This shift matters because front-end vehicle gross has faced decades of compression. According to Dealertrack's 2024 margin analysis, new vehicle front-end gross fell from $1,420 per unit in 2005 to $808 by 2014 — and while pandemic-era demand temporarily inflated those numbers, Q1 2025 showed a 14.4% year-over-year drop back toward structural norms.

F&I and ancillary products filled that gap. For franchise dealers, independent operations, and BHPH dealers alike, understanding how these products work — and who actually keeps the profit from them — is no longer optional strategy. It's operational survival.

This article covers what ancillary products are, how they function inside the F&I office, why they're critical to dealership profitability, and what most dealers get wrong about where the money actually goes.

TL;DR

- Ancillary products — VSCs, GAP, tire and wheel, and more — are supplemental protection products sold in the F&I office after vehicle price is set

- They represent the highest-margin revenue source available to dealerships of all types

- F&I gross profit per vehicle at public dealer groups averaged $2,505 in Q1 2025 — near all-time highs

- Third-party administrators quietly keep 50–70% of that income as underwriting profit

- Dealers who own their reinsurance company capture 100% of what third parties would otherwise keep

What Are Ancillary Products in Auto Dealerships?

Ancillary products are supplemental financial protection and coverage products offered to customers at the point of sale — specifically in the F&I office, after the vehicle price has already been negotiated.

The name reflects their position in the deal: they're secondary to the vehicle transaction itself, yet they drive a significant share of dealership back-end profitability.

For customers, these products reduce financial exposure from mechanical failure, theft, accidents, or loan imbalances after a total loss. For the dealership, they generate back-end income on every deal where they're accepted.

Key distinctions:

- Ancillary products are voluntary — they cannot legally be presented as conditions of financing

- They are separately priced from the vehicle, with their own disclosed costs

- They are administered by third-party providers unless the dealer has established a dealer-owned program

- They are distinct from manufacturer factory warranties, which are included in the vehicle price and administered by the automaker

That last point connects to a terminology clarification dealers encounter often. In practice, "ancillary products" and "F&I products" are used interchangeably — but technically, F&I products is the broader category for everything sold in the finance office, while ancillary products refers specifically to the protection and coverage add-ons, distinct from the financing transaction itself.

The Most Common Types of Ancillary Products Sold at Dealerships

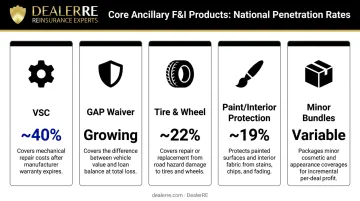

Vehicle Service Contracts (VSCs)

VSCs are the cornerstone of most F&I menus and typically the highest-revenue ancillary product per deal. They cover mechanical failures after the factory warranty expires (or for vehicles without factory coverage), with tiers ranging from exclusionary wrap coverage on newer vehicles down to powertrain-only contracts for high-mileage inventory.

Average VSC penetration rates sit around 40% of deals nationally, making them both the most commonly sold and most consistently profitable ancillary product.

DealerRE structures VSC reinsurance programs across the full coverage spectrum, from 72-month exclusionary wrap contracts for late-model vehicles to short-term powertrain programs for high-mileage used inventory.

GAP Waivers

GAP (Guaranteed Asset Protection) addresses a specific and growing risk: the gap between what insurance pays on a totaled vehicle and what the customer still owes on the loan.

Edmunds data from Q2 2025 found that 28.5% of new vehicle trade-ins were underwater — a four-year high — with an average negative equity balance of $6,754. For subprime used car buyers and BHPH customers carrying high loan-to-value ratios, GAP functions as a genuine financial safeguard, not an optional add-on.

For BHPH dealers specifically, GAP is particularly compelling: most are already absorbing these losses informally when they forgive remaining balances after total losses. A reinsured GAP program converts that cost center into revenue.

Tire and Wheel Protection

Tire and wheel plans cover road hazard damage — nails, potholes, metal debris, glass — that standard auto insurance typically excludes. Penetration averages around 22% nationally, with stronger performance in urban markets where road conditions make claims more likely.

Non-prorated coverage and 24/7 roadside assistance make tire and wheel a strong candidate for F&I menu bundling — DealerRE's product includes both.

Appearance and Paint/Interior Protection

Paint sealants, fabric protection, and exterior coatings carry relatively high markup relative to cost. Penetration runs around 19% nationally. These products draw occasional skepticism from both consumers and lenders, with lenders in particular scrutinizing high-cost appearance packages when reviewing total financed amounts.

Presentation discipline matters here. Products framed around concrete protection benefits (stain resistance, UV protection) hold better than vague "treatment" language.

Minor Ancillary Products and Bundles

Several smaller products serve a specific strategic function: they add incremental per-deal income at modest price points while creating bundled value that lifts acceptance across the whole menu. Common examples include:

- Windshield repair

- Door ding protection

- Key replacement

- Theft deterrent coverage

DealerRE recommends packaging windshield repair, door ding protection, and paint/fabric protection into a Multi-Shield ancillary bundle — a structure that builds customer value, raises overall penetration, and improves back-end gross without requiring high individual product prices.

How Ancillary Products Work in the F&I Office

The F&I Office Setting

By the time a customer reaches the F&I office, the vehicle price is settled. The F&I manager's job is to present ancillary products in a structured, compliant way — typically using a menu format that lays out product options, coverage details, and payment impact clearly.

Industry best practice (and regulatory guidance in several states) holds that a properly executed F&I menu should:

- Confirm the agreement from the sales department

- Explicitly identify all F&I products as optional

- Fully disclose the payment impact of each product

- Serve as a compliance document retained in the deal jacket

California and Minnesota have codified menu-style disclosure requirements for retail deals. Everywhere else, it's best practice — and increasingly an enforcement expectation given the FTC's escalating attention to F&I presentation.

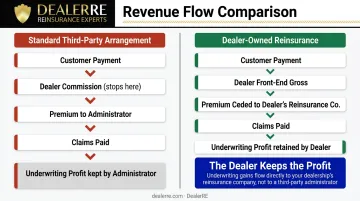

Revenue Flow: Where the Money Goes

When a customer pays for an ancillary product, the revenue doesn't all stay with the dealer — and that's where the structure gets critical.

Under a standard third-party arrangement:

- The dealer earns a commission or markup on the sale

- Premiums flow to the third-party administrator

- The administrator holds reserves, pays claims, and keeps whatever remains as underwriting profit

- The dealer's revenue stops at the initial sale

Under a dealer-owned reinsurance program (like DealerRE administers):

- The dealer still earns the same front-end gross

- Premiums are ceded to the dealer's own reinsurance company

- Claims are paid from the dealer's reinsurance account

- Everything remaining after claims = underwriting profit retained by the dealer

That gap has a direct implication for long-term profitability. As DealerRE puts it: if your third-party warranty provider weren't making a profit off you, why would they keep doing business with you?

Compliance Obligations

Understanding revenue structure is only half the equation — how products are presented carries its own legal weight. F&I products must be presented honestly, with these rules in play:

- Products cannot be presented as required for financing approval

- Cancellation rights and refund obligations are governed by state law

- The FTC's CARS Rule (effective July 2024) prohibits charging for add-ons without explicit consumer consent

The August 2024 FTC action against Asbury Automotive — charging dealerships with adding products without consent and discriminatory pricing — is a clear signal that enforcement is real and consequential. Menu discipline and transparent presentation aren't just ethical best practices; they're legal protection.

Why Ancillary Products Are Critical to Dealership Profitability

The Front-End Compression Problem

Vehicle sales margins are structurally thin. The average new car dealer operates on a total gross margin of approximately 3.9%, with a net profit margin of only 1.3%. F&I products, by contrast, allow dealerships to retain 70 to 80 cents per dollar generated — making the F&I department one of the most efficient profit centers in the building.

According to Haig Partners, public dealer groups averaged $2,505 in F&I gross profit per vehicle retailed in Q1 2025 — up 2.8% year-over-year and approaching the all-time high of $2,603 set in Q3 2022. F&I income has held near record levels even as front-end vehicle gross declined 14.4% over the same period.

That gap is the core argument for F&I: front-end margins are volatile and trending down, while a well-managed F&I program holds steady and grows.

The Compounding Revenue Effect

A dealership averaging $1,500 in ancillary product income per deal on 600 annual units generates $900,000 in F&I-related gross. At $2,000 per deal, that number crosses $1.2 million. F&I now contributes an estimated 25–35% of total dealership gross profit across the industry — and those per-deal averages are well within reach for dealers running disciplined programs.

The Profit Leakage Problem

Most dealers don't realize how much of that F&I income they're not actually keeping.

Under standard third-party arrangements, underwriting profit — the money left after claims are paid — flows to the administrator, not the dealer. The dealer earns a margin on the sale; the administrator builds a business on the spread between premiums and claims.

Dealer-owned reinsurance solves this directly. By establishing their own administrator obligor reinsurance company — the structure DealerRE has been building for dealers since 1994 — dealerships gain control over where that money goes. Key advantages of the structure include:

- Captures 100% of underwriting profits instead of passing them to a third-party administrator

- Holds premiums in a U.S. trust account, invested conservatively for additional return

- Keeps investment income inside the dealer's reinsurance company

- Turns what was a vendor's margin into a compounding financial asset the dealer owns

What remains after claims isn't a vendor's profit. It's the dealer's.

Common Misconceptions About Ancillary Products in Dealerships

Three persistent myths shape how many dealers think about ancillary products — and all three cost them money.

"Ancillary products are just a manipulation tactic."

The product itself provides real value. A VSC that pays for a failed transmission or GAP coverage that clears a $6,000 loan shortfall after a totaled car aren't gimmicks. Compliance and ethics issues arise from how products are presented, not from the products themselves. Transparent, menu-based presentation at honest prices serves both the customer and the dealer.

"The selling dealer keeps all the F&I profit."

This is the most operationally significant misconception. Under standard third-party arrangements, the dealer earns a commission — but the underwriting profit, often thousands of dollars per contract over its life, goes to the administrator. Dealers who haven't examined their program structure may be generating strong F&I income on paper while surrendering the most valuable portion of it.

"Dealer-owned reinsurance is only for large franchise groups."

DealerRE has been correcting this since Tim Byrd founded the company in 1994. The admin obligor reinsurance concept was built specifically to give dealers of varying sizes an alternative to third-party dependency.

DealerRE works with dealers selling 30+ cars per month across franchise, independent, and BHPH operations. Most larger dealers do own their reinsurance companies today — but the structure is accessible well below that scale.

Frequently Asked Questions

What is the difference between ancillary products and F&I products?

"F&I products" is the broader category for everything sold in the finance and insurance office. "Ancillary products" refers specifically to the protection and coverage add-ons — VSCs, GAP, tire and wheel, etc. — as distinct from the financing transaction itself. In practice, the terms are often used interchangeably.

Are ancillary products required for a car buyer to get financing?

No. Ancillary products are voluntary and cannot legally be presented as a condition of financing approval. Misrepresenting them as required is a compliance violation under FTC regulations and exposes the dealership to enforcement risk.

What are the most profitable ancillary products for dealerships?

Vehicle service contracts (VSCs) typically generate the highest per-deal F&I income, followed by GAP waivers. Profitability depends on whether the dealer retains underwriting profits through a reinsurance structure or surrenders them to a third-party administrator.

What is the difference between a vehicle service contract and a factory warranty?

A factory warranty is included by the manufacturer and covers defects for a specified period at no additional charge. A VSC is a separate, purchased agreement that extends or supplements mechanical coverage — administered by a third party or a dealer-owned program, not the manufacturer, and not classified as a warranty under U.S. law.

How do dealers measure ancillary product success?

Penetration rate — the percentage of deals that include a given product — and per-vehicle F&I income are the two primary metrics. F&I managers track penetration by product; dealer principals track total F&I PVR against volume to assess program performance.

Can independent and BHPH dealers benefit from ancillary product programs?

Yes. NIADA data indicates F&I revenue can equal or exceed vehicle sales profits for independent dealers. BHPH dealers are strong candidates for VSC and GAP reinsurance programs — their customer base makes both products especially relevant, and dealer-owned reinsurance structures are accessible to non-franchise dealers with sufficient volume.