Introduction

F&I has become the load-bearing wall of dealership profitability. As front-end new vehicle gross profit per vehicle retailed dropped 14.4% year-over-year in Q1 2025, F&I PVR climbed to $2,515 — and the dealers capturing the most from that trend aren't just selling more products. They own the underwriting profits behind them.

Reinsurance remains one of the most powerful wealth-building strategies available to auto dealers, yet most are still selecting programs based on a single number: the admin fee. That's a costly habit heading into 2026.

With 25% tariffs on imported vehicles and parts now in effect, average new vehicle prices projected to rise from $48,000 toward $54,000, and front-end margins continuing to compress, the structure and partner behind your reinsurance program carry more weight than ever. A program that looks cheap on the surface can drain the profits it was supposed to protect.

This guide breaks down the four primary reinsurance structures available in 2026, what sets them apart, and how to evaluate your options beyond the admin fee.

TL;DR

- Four primary structures exist in 2026: CFC, Super CFC, DOWC, and Admin Obligor — each with distinct tax treatment, profit capture, and compliance requirements

- The right fit depends on dealership volume, growth trajectory, and how much operational infrastructure the dealer can support

- Total cost goes well beyond the admin fee — ceding fees, claims adjudication fees, and premium taxes all affect net profitability

- Admin Obligor programs let dealers own their reinsurance entity outright, backed by A-rated carriers, without taking on heavy compliance overhead

- Program administration quality — claims handling, compliance filings, reporting — directly determines how much profit the dealer actually keeps

What Is a Dealer Reinsurance Program — and Why It Matters in 2026

In plain terms, dealer reinsurance replaces third-party F&I product administrators with the dealer's own reinsurance company. Instead of paying a VSC administrator or GAP provider to absorb underwriting profits on contracts your dealership sold, that income flows into a company you own.

Every time a third-party vendor processes a claim, they're using profit margin that came from your customers and your F&I office. The question isn't whether that profit exists — it's whether it goes to them or to you.

Why 2026 Changes the Calculus

A 25% tariff on imported vehicles took effect April 3, 2025, with a matching tariff on imported parts following in May. Parts account for roughly 50% of claim costs, and approximately half of those parts are imported — meaning VSC claim costs are projected to rise 3% to 6%.

At the same time, higher vehicle prices are pushing stronger demand for service contracts and GAP coverage, as buyers look to protect a costlier investment. Two forces are moving at once: claim costs rising, F&I product volume growing.

Where that profit lands — inside your reinsurance company or inside a third-party administrator — depends entirely on how your program is structured. The four structures below differ meaningfully on profit capture, tax treatment, and operational complexity.

Top Dealer Reinsurance Program Types for 2026

Program types below were evaluated across five dimensions: profit capture potential, tax efficiency, level of control, scalability, and suitability for different dealer profiles — from BHPH and independent used-car lots to franchise stores and multi-rooftop groups.

CFC (Controlled Foreign Corporation)

The CFC is the most established dealer reinsurance structure. It operates as an offshore corporation that reinsures F&I contracts issued by a licensed obligor, making it a common starting point for small-to-mid-size dealerships seeking tax efficiency without significant compliance overhead.

The primary advantage is the §831(b) election, which excludes underwriting profits from taxable income up to the annual premium cap — set at $2,900,000 for 2026 per the IRS-confirmed annual indexed adjustment. Only investment income is taxed annually.

The limitation: CFCs use net accounting, meaning only the wholesale portion of the premium — after admin fees and commissions — flows into the captive. For higher-volume stores, that cap becomes a ceiling on growth.

| Factor | CFC Details |

|---|---|

| Ideal Dealer Profile | Small-to-mid-size stores with moderate F&I volume |

| Tax Treatment | §831(b) excludes underwriting profit up to annual cap; investment income taxed annually |

| Premium Capture | Net accounting — wholesale portion only after admin fees/commissions |

| Setup Complexity | Lower — obligor handles licensing, compliance, claims support |

| Control Level | Moderate — dealer owns the company; obligor manages operations |

Super CFC

The Super CFC was developed specifically to remove the annual premium cap that limits traditional CFCs. It remains offshore and still reinsures through a licensed obligor, but uses retail accounting — booking the full contract price as written premium rather than just the wholesale net.

That distinction matters at scale. By recording full retail premium and creating large unearned premium reserves, the Super CFC generates net operating losses (NOLs) in early years that carry forward to defer tax exposure. There's no annual ceiling, so volume isn't restricted. Dealers can also typically borrow against unearned premium reserves for earlier access to capital — a meaningful advantage for growing groups managing cash flow across multiple stores.

| Factor | Super CFC Details |

|---|---|

| Ideal Dealer Profile | Mid-to-large volume dealers who've outgrown the CFC cap |

| Tax Treatment | Tax deferral via NOL carryforwards; no annual premium ceiling |

| Premium Capture | Retail accounting — full contract price booked as written premium |

| Setup Complexity | Moderate — more complex accounting; still relies on licensed obligor |

| Control Level | Moderate-to-high — more investment flexibility and capital access |

DOWC (Dealer-Owned Warranty Company)

A DOWC places the dealer's own entity in the obligor role, meaning the dealer's company issues the contracts directly and bears full legal responsibility for claims. That's the maximum-control position in dealer reinsurance, and it comes with corresponding requirements.

DOWCs use retail accounting and capture 100% of underwriting and investment income. The trade-off is regulatory complexity: state-by-state licensing or surety bonds, solvency maintenance, higher startup capitalization, and ongoing compliance management.

The NAIC Service Contracts Model Act establishes financial security requirements including funded reserve accounts of at least 40% of gross consideration received (less claims paid), plus a minimum deposit of 5% of gross consideration with the state commissioner. That infrastructure demand makes DOWCs best suited for large dealer groups with dedicated compliance and financial management staff.

| Factor | DOWC Details |

|---|---|

| Ideal Dealer Profile | Large groups/multi-rooftop operations with in-house compliance resources |

| Tax Treatment | Retail accounting with NOL deferral; treated as domestic corporation |

| Premium Capture | 100% retail premium — dealer is the obligor with no third-party split |

| Setup Complexity | High — state licensing, solvency requirements, higher capitalization |

| Control Level | Maximum — full control over product design, claims, reserves, investments |

Admin Obligor Reinsurance

The Admin Obligor structure gives dealers ownership of their own reinsurance company while the program is backed by A-rated insurance carriers. The obligor — a licensed administrator — handles state compliance and claims, but the dealer's reinsurance entity captures the underwriting profits and investment income from their own F&I book.

The practical result: dealers stop paying third-party administrators to keep profits that originated from their own customer transactions, without absorbing the full regulatory infrastructure of a DOWC. It sits between a CFC and a DOWC on the complexity spectrum — closer to DOWC-level profit capture with CFC-level setup demands.

It's particularly well-suited for independent dealers, used-car lots, and BHPH operators. In the BHPH space specifically, the admin obligor model can be designed to cover mechanical breakdown and insurance losses funded by the dealer's existing customer base — CPI, DCC, GAP, and VSCs all fold into the structure, converting what were previously third-party expenses into captured underwriting profit.

DealerRE has specialized in this model since 1994 and has helped over 400 dealers nationwide establish and manage admin obligor reinsurance companies. Full-service administration covers training, claims adjudication, compliance, performance reporting, and bookkeeping, so dealers stay focused on operations rather than running an insurance company.

| Factor | Admin Obligor Details |

|---|---|

| Ideal Dealer Profile | Independent dealers, franchise stores, used-car lots, BHPH operators |

| Tax Treatment | Underwriting profits accumulate within dealer-owned company; investment income reinvestable into real estate, equipment, or dealership operations |

| Premium Capture | Net-to-retail hybrid depending on program design; dealer replaces third-party F&I products and retains profits |

| Setup Complexity | Low-to-moderate — A-rated obligor handles compliance; full-service partner manages filings, taxes, renewals |

| Control Level | High — dealer owns the company; partner manages administration |

How to Evaluate Dealer Reinsurance Programs Beyond the Admin Fee

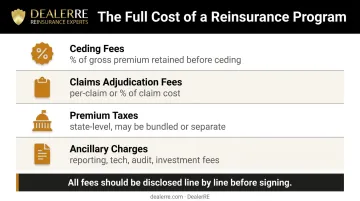

Admin fee comparisons are how dealers get conditioned to overlook the costs that actually determine net profitability. The admin fee is one number on one line. The real cost structure has several more.

The Full Cost Picture

When evaluating any reinsurance program, these are the charges that determine what actually ends up in your company:

- Ceding fees — a percentage of gross premium retained by the administrator before funds are ceded to your company; scales with volume and can erode profitability more than a fixed admin fee

- Claims adjudication fees — charged per claim or as a percentage of total claim cost; often blended into the "claims paid" line, making it difficult to distinguish from actual repair costs

- Premium taxes — mandatory state-level charges; may be bundled into the admin fee or billed separately depending on the program

- Ancillary charges — reporting fees, technology costs, audit expenses, investment management fees; rarely prominent but consistently present

Every cost above should be disclosed upfront — line by line, before you sign. DealerRE operates on a no-hidden-fees basis and holds that as the standard. Most programs don't.

What Else Matters When Comparing Programs

Cost structure is only part of the evaluation. These factors determine whether a program actually performs over time:

- Reporting transparency — quarterly statements should include clear benchmarks: loss ratios, reserve adequacy, claims trends, and investment performance. Programs that obscure these details make it impossible to track whether your program is on track or slipping.

- Scalability — the right structure today may not fit your business in three years. Programs should accommodate growth, including transitions that don't disrupt existing contracts or cash flow.

- Partner support quality — full-service administration covers F&I training, claims adjudication, compliance management, staff onboarding, and financial bookkeeping. A well-supported program and a neglected one produce measurably different loss ratios and underwriting profit over time.

- Product mix and loss ratio stability — vehicle service contracts, appearance protection, and tire-and-wheel coverage tend to produce more predictable loss ratios than volatile ancillary products. The right partner helps identify the mix that maximizes underwriting profit without adding unnecessary risk.

Conclusion

No single reinsurance structure is the right answer for every dealer. The CFC works well for moderate-volume stores prioritizing tax efficiency within the §831(b) cap. The Super CFC removes that ceiling for growing groups that need scalability and earlier capital access. The DOWC delivers maximum control for large operations with the infrastructure to support it. And the Admin Obligor model offers a strong balance — meaningful profit capture, A-rated carrier backing, and full-service administrative support for dealers who want a trusted partner managing the complexity.

What matters equally is the partner behind the program. Transparent cost disclosure, quality reporting, ongoing support, and a track record of helping dealers build profitable long-term programs aren't features to look for after you've signed. Evaluate them before committing to any structure.

Dealers ready to explore their options, or reassess an existing program, can connect with DealerRE for a no-obligation program analysis. Trusted since 1994 and serving over 400 dealers nationwide, DealerRE has spent decades helping dealers of all profiles establish and manage admin obligor reinsurance companies that turn F&I products into long-term F&I profitability.

Reach the team at (804) 824-9533.

Frequently Asked Questions

What type of reinsurance company offers diversity and capacity not found in other reinsurers?

Captive and admin obligor reinsurance structures backed by A-rated carriers offer greater flexibility in product design, investment options, and profit capture than standard third-party arrangements. They combine the dealer's direct ownership of underwriting profits with the financial capacity and regulatory backing of established insurance carriers. Neither a pure captive nor a standard third-party provider delivers both.

What is the difference between a CFC and a DOWC for auto dealers?

A CFC is an offshore entity that reinsures through a licensed obligor, limiting compliance burden but capping scale through net accounting. A DOWC makes the dealer the obligor, capturing 100% of retail premium but requiring state licensing, solvency compliance, and higher capitalization.

What does an admin obligor reinsurance program mean for auto dealers?

In an admin obligor program, the dealer owns the reinsurance company while a licensed obligor backed by A-rated carriers handles state compliance and claims processing. The dealer captures underwriting profits and investment income from their own F&I book without taking on the full regulatory infrastructure required by a DOWC.

How do dealer reinsurance programs help with tax planning?

Depending on structure, underwriting profits can grow tax-deferred via NOL carryforwards (Super CFC and DOWC) or be excluded from taxable income up to the §831(b) annual cap (CFC). Accumulated profits can also be reinvested into real estate, equipment, or dealership assets. Consult a CPA experienced with dealer reinsurance before structuring.

Which reinsurance structure is best for BHPH dealers?

BHPH dealers typically benefit most from an admin obligor structure designed to cover mechanical breakdown and insurance losses funded by the customer base. CPI, DCC, GAP, and VSCs all integrate into the program, converting third-party costs into captured underwriting profit.

What should dealers look for when choosing a reinsurance partner in 2026?

Prioritize transparent cost disclosure (ceding fees, adjudication fees, premium taxes), full-service administrative support (training, compliance, bookkeeping), and regular readable performance reporting. A partner with a proven track record — not just a low admin fee — is what separates a program that compounds wealth from one that underdelivers over time.