The stakes are substantial. Choosing the wrong reinsurance partner or structure can mean years of eroded underwriting profits, hidden fees draining reserves, and loss of control over the customer experience. Choosing well creates a genuine fifth profit center — one that compounds value as your dealership grows. With F&I gross profit per vehicle reaching $2,612 in Q4 2025, dealers who don't participate in reinsurance or who participate poorly are leaving significant money on the table.

This guide walks you through exactly how to evaluate any reinsurance proposal before you sign, using criteria that connect today's proposal details to tomorrow's financial outcomes.

Key Takeaways

- The full fee stack — not just the admin fee — determines real program cost; compare everything

- Reserve control, investment authority, and claims oversight define whether you actually own your program

- Monthly reporting by product category is a baseline expectation, not a premium feature

- Vet underwriting, compliance support, and exit terms before signing anything

- Red flags: bundled fees without line-item disclosure, resistance to transparency, and lock-in clauses

What a Dealer Reinsurance Program Proposal Should Contain

A legitimate reinsurance proposal clearly lays out program structure, complete cost architecture, eligible products, and administrative responsibilities. Anything missing from these categories signals a problem.

Program Structure Documentation

The proposal should specify which structure you'll operate under — Controlled Foreign Corporation (CFC), Non-Controlled Foreign Corporation (NCFC), or Dealer-Owned Warranty Company (DOWC)/admin obligor. Each has distinct implications for dealer control, tax treatment, investment flexibility, and capital access. A proposal that doesn't specify structure or glosses over the differences deserves more scrutiny.

Premium Flow Transparency

You need to see how dealer F&I product premiums move from the dealership into the reinsurance entity, what gets deducted along the way, and what ultimately lands in your reserves. This flow should be documented with line-item specificity — not summarized in vague totals.

If the proposal shows only a single premium number and a single reserve balance without explaining the path between them, critical information is being withheld.

Ongoing Provider Obligations

Reinsurance is a business that requires active, ongoing management — not a product you purchase and set aside. The proposal should outline:

- Reporting cadence (monthly, at minimum)

- Claims adjudication process and timelines

- Compliance management scope (domicile filings, tax returns, premium tax remittance)

- F&I training support and penetration coaching

- Performance review frequency and format

If these operational details aren't addressed in the proposal, they likely won't be addressed after you sign either.

6 Criteria to Evaluate Any Dealer Reinsurance Proposal

Most dealers compare proposals on admin fee alone — a single number that rarely tells the full story. These six criteria give dealers a structured way to connect proposal details to long-term financial outcomes.

Fee Structure Transparency

The admin fee is just the starting point. A thorough evaluation must account for the entire fee stack:

- Ceding fees: The portion of premium retained before funds reach your reinsurance entity

- Claims adjudication fees: Often a percentage of each net claim paid

- Premium taxes: Vary by domicile and product type

- Ancillary charges: Technology, roadside assistance, reporting, compliance support

Even small percentage differences in ceding or adjudication fees compound significantly over a multi-year program. Two programs with identical admin fees can produce dramatically different financial outcomes — see Elite F&I Partners' breakdown of transparent reinsurance fee structures for a detailed illustration of how the full fee stack diverges.

Request a line-item disclosure in writing before comparing any two proposals. Verbal assurances about "competitive pricing" mean nothing without documentation.

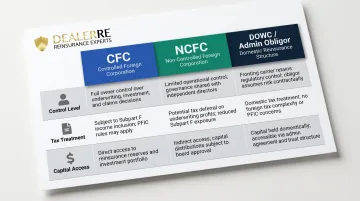

Program Structure and Ownership Control

The three primary structures differ substantially:

| Structure | Control | Tax Treatment | Capital Access |

|---|---|---|---|

| CFC | Dealer owns majority stake | 831(b) election available; tax only on investment income up to $2.9M premium cap | Full access to reserves and investment income |

| NCFC | Shared ownership among multiple dealers | No single dealer controls; profit participation model | Limited individual access; pooled structure |

| DOWC/Admin Obligor | Dealer owns 100% | C-corp taxation; no premium cap | Full control; backed by A-rated insurer via CLIP |

Each structure carries meaningfully different implications for control, tax exposure, and access to capital. In an admin obligor structure, the dealer's reinsurance company is backed by an A-rated insurer — a layer of security worth confirming with any administrator you're evaluating. Not all structures carry this protection, and the difference matters when claims volume spikes or reserves come under pressure.

Critical question: Who controls reserve assumptions, investment decisions, and distribution timing? If the answer is "the administrator," you're participating in a program without truly owning it.

Reporting Frequency and Clarity

Annual summaries hide multi-year trends in loss ratios, reserve adequacy, and fee erosion. A strong proposal commits to monthly reporting that shows:

- Premiums collected by product category

- Claims incurred and paid by product type

- Reserve changes and adequacy projections

- Expense deductions (line-item, not bundled)

- Underwriting results broken down, not blended into a single total

EasyCare's benchmarking analysis found that dealers receiving only annual summaries were frequently unable to identify fee erosion or deteriorating loss ratios until significant capital had already been affected — by which point course-correcting was costly.