability or personal protection while driving — it only protects the dealer's collateral interest. Customers enrolled in CPI remain legally responsible for carrying their own liability coverage as required by their state. CPI is not a substitute for comprehensive auto insurance.

What is a ceding fee in a CPI program?

A ceding fee is the percentage of CPI premiums that the dealer pays to the program provider or insurance carrier in exchange for risk coverage and program administration. It is the primary recurring cost of a CPI program and varies significantly between providers (8%-20%), so it warrants close comparison when evaluating options.

Can a BHPH dealer make money from a CPI program?

Yes. Dealers who structure their CPI program through a dealer-owned reinsurance company (PORC or admin obligor entity) can capture underwriting profits instead of paying them to a third-party carrier. The structure typically nets $25-$45 per enrolled vehicle per month and makes the most financial sense for dealers with 50-100+ active accounts.

Is CPI required for BHPH dealers?

CPI is not legally mandated in most states, but it functions as a financial necessity for BHPH dealers. With 15.4% of U.S. drivers uninsured — and BHPH customers skewing higher — dealers without CPI absorb the full cost of any uninsured damage or total loss on their financed inventory.